by

by Material variances refer to the differences between the standard cost of materials and the actual cost of materials used in production. These variances help management identify whether material costs are being controlled effectively and determine the reasons for deviations from standards.

A material variance may be:

- Favourable (F): Actual cost is less than standard cost.

- Adverse or Unfavourable (A): Actual cost is more than standard cost.

Material variance analysis is an important part of standard costing because materials generally constitute a significant portion of production costs.

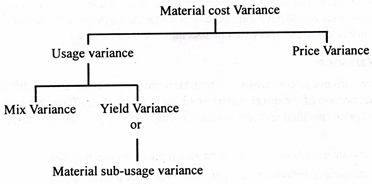

Material Cost Variance (MCV)

Material Cost Variance (MCV) is the difference between the standard cost of materials that should have been incurred for actual production and the actual cost of materials consumed during production.

It measures the overall effect of differences in:

- Material prices, and

- Material quantities used.

Material Cost Variance is one of the most important variances in standard costing because it helps management determine whether material costs are being controlled effectively.

Definition

Material Cost Variance is the difference between:

Standard Cost of Materials – Actual Cost of Materials

This can be computed by using the following formula:

Where:

- SQ = Standard Quantity

- SP = Standard Price

- AQ = Actual Quantity

- AP = Actual Price

Alternative Formula

MCV = Material Price Variance + Material Usage Variance

or

MCV = MPV + MUV

Interpretation of MCV

Favourable Variance (F)

When:

Standard Cost > Actual Cost

This means the company spent less than expected.

Adverse or Unfavourable Variance (A)

When:

Actual Cost > Standard Cost

This means the company spent more than expected.

Example 1

Standard Data

- Standard Quantity = 100 kg

- Standard Price = ₹20 per kg

Standard Cost:

100 × 20 = ₹2,000

Actual Data

- Actual Quantity = 110 kg

- Actual Price = ₹22 per kg

Actual Cost:

110 × 22 = ₹2,420

Material Cost Variance

MCV = ₹2,000 − ₹2,420

Thus, the company incurred an Adverse Material Cost Variance of ₹420.

Example 2

Standard Data

- Standard Quantity = 500 kg

- Standard Price = ₹15 per kg

Standard Cost:

500 × 15 = ₹7,500

Actual Data

- Actual Quantity = 480 kg

- Actual Price = ₹14 per kg

Actual Cost:

480 × 14 = ₹6,720

Material Cost Variance

MCV = ₹7,500 − ₹6,720

Thus, the company earned a Favourable Material Cost Variance of ₹780.

Material Usage Variance

The material quantity or usage variance results when actual quantities of raw materials used in production differ from standard quantities that should have been used to produce the output achieved. It is that portion of the direct materials cost variance which is due to the difference between the actual quantity used and standard quantity specified.

As a formula, this variance is shown as:

Materials quantity variance = (Actual Quantity – Standard Quantity) x Standard Price

A material usage variance is favourable when the total actual quantity of direct materials used is less than the total standard quantity allowed for the actual output.

Causes of Favourable Material Cost Variance

- Purchase of materials at lower prices.

- Efficient use of materials.

- Reduction in material wastage.

- Bulk purchase discounts.

- Better purchasing policies.

- Improved production methods.

- Efficient supervision.

- Use of substitute materials at lower costs.

Causes of Adverse Material Cost Variance

- Increase in market prices.

- Excessive material consumption.

- Poor quality materials.

- Inefficient labour.

- Machine breakdowns.

- Production defects.

- Failure to obtain discounts.

- Material theft or wastage.

Importance of Material Cost Variance

- Helps control material costs.

- Measures purchasing efficiency.

- Evaluates production efficiency.

- Identifies wastage and losses.

- Improves resource utilization.

- Assists managerial decision-making.

- Facilitates cost reduction.

- Strengthens budgetary control.

- Improves profitability.

- Supports performance evaluation.

Material Mix Variance

Material Mix Variance (MMV) is the portion of Material Usage Variance that arises because the actual proportion of materials used differs from the standard proportion or mix.

It is applicable when two or more materials are mixed together to produce a finished product. If the actual combination of materials differs from the standard combination, a material mix variance occurs.

Material Mix Variance helps management determine whether changes in the composition of materials have increased or reduced production costs.

Definition

Material Mix Variance is the difference between:

The cost of the Revised Standard Mix and the cost of the Actual Mix at standard prices.

