Month: April 2020

by

by University of Mumbai BMS Notes

1st Semester

| Subjects | |

| Introduction to Financial Accounts (Updated) |

VIEW |

| Business Law (Updated) | VIEW |

| Business Statistics (Updated) | VIEW |

| Business Communication I (Updated) | VIEW |

| Foundation of Human Skills (Updated) | VIEW |

| Business Economics I (Updated) | VIEW |

2nd Semester

| Subjects | |

| Principles of Marketing (Updated) | VIEW |

| Industrial Law (Updated) | VIEW |

| Business Mathematics (No Update) |

VIEW |

| Business Communication II (Updated) | VIEW |

| Business Environment (Updated) | VIEW |

| Principles of Management (Updated) | VIEW |

3rd Semester

| Subjects | |

| Group A: Finance | |

| Basics of Financial Services (Updated) | VIEW |

| Introduction to Cost Accounting (Updated) | VIEW |

| Equity & Debt Market (Updated) | VIEW |

| Corporate Finance (Updated) | VIEW |

| Group B: Marketing | |

| Consumer Behaviour (Updated) | VIEW |

| Product Innovations Management (Updated) | VIEW |

| Advertising (Updated) | VIEW |

| Social Marketing (Updated) | VIEW |

| Group C: Human Resource | |

| Recruitment & Selection (Updated) | VIEW |

| Motivation and Leadership (Updated) | VIEW |

| Employees Relations & Welfare (Updated) |

VIEW |

| Organisation Behaviour & HRM (Updated) | VIEW |

| Ability Enhancement Compulsory Courses (AECC) | |

| Information Technology in Business Management I (Updated) | VIEW |

| Core Courses (CC) | |

| Business Planning & Entrepreneurial Management (Updated) | VIEW |

| Accounting for Managerial Decisions (Updated) | VIEW |

| Strategic Management (Updated) | VIEW |

4th Semester

| Group A: Finance | |

| Financial Institutions & Markets (Updated) |

VIEW |

| Auditing (Updated) | VIEW |

| Strategic Cost Management (Updated) | VIEW |

| Corporate Restructuring (Updated) | VIEW |

| Group B: Marketing | |

| Integrated Marketing Communication (Updated) |

VIEW |

| Rural Marketing (Updated) | VIEW |

| Event Marketing | VIEW |

| Tourism Marketing | VIEW |

| Group C: Human Resource | |

| Human Resource Planning & Information System (Updated) |

VIEW |

| Training & Development in HRM (Updated) | VIEW |

| Change Management (Updated) | VIEW |

| Conflict & Negotiation (Updated) | VIEW |

| Ability Enhancement Compulsory Courses (AECC) | |

| Information Technology in Business Management II (Updated) | VIEW |

| Core Courses (CC) | |

| Business Economics II (Updated) |

VIEW |

| Business Research Methods (Updated) | VIEW |

| Production & Total Quality Management (Updated) |

VIEW |

5th Semester

| Subjects | |

| Group A: Finance | |

| Investment Analysis & Portfolio Management (Updated) | VIEW |

| Commodity & Derivatives Market (Updated) |

VIEW |

| Wealth Management (Updated) | VIEW |

| Financial Accounting (Updated) | VIEW |

| Risk Management (Updated) | VIEW |

| Direct Taxes (Updated) |

VIEW |

| Group B: Marketing | |

| Services Marketing (Updated) | VIEW |

| E-Commerce & Digital Marketing (Updated) | VIEW |

| Sales & Distribution Management (Updated) | VIEW |

| Customer Relationship Management (Updated) | VIEW |

| Industrial Marketing | VIEW |

| Strategic Marketing Management (Updated) | VIEW |

| Group C: Human Resource | |

| Finance for HR Professionals & Compensation Management (Updated) | VIEW |

| Strategic Human Resource Management & HR Policies (Updated) | VIEW |

| Performance Management & Career Planning (Updated) | VIEW |

| Industrial Relations (Updated) | VIEW |

| Talent & Competency Management (Updated) | VIEW |

| Stress Management (Updated) | VIEW |

| Core Course (CC) | |

| Logistics & Supply Chain Management (Updated) | VIEW |

| Ability Enhancement Course (AEC) | |

| Corporate Communication & Public Relations (Updated) | VIEW |

6th Semester

| Subjects | |

| Group A: Finance | |

| International Finance (Updated) | VIEW |

| Innovative Financial Services (Updated) | VIEW |

| Project Management (Updated) | VIEW |

| Strategic Financial Management (Updated) | VIEW |

| Financing Rural Development | VIEW |

| Indirect Taxes (Updated) | VIEW |

| Group B: Marketing | |

| Brand Management (Updated) | VIEW |

| Retail Management (Updated) | VIEW |

| International Marketing (Updated) | VIEW |

| Media Planning & Management (Updated) | VIEW |

| Sports Marketing | VIEW |

| Marketing of Non-Profit Organisation | VIEW |

| Group C: Human Resource | |

| HRM in Global Perspective (Updated) | VIEW |

| Organisational Development (Updated) | VIEW |

| HRM in Service Sector Management | VIEW |

| Workforce Diversity (Updated) | VIEW |

| Human Resource Accounting & Audit (Updated) | VIEW |

| Indian Ethos in Management (Updated) | VIEW |

| Core Course (CC) | |

| Operation Research (Updated) | VIEW |

Budgeting introduction

Budgeting is the process of preparing detailed projections of future amounts. Companies often engage in two types of budgeting:

- Operational budgeting, and

- Capital budgeting

Examples of Operational Budgeting

In a business, the budgeting for operations will include preparing the following projections for the next accounting year:

- Amounts for sales

- Amounts for producing goods

- Amounts for each department’s expenses

- Summarizing the above budgets into a master budget or profit plan

- Cash receipts and disbursements for a cash budget

- Projected financial statements also referred to as pro-forma financial statements

Once prepared and approved, the budgeted amounts are used as a guide or road map in controlling the next year’s business activities.

Example of Capital Budgeting

Capital budgeting involves future projects which overlap several or many future accounting periods. Capital budgeting usually means listing each project along with its cash outlays and expected cash inflows for each year. The amounts should be discounted to their present values and also ranked by priority and profitability.

Once prepared, the capital budget provides a guide for investing in future fixed assets as well as arranging for the financing of the projects.

Approaches to budgeting process

Budgeting can be done in a variety of ways, and it is always a smart choice to be aware of more than just a single way of budgeting. However, two of the most important approaches to budgeting process are:

Top-Down Budget

In the top-down budgeting process, the primary input is made by the top-level executives of the business. The echelon of a certain organizational hierarchy lays down all the guidelines according to which budget will be made. They outline the financial goals that a budget should maintain. Moreover, guidelines related to sales budget, compensation, etc. are all given by the top management. The lower level management is given the least amount of participation in the budgeting process. They are only involved in executing these guidelines.

Bottom-Up Budget

The bottom-up approach to budgeting adopts a more inclusive approach towards the budgeting process. Although the upper-level management gives out the general guidelines related for a budget, however, employees and the lower management formulate these budgets. Each division of the organization forms its budget in accordance to the general guidelines. In the end, the budget of the entire organization is formed by combining the individual budgets of each division. The bottom-up approach for a budgeting process is highly inclusive in nature. The employees overall tend to be much more committed to working under the budget in this approach. This is due to the fact that employees have participated in drawing up a budget and therefore they know that the budget is very acceptable.

