Banking System in India

by

by In India the banks and banking have been divided in different groups. Each group has their own benefits and limitations in their operations. They have their own dedicated target market. Some are concentrated their work in rural sector while others in both rural as well as urban. Most of them are only catering in cities and major towns.

Indian Banking System: Structure

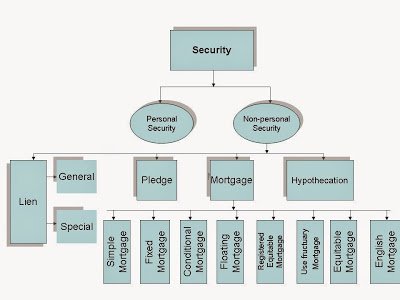

Bank is an institution that accepts deposits of money from the public.

Anybody who has account in the bank can withdraw money. Bank also lends money.

Indigenous Banking

The exact date of existence of indigenous bank is not known. But, it is certain that the old banking system has been functioning for centuries. Some people trace the presence of indigenous banks to the Vedic times of 2000-1400 BC. It has admirably fulfilled the needs of the country in the past.

However, with the coming of the British, its decline started. Despite the fast growth of modern commercial banks, however, the indigenous banks continue to hold a prominent position in the Indian money market even in the present times. It includes shroffs, seths, mahajans, chettis, etc. The indigenous bankers lend money; act as money changers and finance internal trade of India by means of hundis or internal bills of exchange.

Disvantages

(i) They are unorganized and do not have any contact with other sections of the banking world.

(ii) They combine banking with trading and commission business and thus have introduced trade risks into their banking business.

(iii) They do not distinguish between short term and long term finance and also between the purpose of finance.

(iv) They follow vernacular methods of keeping accounts. They do not give receipts in most cases and interest which they charge is out of proportion to the rate of interest charged by other banking institutions in the country.

Suggestions for Improvements

(i) The banking practices need to be upgraded.

(ii) Encouraging them to avail of certain facilities from the banking system, including the RBI.

(iii) These banks should be linked with commercial banks on the basis of certain understanding in the respect of interest charged from the borrowers, the verification of the same by the commercial banks and the passing of the concessions to the priority sectors etc.

(iv) These banks should be encouraged to become corporate bodies rather than continuing as family based enterprises.

Structure of Organized Indian Banking System

The organized banking system in India can be classified as given below:

Reserve Bank of India (RBI)

The country had no central bank prior to the establishment of the RBI. The RBI is the supreme monetary and banking authority in the country and controls the banking system in India. It is called the Reserve Bank’ as it keeps the reserves of all commercial banks.

Commercial Banks

Commercial banks mobilise savings of general public and make them available to large and small industrial and trading units mainly for working capital requirements.

Commercial banks in India are largely Indian-public sector and private sector with a few foreign banks. The public sector banks account for more than 92 percent of the entire banking business in India—occupying a dominant position in the commercial banking. The State Bank of India and its 7 associate banks along with another 19 banks are the public sector banks.

Scheduled and Non-Scheduled Banks

The scheduled banks are those which are enshrined in the second schedule of the RBI Act, 1934. These banks have a paid-up capital and reserves of an aggregate value of not less than Rs. 5 lakhs, hey have to satisfy the RBI that their affairs are carried out in the interest of their depositors.

All commercial banks (Indian and foreign), regional rural banks, and state cooperative banks are scheduled banks. Non- scheduled banks are those which are not included in the second schedule of the RBI Act, 1934. At present these are only three such banks in the country.

Regional Rural Banks

The Regional Rural Banks (RRBs) the newest form of banks, came into existence in the middle of 1970s (sponsored by individual nationalized commercial banks) with the objective of developing rural economy by providing credit and deposit facilities for agriculture and other productive activities of al kinds in rural areas.

The emphasis is on providing such facilities to small and marginal farmers, agricultural labourers, rural artisans and other small entrepreneurs in rural areas.

Other special features of these banks are

(i) Their area of operation is limited to a specified region, comprising one or more districts in any state.

(ii) Their lending rates cannot be higher than the prevailing lending rates of cooperative credit societies in any particular state.

(iii) The paid-up capital of each rural bank is Rs. 25 lakh, 50 percent of which has been contributed by the Central Government, 15 percent by State Government and 35 percent by sponsoring public sector commercial banks which are also responsible for actual setting up of the RRBs.

These banks are helped by higher-level agencies: the sponsoring banks lend them funds and advise and train their senior staff, the NABARD (National Bank for Agriculture and Rural Development) gives them short-term and medium, term loans: the RBI has kept CRR (Cash Reserve Requirements) of them at 3% and SLR (Statutory Liquidity Requirement) at 25% of their total net liabilities, whereas for other commercial banks the required minimum ratios have been varied over time.

Cooperative Banks

Cooperative banks are so-called because they are organized under the provisions of the Cooperative Credit Societies Act of the states. The major beneficiary of the Cooperative Banking is the agricultural sector in particular and the rural sector in general.

The cooperative credit institutions operating in the country are mainly of two kinds: agricultural (dominant) and non-agricultural. There are two separate cooperative agencies for the provision of agricultural credit: one for short and medium-term credit, and the other for long-term credit. The former has three tier and federal structure.

At the apex is the State Co-operative Bank (SCB) (cooperation being a state subject in India), at the intermediate (district) level are the Central Cooperative Banks (CCBs) and at the village level are Primary Agricultural Credit Societies (PACs).

Long-term agriculture credit is provided by the Land Development Banks. The funds of the RBI meant for the agriculture sector actually pass through SCBs and CCBs. Originally based in rural sector, the cooperative credit movement has now spread to urban areas also and there are many urban cooperative banks coming under SCBs.