Components of budget

There are many divisions of an organization and therefore budgeting for each of the division is specific to its needs. When all the budgets of each division are combined, it results into the final budget, which is often referred to as the “Master Budget”. Various components of the budget are discussed as follows:

Sales Budget

Sales budget outlines the forecasted income stream of the business. It is usually the first budget to be prepared as the revenue generated will ultimately determine the level of expenditure. Under the sales budget, sales of the business are forecasted. Sales are forecasted in terms of sales volume and the sales revenue. The forecasting is done on the following basis:

- Previous pattern of sales

- Economic conditions e.g. rate of inflation, interest rate, exchange rate, economic growth rate

- Political conditions

- State of competition in the market

- Other factors that can affect the sales e.g. technology, etc.

Production Budget

The production budget is of high importance in the overall budgeting process. It determines the number of units of a product that will be produced by the business. It also determines the cost at which the products have to be produced. Production budget is made according to the sales budget. Required sales units, opening inventory and required closing inventory are used to reach the number of units that have to be produced in a budgeted period.

Direct Material Purchases Budget

Direct materials, like the name suggests, are the ones that are being used directly in the production of goods. The budget related to direct material determines the amount and cost of these resources that will be required in the production activity.

Labor, Overhead, and SG&A Budget

Budgets related to labor, overhead and SG&A (selling, general and administrative) are prepared separately. They are then combined under a single head.

The direct labor budget is prepared. Labor that participates in the production process forms the direct labor cost. This budget is prepared according to the number of labor hours and the cost per hour.

Overheads are those costs that are not incurred directly in the production of goods, but are indispensable with regard to the production activity e.g. rent of the factory. The budget of the overhead cost is prepared in relation to the direct labor hours.

SG&A costs are incurred in order to conduct the day to day operations of a business. They consist of fixed and variable costs.

Cash Budget

Cash is known to have a similar importance to a business as blood has to body. No matter how successful a business is, if it runs out of cash, its survival is seriously jeopardized. In order to ensure smooth operations of the business, strong emphasis must be laid upon the development of cash budget. Cash budget helps to formulate in advance the payment and receipt cycles of the business and thus it ensures that cash is readily available to a business. By formulating cash budget, the business can keep track of its accounts receivables and accounts payable. In order to avoid shortage of cash, the business can arrange its credit plans related to accounts receivables and accounts payable accordingly.

Budgeted Financial Statements

Budgeted financial statements are prepared on the basis of each budget component. These budgeted financial statements are called pro forma financial statements. Through the budgeted financial statements, a business will be able to forecast its profits. Profit forecasting is important because it will determine the viability of carrying out the business.

Steps in the budgeting process

Budgeting is a detailed process with several intricate steps leading up to understanding it at large. A step-by-step guide to the budgeting process is given as below.

-

Update budget assumptions

Budgets are always prepared on certain assumptions. Those assumptions could be related to the sales trends, cost trends or environmental conditions. Before embarking on preparing the budget, these assumptions must be thoroughly reviewed according to the recent environmental conditions.

-

Note Available funding

Limited funding can greatly hinder the growth projects of the business. Therefore, in the preparation of budgets adequate attention has to be given to the available funding as the availability of investable funds will determine the initiation of viable projects.

-

Step costing points

The business environment is subject to dynamism. Every day it is posed with challenges that can completely change its cost structure. Therefore, in the budgeting process certain factors that can affect the costing for the business should be closely considered. These factors should be identified beforehand in order to make the budget realistic.

-

Create budget package

In budget package, previous standards related to the budgeting process are taken in order to formulate a budget for the current period. Previous standards are updated according to the recent environmental conditions. Budget package is a kind of outline according to which budget has to be prepared.

-

Obtain revenue forecast

There is no denying the fact that sales budget is the most crucial budget of all. All the budgets are based on the sales budget. Furthermore, sales budget determines whether the business is generating enough revenue necessary for its survival. Therefore, adequate attention must be given to the preparation of sales budget by forecasting demand accurately.

-

Obtain department budgets

The department budgets will help to reach a budgeted expenditure for the budgeted period. Each department will prepare its own budget and then all of them will be combined to become a part of the master budget.

-

Validate compensation

Compensation plans are a significant component of the budgeting process. As compensation is subject to an annual increase, therefore, it should be prepared with great care. The approval for compensation increase should first be taken from the top management, and then it should be augmented in the budgeted compensation plans.

-

Validate bonus plans

In order to maintain the morale of the employees, bonuses are frequently given to out motivated workers. Bonuses act as an appraisal method. Bonus announcements that are not considered in the budgeting process can create havoc in the profits of the business. Therefore, any bonus plans should be taken into consideration beforehand. The top management should be consulted for any bonus plans.

-

Obtain capital budget requests

Capital expenditure ensures expansion of the business. It helps the business to avail the opportunities necessary for business growth. Any capital expenditure plans should be taken in advance, and they should be included in the budgeting process accordingly.

10. Update the budget model

Any changes in the assumptions of the budget model should be updated, and final budget should be prepared accordingly. A delay in this may lead to glitches later on that could cause confusion.

11. Review the budget

The budget should be reviewed thoroughly once it is prepared in order to correct any flaws. A little decimal placed wrongly can create quite an unbalance in the budget sheet.

12. Obtain approval

The budget should be presented to the top management. They will evaluate whether it has been prepared according to their requirements and finally l approve it if it does not need any changes.

13. Issue the budget

The budget should be formally issued after its approval. All the operations there and then will take place according to it.

Methods of Budgeting

-

Incremental Budgeting

Incremental budgeting takes last year’s actual figures and adds or subtracts a percentage to obtain the current year’s budget. It is the most common method of budgeting because it is simple and easy to understand. Incremental budgeting is appropriate to use if the primary cost drivers do not change from year to year. However, there are some problems with using the method:

- It is likely to perpetuate inefficiencies. For example, if a manager knows that there is an opportunity to grow his budget by 10% every year, he will simply take that opportunity to attain a bigger budget, while not putting effort into seeking ways to cut costs or economize.

- It is likely to result in budgetary slack. For example, a manager might overstate the size of the budget that the team actually needs so it appears that the team is always under budget.

- It is also likely to ignore external drivers of activity and performance. For example, there is very high inflation in certain input costs. Incremental budgeting ignores any external factors and simply assumes the cost will grow by, for example, 10% this year.

-

Activity-Based Budgeting

Activity-based budgeting is a top-down budgeting approach that determines the amount of inputs required to support the targets or outputs set by the company. For example, a company sets an output target of $100 million in revenues. The company will need to first determine the activities that need to be undertaken to meet the sales target, and then find out the costs of carrying out these activities.

-

Value Proposition Budgeting

In value proposition budgeting, the budgeter considers the following questions:

- Why is this amount included in the budget?

- Does the item create value for customers, staff, or other stakeholders?

- Does the value of the item outweigh its cost? If not, then is there another reason why the cost is justified?

Value proposition budgeting is really a mindset about making sure that everything that is included in the budget delivers value for the business. Value proposition budgeting aims to avoid unnecessary expenditures although it is not as precisely aimed at that goal as our final budgeting option, zero-based budgeting.

-

Zero-Based Budgeting

As one of the most commonly used budgeting methods, zero-based budgeting starts with the assumption that all department budgets are zero and must be rebuilt from scratch. Managers must be able to justify every single expense. No expenditures are automatically “okayed”. Zero-based budgeting is very tight, aiming to avoid any and all expenditures that are not considered absolutely essential to the company’s successful (profitable) operation. This kind of bottom-up budgeting can be a highly effective way to “shake things up”.

The zero-based approach is good to use when there is an urgent need for cost containment, for example, in a situation where a company is going through a financial restructuring or a major economic or market downturn that requires it to reduce the budget dramatically.

Zero-based budgeting is best suited for addressing discretionary costs rather than essential operating costs. However, it can be an extremely time-consuming approach, so many companies only use this approach occasionally.

Comprehensive /Master budget

The Master Budget is consolidated summary of the various functional budgets. It has been defined as “a summary of the budget schedules in capsule form made for the purpose of presenting, in one report, the highlights of the budget forecast”.

The definition of this budget given by the Chartered Institute of Management Accountant, England, is as follows:

“The summary budget incorporating its component functional budgets and which is finally approved adopted and employed”.

The master budget is prepared by the budget committee on the basis of co-ordinated functional budgets and becomes the target for the company during the budget period when it is finally approved by the committee.

This budget summarises functional budgets to produce a Budgeted Profit and Loss Account and a Budgeted Balance Sheet as at the end of the budget period as is clear from the form given as follows:

Advantages of the Master Budget:

Following are the main advantages of the master budget:

(1) A summary of all functional budgets in capsule form is available in one report.

(2) The accuracy of all the functional budgets is checked because the summarised information of all functional budgets should agree with the information given in the master budget.

(3) It gives an overall estimated profit position of the organisation for the budget period.

(4) Information relating to forecast balance sheet is available in the master budget.

This budget is very useful the top management because it is usually interested in the summarised meaningful information provided by this budget.

Some of the components of the master budget are briefly explained as follows:

1. Materials and utilities budget:

This budget provides for acquiring raw materials required for production, spare parts for maintenance, labour time, machine time, and energy consumption and so on.

The labour time and machine time is usually related to what a unit of time is budgeted to yield. In other words it relates to the output per unit of time.

2. Control of liquidity:

This budget involves cash flow and is very important in controlling cash and meeting current financial obligations. The budget forecasts cash receipts and outlays for a given period of time and are necessary to control the income and expenses so that there is no shortage of cash to pay for bills and also there in no excessive unused cash which may be unproductive.

3. Revenue and expense budgets:

The revenue budgets should show anticipated sales by product or by geographical territory or by department and so on. In anticipating sales, managers must take into account their competitors, planned advertising expenditures, sales force effectiveness and other relevant factors.

The expense budgets list the primary activities undertaken by a unit to achieve its goals and the costs associated with these activities. These budgets cover all necessary and relevant areas including rent, utilities, supplies, security and so on.

4. Capital expenditure budgets:

These budgets plan for long term investments and include expenditures for new plants and equipment, major installations, replacement of existing equipment, renovation of buildings and so on. These are typically substantial expenditures both in terms of magnitude and duration.

Capital budgeting is a part of long range planning and must be broken into well defined phases of the program known as milestones each phase being budgeted for cost, time and effort in self contained way.

5. Sales budgets:

A sales budget is the direct outcome of sales forecast and is based on the consideration of demand and supply situation, competition, past sales trends, future prediction of sales, seasonal changes that affect sales and so on.

The sales forecasting is based upon such factors as population trends, general economic environment, consumer’s purchasing power, disposable income, price trends of the products, inflation rate and so an.

6. Production budget:

The production budget contains the plan for future manufacturing operations and is based upon the sales forecasts and sales budgets. It aims at obtaining utilization of manufacturing methods and facilities. The budget may be prepared in two parts, one being the production volume budget and the other being the budget for cost of manufacturing.

The production volume budget relates to the production of physical units and involves production planning. The cost of production budget deals with all costs attributable to the manufacture of the product.

7. Balance Sheet:

A balance sheet is composite budget and reflects anticipated assets, liabilities and owner’s equity or net worth at the end of a given period in the future. It provides a forecast of the anticipated financial status of the company at a future date.

All these budgets should be carefully set and should be flexible enough so that any reasonable changes in the values of various variables can be accommodated.

Cost Variance Analysis

When the actual cost differs from the standard cost, it is called variance. If the actual cost is less than the standard cost or the actual profit is higher than the standard profit, it is called favorable variance. On the contrary, if the actual cost is higher than the standard cost or profit is low, then it is called adverse variance.

Each element of cost and sales requires variance analysis. Variance is classified as follows:

- Direct Material Variance

- Direct Labor Variance

- Overhead Variance

- Sales Variance

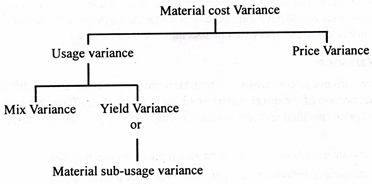

Direct Material Variance

Material variances can be of the following categories:

- Material Cost Variance

- Material Price Variance

- Material Usage Variance

- Material Mix Variance

- Material Yield Variance

| Material Cost Variance | |

| Standard cost of materials for actual output – Actual cost of material used

Or Material price variance + Material usage or quantity variance Or Material price variance + Material mix variance + Material yield variance |

|

| Material Price Variance | |

| Actual usage ( Standard Quantity Price – Actual Unit Price)

Actual Usage = Actual Quantity of material (in units) used Standard Unit Price = Standard Price of material per unit Actual Unit Price = Actual price of material per unit |

|

| Material Usage or Quantity Variance | |

| Material usage or Quantity variance: Standard price per unit (Standard Quantity – Actual Quantity ) | |

| Material Mix Variance | |

| Material mix variance arises due to the difference between the standard mixture of material and the actual mixture of Material mix.

Material Mix variance is calculated as a difference between the standard prices of standard mix and the standard price of actual mix. If there is no difference between the standard and the actual weight of mix, then: Standard unit cost (Standard Quantity – Actual Quantity ) Or Standard Cost of Standard Mix – Standard cost of Actual Mix Sometimes due to shortage of a particular type of material, standard is revised; then: Standard unit cost (Revised Standard Quantity – Actual Quantity) Or Standard cost of revised Standard Mix – Standard Cost of Actual mix If the actual weight of mix differs from the standard weight of mix, then: Standard cost of revised standard mix × (Total weight of actual mix /mixTotal weight of revised standard mix) |

|

| Material Yield Variance | |

| When the standard and the actual mix do not differ, then

Yield Variance = Standard Rate × (Actual Yield – Standard Yield) Standard Rate = Standard cost of standard mix /Net standard output (i.e.Gross output−Standard loss) |

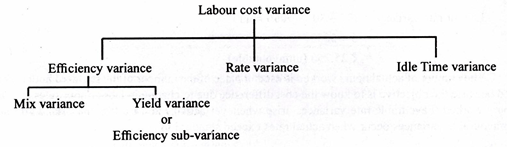

Direct Labor Variance

Direct labor variances are categorized as follows:

- Labor Cost Variance

- Labor Rate of Pay Variance

- Total Labor Efficiency Variance

- Labor Efficiency Variance

- Labor Idle Time Variance

- Labor Mix Variance or Gang Composition Variance

- Labor Yield Variance or Labor Efficiency Sub Variance

- Substitution Variance

| Labor Cost Variance |

| Standard Cost of Labor – Actual Cost of Labor |

| Labor Rate of pay Variance |

| Actual Time taken × (Standard Rate – Actual Rate) |

| Total Labor Efficiency Variance |

| Standard rate × (Standard time – Actual time) |

| Labor Efficiency Variance |

| Standard Rate (Standard time for actual output – Actual time worked) |

| Labor Idle Time Variance |

| Idle Time Variance = Abnormal Idle Time × Standard Rate

Total Labor Cost Variance = Labor rate of Pay variance + Total labor Efficiency Variance Total Labor Efficiency Variance = Labor Efficiency Variance + Labor Idle Time Variance |

| Labor Mix Variance or Gang Composition Variance |

| If actual composition of labor is equal to standard:

LMV = Standard Cost of Standard Composition (for Actual time taken) – Standard Cost of Actual Composition (for Actual time worked) If standard composition of labor revised due to shortage of any specific type of labor but the total actual time is equal to the total standard time: LMV = Standard Cost of Revised Standard Composition (for Actual Time Taken) – Standard Cost of Actual Composition (for Actual Time Worked) If actual and standard time of labor differs: = (Total time of actual labor composition/ Total time of standard labor composition) × Std.cost of std.composition − Std.cost of actual composition In case the Standard is revised and there is a difference in the total Actual and the Standard time: = (Total time of actual labor composition/Total time of revised std./labor composition) × Std.cost of (revised std.composition − actual composition) |

| Labor Yield Variance |

| Std. Labor Cost per unit × (Actual Yield In units – Std. Yield in units expected from Actual time worked on production) |

| Substitution Variance |

| (Actual hrs × Std. Rate of Std. Worker) – (Actual hrs × Std.Rate actual worker) |

Fixed and Flexible Budget

Fixed Budget:

This budget is drawn for one level of activity and one set of conditions. It has been defined as a budget which is designed to remain unchanged irrespective of the volume of output or turnover attained. It is rigid budget and is drawn on the assumption that there will be no change in the budgeted level of activity. It does not take into consideration any change in expenditure arising out of changes in the level of activity.

Thus, it does not provide for changes in expenditure arising out of change in the anticipated conditions and activity. A fixed budget will, therefore, be useful only when the actual level of activity corresponds to the budgeted level of activity.

A master budget tailored to a single output level of (say) 20,000 units of sales is a typical example of a fixed budget. But, in practice, the level of activity and set conditions will change as a result of internal limitations and external factors like changes in demand and prices, shortages of materials and power, acute competition etc.

It is hardly of any use as a mechanism of budgetary control because it does not make any distinction between fixed, variable and semi-variable costs and provides for no adjustment in the budgeted figures as a result of change in cost due to change in level of activity. It does not provide a meaningful basis for comparison and control. It is also not helpful at all in the fixation of price and submission offenders.

Flexible Budget:

The Chartered Institute of Management Accountants, England, defines a flexible budget (also called sliding scale budget) as a budget which, by recognising the difference in behaviour between fixed and variable costs in relation to fluctuations in output, turnover, or other variable factors such as number of employees, is designed to change appropriately with such fluctuations. Thus, a flexible budget gives different budgeted costs for different levels of activity.

A flexible budget is prepared after making an intelligent classification of all expenses between fixed, semi-variable and variable because the usefulness of such a budget depends upon the accuracy with which the expenses can be classified.

Such a budget is prescribed in the following cases:

(i) Where the level of activity during the year varies from period to period, either due to the seasonal nature of the industry or to variation in demand.

(ii) Where the business is a new one and it is difficult to foresee the demand.

(iii) Where the undertaking is suffering from shortage of a factor of production such as materials, labour, plant capacity etc. The level of activity depends upon the availability of such a factor of production.

(iv) Where an industry is influenced by changes in fashion.

(v) Where there are general changes in sales.

(vi) Where the business units keep on introducing new products or make changes in the design of its products frequently.

(vii) Where the industries are engaged in make to order business like ship-building.

Utility (or Importance) of Flexible Budget

- Flexible budget provides a logical comparison of budgeted allowances with the actual cost i.e., a comparison with like basis.

- Flexible budget reckons operational realities and streamlines control function and profit planning. It gives balanced perspective on comparison. When flexible budget is prepared, actual cost at actual activity is compared with budgeted cost at actual activity i.e., two things to a like basis.

- Flexible budget recognises concept of variability and provides logical comparison of expenditure with actual expenditure as a means of control.

- With flexible budget, it is possible to establish budgeted cost for any range of activity.

- A flexible budget is very useful for purposes of budgetary control because it corresponds with changes in the level of activity.

- It is helpful in assessing the performance of departmental heads because their performance can be judged in relation to the level of activity attained by the organisation.

- Cost ascertainment at different levels of activity is possible because a flexible budget is prepared for various levels of activity.

- It is helpful in price fixation and sending quotations.

Difference

|

Fixed Budget |

Flexible Budget |

|

| Meaning | The budget designed to remain constant, regardless of the activity level reached is Fixed Budget. | The budget designed to change with the change in the activity levels is Flexible Budget. |

| Nature | Static | Dynamic |

| Activity Level | Only one | Multiple |

| Performance Evaluation | Comparison between actual and budgeted levels cannot be done accurately, if there is a distinction in their activity levels. | It provides a good base for making a comparison between the actual and budgeted levels. |

| Rigidity | Fixed Budget cannot be modified as per the actual volume. | Flexible budget can be easily modified in accordance with the activity level attained. |

| Estimates | Based on assumption | Realistic and Practical |

Functional Budgets

A functional budget is a budget which relates to any of the functions of an undertaking, e.g., sales, production, research and development, cash etc.

Following functional budgets are generally prepared:

(i) Sales Budget:

Sales budget is the most important budget and of primary importance. It forms the basis on which all the other budgets are built up. This budget is a forecast of quantities and values of sales to be achieved in a budget period. Every effort should be made to ensure that its figures are as accurate as possible because this is usually the starting budget (sales being limiting factor on which all the other budgets are built up).

The Sales Manager should be made directly responsible for the preparation and execution of the budget. The sales budget may be prepared according to products, sales territories, types of customers, salesmen etc.

In the preparation of the sales budget, the sales manager should take into consideration the following factors:

- Past Sales Figures and Trends:

The complier of the sales budget should be assisted by graphs recording sales of the previous year and the general sales trend (upward and downward) should be noticed from the graphs. The record of previous year’s sales is the most reliable basis as to future sales as the past performance is based on actual business conditions. But in addition to past sales, other factors affecting future sales, e.g., seasonal fluctuations, growth of market, trade cycle etc., should be considered in the preparation of the sales budget.

- Salesmen’s Estimates:

In preparing the sales budget, the sales manager should consider the estimates of sales received from salesmen because they can make more accurate estimates, being in direct contact with the customers. However, it should be seen that salesmen’s estimates should neither be over-optimistic nor too conservative.

- Plant Capacity:

The budget should be within the plant capacity available and should ensure proper utilisation of plant facilities. Proposed plant extensions should be allowed for in the preparation of the sales budget.

- Availability of Raw Material and Other Supplies:

Adequate supply of raw materials and other supplies should be ensured before preparing the sales estimates. Sales estimates should be adjusted according to the availability of raw material if the raw materials are in short supply.

- General Trade Prospects:

The probability of the sales going up or down depends on the general trade prospects. In this connection valuable information may be gathered from financial papers and magazines such as the Economic Times, the Financial Express, the Commerce, etc.

- Orders in Hand:

In boom periods or where production is a very lengthy process the value of orders in hand may have considerable influence on the amount of sales to be budgeted.

- Seasonal Fluctuations:

In preparation of the sales budget, seasonal fluctuations should be considered because sales are affected by these fluctuations. In order to have an even flow of production, efforts should be made to minimise the effects of seasonal fluctuations on sales by giving special concessions or added inducements during the off- season.

- Financial Aspect:

The sales budget should be within the financial capacity of the concern. Sales expansion usually requires an increase in capital outlay. Thus, if any big sales expansion is planned, it must be ensured that facilities are available to finance the operations.

- Adequate Return on Capital Employed:

The sales volume budgeted should produce an adequate return on the capital employed.

- Competition:

The nature and degree of competition within the industry should be considered in the preparation of the sales budget to have a realistic sales budget capable of being achieved in the face of competition.

- Miscellaneous Considerations:

Other considerations such as advertising and sales promotion efforts, government intervention, import possibility, product profitability, market research studies, pricing policies etc. should also be kept in view.

The sales manager, after taking into consideration the above factors, should prepare the sales budget in terms of quantities and amounts and the sales estimates must be analysed for products periods and territories. The sales budget should include an estimate of selling and distribution costs in addition to an estimate of the total proceeds.

(ii) Production Budget:

Production budget is a forecast of the total output of the whole organisation broken down into estimates of output of each type of product with a scheduling of operations (by weeks and months) to be performed and a forecast of the closing finished stock. This budget may be expressed in quantitative (weight, units etc.) or financial (rupees) units or both.

This budget is prepared after taking into consideration the estimated opening stock, the estimated sales and the desired closing finished stock of each product.

The Works Manager is responsible for the total production budget and the departmental managers are responsible for the departmental production budget.

In preparing the production budget, the following factors are considered:

(1) The time lag between the production in the factory and sales to the customer should be considered so as to allow for the time required for the despatch of goods from the factory to the place of the customers.

(2) The stock of goods to be maintained both at the factory’s godown and at the sales centres.

(3) The level of production needed to meet the sales programme. Monthly production targets should be fixed and it should be seen that production is kept more or less at a uniform level throughout the year.

Planning the level of production involves the answer of four questions:

(a) What is to be produced?

(b) When is it to be produced?

(c) How is it to be produced?

(d) Where is to be produced?

The material, labour and plant requirements should be ascertained to have the desired production to meet the sales programme.

The sales and the production budget are inter-dependent because production budget is governed by the sales budget and the sales budget is largely determined by the production capacity and by production costs. The specimen proforma of production budget is given on the next page.

(iii) Cost of Production Budget:

After determining the volume of output the cost of procuring the output must be obtained by preparing a cost of production budget. This budget is an estimate of cost of output planned for a budget period and may be classified into material cost budget, labour cost budget and overhead budget because cost of production includes material, labour and overheads.

Materials Budget:

In drawing up the production budget, one of the first requirements to be considered is material. As we know, materials may be direct or indirect. Thus materials budget deals with the requirement and procurement of direct materials. Indirect materials are dealt with under the works overhead budget.

The budget should be related to the production budget and the period of the budget should be of short duration because this budget has an important bearing on the cash budget.

The preparation of the materials budget includes:

(1) The preparation of estimates of different types of raw materials needed for various products.

(2) Procuring or purchasing raw materials in required quantities at the required time.

In preparing the materials budget the following factors are considered:

(i) Raw materials required for the budgeted output.

(ii) The percentage of raw materials to total cost of products should be calculated on the basis of previous records. On the basis of this percentage a rough total value of raw materials required for the budgeted output will be ascertained.

(iii) Consideration must be given to the company’s stocking policy. Figures related to the anticipated raw materials stock to be held at different times should be known.

(iv) Consideration must be given to the lag between the placing of the order of the purchase of materials and the receipt of materials.

(v) The seasonal nature in the availability of raw materials should be considered.

(vi) The price trend in the market.

Materials budget can be classified into material requirement budget and material procurement purchase budget. The material requirement budget gives information about the quantity of materials required during the budget period to attain the production target. Material requirement budget takes into consideration the inventory of materials and the materials on order at the beginning of a budget period, and the anticipated inventory of materials are the materials to be on order on the closing date of the budget period.

Purchase Budget:

Purchase Budget is mainly dependent on production budget and material requirement budget. This budget provides information about the materials to be acquired from the market during the budget period.

Following factors should be taken into consideration while preparing a purchase budget:

- Quantity and quality of each material needed according to the production target;

- Capital items, tools and general supplies required during the budget period ;

- The present stock position and materials expected to arrive, already covered by purchase orders ;

- The dates on which purchase items are required ;

- Prices of items to be bought and possibility of quantity discount;

- Sources of supply ;

- Availability of cash to settle accounts of suppliers ;

- Transport requirements ;

- Inspection and receiving arrangements ; and

- Storage capacity and other factors such as handling of stocks, insurance, obsolescence and shrinkage.

Purchase budget should be prepared by the purchase manager by getting relevant information about capital items, tools, general supplies and direct materials required during the budget period from other related departments. Like other budgets, the purchase budget has to be approved by the budget committee.

After approval it becomes the responsibility of the purchase officer to see that purchases are made as per the purchase budget.

(iv) Labour and Personnel Budget:

Direct Labour Budget:

This budget gives an estimate of the requirements of direct labour essential to meet the production target. This budget may be classified into labour requirement budget and labour recruitment budget. The labour requirement budget is developed on the basis of requirement of the production budget given and detailed information regarding the different classes of labour, e.g. fitters, welders, turners, millers, grinders, drillers etc., required for each department, their scales of pay and hours to be spent.

This budget is prepared with a view to enable the personnel department to carry out programmes of training and transfer and to find out sources of labour needed so that every effort may be made to remove difficulties arising in production through lack of suitable personnel.

Labour recruitment budget is prepared on the basis of labour requirement budget after taking into consideration the available workers in each department, the expected changes in the labour force during the budget period due to the labour turnover.

This budget gives information about the personnel specifications for the jobs for which workers are to be recruited, the degree of skill and experience required and the rates of pay. In preparing the labour cost budget, the question of overtime should not be overlooked because workers are to get higher rates of wages if they work on overtime.

Regular overtime should be avoided by engagement of additional workers and extension of plant. Where standard costing system is applied, the labour cost budget is developed on the basis of standard labour cost per unit multiplied by the quantity of anticipated production determined in the production budget. If standard costing system is not being followed in the organisation, the information of labour cost may be obtained from past records or estimated cost.

Manpower Budget:

This budget gives the requirements of direct and indirect labour necessary to meet the programme set out in the sales, manufacturing, maintenance, research and development and capital expenditure budgets. The labour requirements are expressed in terms of rupee value, number of labour hours, number and grade of workers etc. This budget makes provision for shift and overtime work and for the effective training for new workers on labour cost.

The main purposes of this budget are:

(1) It provides efficient personnel management.

(2) It helps to make provision for a suitable yardstick with which the actual labour force may be compared and controlled.

(3) It helps in reducing labour turnover by providing favourable conditions.

(4) It also helps to measure and stabilise the ratio between direct labour and indirect labour.

(5) It gives the requirements of cash for paying wages and thus facilitates the preparation of Cash Budget.

(v) Manufacturing (or Production) Overheads Budget:

This budget gives an estimate of the works overhead expenses to be incurred in a budget period to achieve the production target. The budget includes the cost of indirect materials, indirect labour and indirect works expenses. The budget may be classified into fixed cost, variable cost and semi-variable cost. It can be broken into departmental overhead budget to facilitate control.

In preparing the budget, fixed works overhead can be estimated on the basis of past information after taking into consideration the expected changes which may occur during the budget period. Variable expenses are estimated on the basis of the budgeted output because these expenses are bound to change with the change in output.

The Cost Accountant prepares this budget on the basis of figures available in the manufacturing overhead ledger or the head of the workshop may be asked to give estimates for the manufacturing expenses. A good method is to combine the estimates of the Cost Accountant and the shop executive.

(vi) Administration Expenses Budget:

This budget covers the expenses incurred in framing policies, directing the organisation and controlling the business operations. In other words, the budget provides an estimate of the

expenses of the central office and of management salaries. The budget can be prepared with the help of past experience and anticipated changes.

Budget may be prepared for each administration department so that responsibility for increasing such expenses may be fixed and related to the different executives. Much difficulty is not experienced in developing such budget as most of the administration expenses are of a fixed nature.

Although fixed expenses remain constant and are not related to sales volume in the short run, they are dependent upon sales in the long run. With a small change in output, they do not change.

However, if there is a persistent fall in output, administration expenses will have to be reduced by discharging the services of some members of the staff and taking other economy measures. On the other hand, with persistent increase in output or business activity, administration expenses will increase but they may lag behind business activity.

(vii) Plant Utilisation Budget:

This budget lays down the requirements of plant capacity to carry out the production as per the production programme. This budget is expressed in terms of convenient physical units as weight or number of products or working hours.

The main functions of this budget are:

(i) It will show the machine load in each department during the budget period.

(ii) It will indicate the overloading on some departments, machine or group of machines and alternative courses of actions as working overtime, off-loading, procurement or expansion of plants, sub-contracting etc., can be taken.

(iii) Idle capacity in some departments may be utilised by making efforts to increase the demand for the products by providing after sale service, conducting advertisement campaign, reducing prices, introducing lucky prize coupons, recruiting efficient sales staff etc.

(viii) Capital Expenditure Budget:

The capital expenditure budget gives an estimate of the amount of capital that may be needed for acquiring the fixed assets required for fulfilling production requirements as specified in the production budget. The budget is prepared after taking into consideration the available productive capacities, probable reallocation of the existing assets and possible improvement in production techniques. Separate budgets may La prepared for different items of fixed assets such as plant and equipment budget, building budget etc.

The capital expenditure budget is an important budget providing for acquisition of assets, necessitated by the following factors:

(i) Replacement of existing assets.

(ii) Purchase of additional assets to meet a proposed increase in production due to increase in demand.

(iii) Purchase of additional assets because of starting up of new lines of production.

(iv) Installation of an improved type of machinery so as to reduce cost of production.

Thus, the capital expenditure budget enables one to know what new fixed assets are needed and what will be their costs and rates of return.

(ix) Research and Development Cost Budget:

While developing research and development cost budget, it should be clear in mind that work relating to research and development is different from that relating to the manufacturing function. Manufacturing function gives quicker results than research and development which may go on for several years. Therefore, these budgets are established on a long term basis say for 5 to 10 years which can be further subdivided into short-term budgets on annual basis.

As a rule research workers are less cost conscious; so they are not susceptible to strict control. A research and development budget is prepared taking into consideration the research projects in hand and the new research and development projects to be taken up. Thus this budget provides an estimate of the expenditure to be incurred on research and development during the budget period.

After fixation of the research and development cost budget, the research executive fixes priorities for the various research and development projects and submits research and development project authorization forms to the budget committee.

The projects are finally approved by the senior executive. Before giving the approval, the expenditure on research and development is matched against the benefits likely to be availed of from the new object. After the approval of the budget, a close watch is kept on the expenditure so that it may not exceed budget provisions. It is also seen that extent of progress made is commensurate with the expenditure incurred.

(x) Cash (or Financial) Budget:

This budget gives an estimate of the anticipated receipts and payments of cash during the budget period. Therefore, this budget is divided into two parts, one showing the estimated cash receipts on account of cash sales, credit collections and miscellaneous receipts and the other showing the estimated disbursement on account of cash purchases, amount payable to creditors, wages payable to workers, indirect expenses payable, income tax payable, dividend payable, budgeted capital expenditure etc. In short, every factor which affects the receipts and payments of cash is taken into account in the preparation of this budget.

Cash budget makes a provision for a minimum cash balance which will be available at all times. In general, this balance should be equal to one month’s operating expenses plus some provision for contingencies. The minimum balance of cash will help in tiding over adverse conditions of a minor nature. Meanwhile management can make alternative arrangement for additional cash.

This budget is prepared by the Chief Accountant for the guidance of management so that arrangements may be made for the requirements of the organisation.

Advantages of Cash Budget:

Following are the main advantages of preparing cash budget:

(i) It provides an opportunity to review the cash flow for future periods as realistically as possible and make sure that cash is available for revenue and capital expenditure.

(ii) Where adequate amount of cash is not likely to be available during certain periods e.g. when payment of bonus, dividend, tax etc. fall due the company can know in advance so that advance action can be taken to make available the required amount on the most advantageous terms.

(iii) If large surplus of cash is likely to result during certain periods then it will be possible to plan most profitable investment of these funds.

(iv) Preparation of a cash budget by a company will help to plan its cash position in such a way that maximum seasonal discounts can be availed of.

(v) Even for obtaining funds from financial institutions, the system of preparing cash budget helps to convince the bank or other financial institutions about the benefices of the company’s requirements.

(vi) The importance of cash budget may be more in some trades than in others e.g. in trades where there are wide seasonal fluctuations or where long contracts are undertaken.

There are three methods of preparing cash forecasts:

(i) Receipt and Payment Method

(ii) Balance Sheet Forecast Method

(iii) Profit Forecast Method.

(i) Receipt and Payment Method:

This method is useful for forecasting all cash receipts and payments for a short period. Forecasts of cash receipts and payments are made on the basis of the provisions made in the individual functional budgets including the capital expenditure budget and research and development budget. In short, this method of cash forecasts is the same as we have described in the beginning of the discussion on cash budget. Following illustration will make it more clear.

(ii) Balance Sheet Forecast Method:

This method is used for long term forecasting of cash. Forecast of cash is made on the basis of changes in the balance sheet. The opening balance of cash all anticipated changes in the assets and liabilities are added or deducted according to the nature of the time.

Decreases in assets and increases in liabilities are added to the opening balance of cash and increases in assets and decreases in liabilities are deducted from the opening balance of cash. The resulting figure is the estimated cash in hand or cash required at the end of the period.

This method suffers from the following defects:

(a) This method does not take into consideration items of expenses and incomes on the assumption that there is a regular pattern of inflow and outflow of cash.

(b) This method does not give an idea of surplus or deficiency of cash occurring within the budget period because it shows cash in hand or cash required at the end of the budget period.

(iii) Profit Forecast Method:

This method is also helpful for long term forecast of cash and is based on the assumption that it is the profit which makes cash available to the opening balance of cash, estimated net profit adjusted by adding back depreciation (not being outflow of cash), decrease in amount due to stock, bills receivable, debtors, work-in-progress and fixed assets, capital receipts, increase in liabilities and amount received on issue of shares and debentures are added.

Increase in amount due to current assets and fixed assets, decrease in liabilities, dividend payments and prepayments are deducted and the resultant figure will be cash in hand or cash required at the end of the budget period.

This method also has the same drawbacks which balance sheet forecast method has. Of all the three methods, receipt and payment method is the most popular because it shows surplus or deficiency of cash occurring within the budget period.

Standard Costing introduction

Standard Costing is a cost accounting method that involves setting predetermined, standard costs for direct materials, direct labor, and manufacturing overhead. It is used to establish a benchmark for comparing actual costs to expected costs and to identify any variances that may occur during production.

Standard costing, costs are recorded in the accounting system at standard rates, and variances are identified and analyzed to understand the reasons for deviations from the standard. This information is then used to adjust future cost estimates and improve cost control.

Standard costing is commonly used in manufacturing industries where products are produced in large quantities and costs can be accurately predicted based on historical data and experience. It is also used in service industries where costs can be assigned to individual products or services.

Process of Standard Costing:

- Establishing standard costs for direct materials, direct labor, and manufacturing overhead

- Recording actual costs incurred during production

- Calculating and analyzing variances between actual and standard costs

- Investigating and explaining the reasons for variances

- Adjusting future cost estimates based on the information gathered from the analysis.

Advantages of standard costing:

- It helps to identify inefficiencies in production processes.

- It provides a framework for cost control.

- It enables management to identify areas for improvement.

- It facilitates the calculation of variances that can be used for performance evaluation.

- It provides a consistent basis for decision-making.

Disadvantages of Standard Costing:

- It can be time-consuming and expensive to set up.

- It may not accurately reflect the actual costs of production.

- It may not be suitable for businesses that operate in rapidly changing markets.

- It can lead to a focus on cost reduction at the expense of quality and customer service.

- It may not take into account non-financial factors that can impact production costs, such as employee morale and motivation.

The main formulas used in standard costing are:

- Standard Cost per unit = Direct materials standard cost per unit + Direct labor standard cost per unit + Manufacturing overhead standard cost per unit

- Total Standard cost = Standard cost per unit × Number of units produced

- Variance = Actual cost – Standard cost

- Material price variance = (Actual price – Standard price) × Actual quantity

- Material quantity variance = (Actual quantity – Standard quantity) × Standard price

- Labor rate variance = (Actual rate – Standard rate) × Actual hours

- Labor efficiency variance = (Actual hours – Standard hours) × Standard rate

- Overhead spending variance = (Actual overhead – Budgeted overhead) × Actual activity

- Overhead efficiency variance = (Actual activity – Standard activity) × Standard overhead rate.

Standard Costing example question with solution

ABC Ltd. produces and sells widgets. The company’s budgeted production for the year is 10,000 units, with a budgeted overhead of $50,000. The budgeted direct materials and direct labor cost per unit are $20 and $10 respectively. The budgeted fixed overhead per unit is $5. The standard overhead rate per direct labor hour is $5.

During the year, ABC Ltd. produced 9,800 units, and incurred actual overhead of $49,500. The actual direct materials cost was $195,000, while actual direct labor cost was $98,000.

Required:

- Calculate the standard cost per unit for direct materials, direct labor, and overhead.

- Calculate the total standard cost per unit.

- Prepare a standard cost card.

- Calculate the overhead variance and the overhead cost applied.

Solution:

- Calculation of standard cost per unit:

Direct materials cost per unit = Budgeted direct materials cost per unit = $20

Direct labor cost per unit = Budgeted direct labor cost per unit = $10

Variable overhead cost per unit = Standard overhead rate per direct labor hour * Budgeted direct labor hours per unit = $5 * 1 = $5

Fixed overhead cost per unit = Budgeted fixed overhead cost per unit = $5

Total standard cost per unit = Direct materials cost per unit + Direct labor cost per unit + Variable overhead cost per unit + Fixed overhead cost per unit

= $20 + $10 + $5 + $5 = $40

- Calculation of total standard cost per unit:

Total standard cost per unit = Standard cost per unit * Budgeted production per year = $40 * 10,000 = $400,000

- Preparation of standard cost card:

Direct materials: $20 per unit

Direct labor: $10 per unit

Variable overhead: $5 per unit

Fixed overhead: $5 per unit

Total: $40 per unit

- Calculation of overhead variance and overhead cost applied:

Actual overhead = $49,500

Actual direct labor cost = $98,000

Standard overhead rate per direct labor hour = $5

Budgeted direct labor hours = Budgeted production * Budgeted direct labor hours per unit = 10,000 * 1 = 10,000 hours

Overhead cost applied = Standard overhead rate per direct labor hour * Actual direct labor hours

= $5 * 9,800 = $49,000

Overhead variance = Actual overhead – Overhead cost applied

= $49,500 – $49,000 = $500 (favorable)

The favorable variance suggests that the company’s actual overhead cost was less than the overhead cost applied based on the standard rate.

Setting of Standard

Standard costing is a method of accounting that uses standard costs and variances to evaluate performance and control costs. In standard costing, a standard is set for each cost element, such as direct materials, direct labor, and overhead. The standard represents the expected cost for a unit of product or service, based on historical data or estimates.

Setting standards in standard costing is an important process that allows businesses to control costs and evaluate performance. By setting standards for each cost element, businesses can compare actual costs to expected costs and identify variances. Variances may be favorable (actual costs are lower than expected) or unfavorable (actual costs are higher than expected), and can provide insights into areas where cost control measures may be necessary. By analyzing variances and taking corrective action, businesses can improve their performance and profitability.

Steps in setting standards in Standard Costing:

- Identify cost elements:

The first step in setting standards is to identify the cost elements that will be included in the standard cost. This typically includes direct materials, direct labor, and overhead.

- Determine standard quantity and price:

For each cost element, the standard quantity and price are determined. The standard quantity is the amount of a cost element that is required to produce one unit of product or service, while the standard price is the expected cost per unit of the cost element.

- Establish standard costs:

The standard cost for each cost element is calculated by multiplying the standard quantity by the standard price. For example, if the standard quantity for direct materials is 2 pounds per unit and the standard price is $5 per pound, the standard cost for direct materials is $10 per unit.

- Review and update standards:

Standards should be reviewed and updated regularly to ensure they remain accurate and relevant. This includes considering changes in market conditions, technology, and production processes that may affect costs.

Applications of Standard Costing:

-

Budgeting and Forecasting:

Standard costing is integral to the budgeting process, providing a basis for estimating future costs. It helps management forecast the costs of materials, labor, and overheads, which allows for better financial planning and resource allocation. By using standard costs, companies can predict profitability and set realistic financial goals for the upcoming periods.

-

Cost Control:

One of the primary applications of standard costing is in cost control. By comparing actual costs with standard costs, management can identify variances and investigate their causes. Favorable variances indicate cost savings, while unfavorable variances signal inefficiencies or wastage. This helps managers take corrective actions to maintain cost efficiency.

-

Performance Evaluation:

Standard costing helps in evaluating the performance of departments, cost centers, and employees. Managers can assess whether workers and departments are operating efficiently by comparing actual performance with standards. Variances provide insight into areas where performance may need improvement, and they can also be used to reward or penalize employees based on their contributions to cost management.

-

Inventory Valuation:

Standard costs are often used to value inventories in the balance sheet. This simplifies the process of determining the cost of goods sold (COGS) and ending inventory, as actual costs do not need to be tracked continuously. Inventory is recorded at standard cost, and any variances are recognized separately, improving financial reporting efficiency.

-

Pricing Decisions:

Standard costing helps in setting competitive yet profitable prices. By having a clear understanding of the standard cost of producing goods or delivering services, businesses can make informed pricing decisions that cover costs while maintaining profitability. Standard costs provide a baseline for determining the minimum price at which a product should be sold.

-

Variance Analysis:

One of the most significant applications of standard costing is variance analysis. Variances between actual and standard costs are analyzed to understand deviations in material usage, labor efficiency, and overheads. This analysis helps management pinpoint problem areas and make informed decisions to improve efficiency and reduce costs.

-

Motivation and Benchmarking:

Standard costs serve as benchmarks that motivate employees and departments to achieve cost efficiency. When realistic and attainable, standard costs create targets that guide operational activities. Employees strive to meet or beat these standards, driving productivity and cost-saving initiatives across the organization.

Labour Variance

Direct labour variances arise when actual labour costs are different from standard labour costs. In analysis of labour costs, the emphasis is on labour rates and labour hours.

Labour variances constitute the following:

Labour Cost Variance:

Labour cost variance denotes the difference between the actual direct wages paid and the standard direct wages specified for the output achieved.

This variance is calculated by using the following formula:

Labour cost variance = (AH x AR) – (SH x SR)

Where:

AH = Actual hours

AR = Actual rate

SH = Standard hours

SR = Standard rate

Labour Efficiency Variance:

The calculation of labour efficiency or usage variance follows the same pattern as the computation of materials usage variance. Labour efficiency variance occurs when labour operations are more efficient or less efficient than standard performance. If actual direct labour hours required to complete a job differ from the number of standard hours specified, a labour efficiency variance results; it is the difference between actual hours expended and standard labour hours specified multiplied by the standard labour rate per hour.

Labour efficiency variance is computed by applying the following formula:

Labour efficiency variance = (Actual hours – Standard hours for the actual output) x Std. rate per hour.

Assume the following data:

Standard labour hour per unit = 5 hr

Standard labour rate per hour = Rs 30

Units completed = 1,000

Labour cost recorded = 5,050 hrs @ Rs 35

Labour efficiency variance = (5,050-5,000) x Rs 30 = Rs 1,500 (unfavourable) It may be noted that the standard labour hour rate and not the actual rate is used in computing labour efficiency variance. If quantity variances are calculated, changes in prices/rates are excluded, and when price variances are calculated, standard quantities are ignored.

(i) Labour Mix Variance:

Labour mix variance is computed in the same manner as materials mix variance. Manufacturing or completing a job requires different types or grades of workers and production will be complete if labour is mixed according to standard proportion. Standard labour mix may not be adhered to under some circumstances and substitution will have to be made. There may be changes in the wage rates of some workers; there may be a need to use more skilled or expensive types of labour, e.g., employment of men instead of women; sometimes workers and operators may be absent.

These lead to the emergence of a labour mix variance which is calculated by using the following formula:

Labour mix variance = (Actual labour mix – Revised standard labour mix in terms of actual total hours) x Standard rate per hour

(ii) Labour Yield Variance:

The final product cost contains not only material cost but also labour cost. Therefore, gain or loss (higher or lower output than the standard output) should take into account labour yield variance also. A lower output simply means that final output does not correspond with the production units that should have been produced from the hours expended on the inputs.

It can be computed by applying the following formula:

Labour yield variance = (Actual output – Standard output based on actual hours) x Av. Std. Labour Rate per unit of output.

Or

Labour yield variance = (Actual loss – Standard loss on actual hours) x Average standard labour rate per unit of output

Labour yield variance is also known as labour efficiency sub-variance which is computed in terms of inputs, i.e., standard labour hours and revised labour hours mix (in terms of actual hours).

Labour efficiency sub-variance is computed by using the following formula:

Labour efficiency sub-variance = (Revised standard mix – standard mix) x Standard rate

Labour Rate Variance:

Labour rate variance is computed in the same manner as materials price variance. When actual direct labour hour rates differ from standard rates, the result is a labour rate variance. It is that portion of the direct wages variance which is due to the difference between actual rate paid and standard rate of pay specified.

The formula for its calculation is:

Labour rate variance = (Actual rate – Standard rate) x Actual hours

Using data from the example given above, the labour rate variance is Rs 25,250, i.e.,

Labour rate variance = (35 – 30) x 5050 hours = 5 x 5050 = Rs 25,250 (unfavourable)

The number of actual hours worked is used in place of the number of the standard hours specified because the objective is to know the cost difference due to change in labour hour rates, and not hours worked. Favourable rate variances arise whenever actual rates are less than standard rates; unfavourable variances occur when actual rates exceed standard rates.

Idle Time Variance:

Idle time variance occurs when workers are not able to do the work due to some reason during the hours for which they are paid. Idle time can be divided according to causes responsible for creating idle time, e.g., idle time due to breakdown, lack of materials or power failures. Idle time variance will be equivalent to the standard labour cost of the hours during which no work has been done but for which workers have been paid for unproductive time.

Material Variances, Material Price Variance, Material Usage Variance, Material Mix and Yield Variance

Material variances refer to the differences between the standard cost of materials and the actual cost of materials used in production. These variances help management identify whether material costs are being controlled effectively and determine the reasons for deviations from standards.

A material variance may be:

- Favourable (F): Actual cost is less than standard cost.

- Adverse or Unfavourable (A): Actual cost is more than standard cost.

Material variance analysis is an important part of standard costing because materials generally constitute a significant portion of production costs.

Material Cost Variance (MCV)

Material Cost Variance (MCV) is the difference between the standard cost of materials that should have been incurred for actual production and the actual cost of materials consumed during production.

It measures the overall effect of differences in:

- Material prices, and

- Material quantities used.

Material Cost Variance is one of the most important variances in standard costing because it helps management determine whether material costs are being controlled effectively.

Definition

Material Cost Variance is the difference between:

Standard Cost of Materials – Actual Cost of Materials

This can be computed by using the following formula:

Where:

- SQ = Standard Quantity

- SP = Standard Price

- AQ = Actual Quantity

- AP = Actual Price

Alternative Formula

MCV = Material Price Variance + Material Usage Variance

or

MCV = MPV + MUV

Interpretation of MCV

Favourable Variance (F)

When:

Standard Cost > Actual Cost

This means the company spent less than expected.

Adverse or Unfavourable Variance (A)

When:

Actual Cost > Standard Cost

This means the company spent more than expected.

Example 1

Standard Data

- Standard Quantity = 100 kg

- Standard Price = ₹20 per kg

Standard Cost:

100 × 20 = ₹2,000

Actual Data

- Actual Quantity = 110 kg

- Actual Price = ₹22 per kg

Actual Cost:

110 × 22 = ₹2,420

Material Cost Variance

MCV = ₹2,000 − ₹2,420

Thus, the company incurred an Adverse Material Cost Variance of ₹420.

Example 2

Standard Data

- Standard Quantity = 500 kg

- Standard Price = ₹15 per kg

Standard Cost:

500 × 15 = ₹7,500

Actual Data

- Actual Quantity = 480 kg

- Actual Price = ₹14 per kg

Actual Cost:

480 × 14 = ₹6,720

Material Cost Variance

MCV = ₹7,500 − ₹6,720

Thus, the company earned a Favourable Material Cost Variance of ₹780.

Material Usage Variance

The material quantity or usage variance results when actual quantities of raw materials used in production differ from standard quantities that should have been used to produce the output achieved. It is that portion of the direct materials cost variance which is due to the difference between the actual quantity used and standard quantity specified.

As a formula, this variance is shown as:

Materials quantity variance = (Actual Quantity – Standard Quantity) x Standard Price

A material usage variance is favourable when the total actual quantity of direct materials used is less than the total standard quantity allowed for the actual output.

Causes of Favourable Material Cost Variance

- Purchase of materials at lower prices.

- Efficient use of materials.

- Reduction in material wastage.

- Bulk purchase discounts.

- Better purchasing policies.

- Improved production methods.

- Efficient supervision.

- Use of substitute materials at lower costs.

Causes of Adverse Material Cost Variance

- Increase in market prices.

- Excessive material consumption.

- Poor quality materials.

- Inefficient labour.

- Machine breakdowns.

- Production defects.