Formula

MMV = ∑SP(RSQ−AQ)

Where:

- SP = Standard Price

- RSQ = Revised Standard Quantity

- AQ = Actual Quantity

Alternative Formula

MMV = Revised Standard Cost − Actual Mix Cost at Standard Prices

Calculation of Revised Standard Quantity (RSQ)

RSQ = (Total Actual Quantity / Total Standard Quantity) × Standard Quantity of each material

Interpretation

Favourable Variance (F)

When the actual mix is cheaper or more economical than the standard mix.

Adverse Variance (A)

When the actual mix is more expensive than the standard mix.

Example

Standard Mix

| Material | Quantity | Price per kg | Cost |

|---|---|---|---|

| A | 60 kg | ₹10 | ₹600 |

| B | 40 kg | ₹20 | ₹800 |

| Total | 100 kg | ₹1,400 |

Actual Mix

| Material | Quantity |

|---|---|

| A | 50 kg |

| B | 50 kg |

| Total | 100 kg |

Step 1: Calculate Revised Standard Quantity

Since the total actual quantity is equal to the total standard quantity, the Revised Standard Quantity is:

| Material | RSQ |

|---|---|

| A | 60 kg |

| B | 40 kg |

Step 2: Calculate Material Mix Variance

Material A

MMV = 10(60 − 50)

Material B

MMV = 20(40−50)

Total Material Mix Variance

MMV = ₹100(F) − ₹200(A)

Therefore, the Material Mix Variance is ₹100 Adverse.

Another Illustration

Standard Mix

| Material | Quantity | Price |

|---|---|---|

| X | 80 kg | ₹5 |

| Y | 20 kg | ₹15 |

Actual Mix

| Material | Quantity |

|---|---|

| X | 70 kg |

| Y | 30 kg |

Calculation

For X:

5(80−70) = ₹50(F)

For Y:

15(20−30) = ₹150(A)

Total:

MMV=₹50(F)−₹150(A)

Causes of Material Mix Variance

1. Shortage of Materials

Certain materials may not be available, forcing the company to use substitutes.

2. Price Changes

A company may change the mix to reduce material costs.

3. Poor Quality Materials

Inferior materials may require additional quantities of other materials.

4. Change in Production Methods

Production techniques may require a different material combination.

5. Purchasing Decisions

The purchase department may buy alternative materials.

6. Technical Reasons

Engineers may recommend changes in material composition.

7. Human Errors

Incorrect mixing of materials may create variances.

8. Change in Product Specifications

Customer requirements may lead to changes in the standard mix.

Relationship with Material Usage Variance

MUV = MMV + MYV

Where:

- MMV = Material Mix Variance

- MYV = Material Yield Variance

Importance of Material Mix Variance

- Helps control material composition.

- Measures efficiency in mixing materials.

- Identifies uneconomical material substitutions.

- Assists in cost reduction.

- Improves production planning.

- Helps evaluate purchasing decisions.

- Improves resource utilization.

- Supports managerial decision-making.

- Increases profitability.

- Strengthens cost control.

Advantages of Material Mix Variance Analysis

- Detects inefficient material combinations.

- Improves quality control.

- Reduces material costs.

- Facilitates performance evaluation.

- Improves production efficiency.

- Helps in variance investigation.

- Encourages economical use of materials.

- Enhances profitability.

Limitations of Material Mix Variance

- Applicable only where multiple materials are mixed.

- Requires detailed records.

- Time-consuming calculations.

- Depends on accurate standards.

- Ignores external market conditions.

- Difficult in highly customized production.

Materials Yield Variance

Materials yield variance explains the remaining portion of the total materials quantity variance. It is that portion of materials usage variance which is due to the difference between the actual yield obtained and standard yield specified (in terms of actual inputs). In other words, yield variance occurs when the output of the final product does not correspond with the output that could have been obtained by using the actual inputs. In some industries like sugar, chemicals, steel, etc. actual yield may differ from expected yield based on actual input resulting into yield variance.

The total of materials mix variance and materials yield variance equals materials quantity or usage variance. When there is no materials mix variance, the materials yield variance equals the total materials quantity variance. Accordingly, mix and yield variances explain distinct parts of the total materials usage variance and are additive.

The formula for computing yield variance is as follows:

Yield Variance = (Actual yield – Standard Yield specified) x Standard cost per unit

Materials Price Variance

A materials price variance occurs when raw materials are purchased at a price different from standard price. It is that portion of the direct materials which is due to the difference between actual price paid and standard price specified and cost variance multiplied by the actual quantity. Expressed as a formula,

Materials price variance = (Actual price – Standard price) x Actual quantity

Materials price variance is un-favourable when the actual price paid exceeds the predetermined standard price. It is advisable that materials price variance should be calculated for materials purchased rather than materials used. Purchase of materials is an earlier event than the use of materials.

Therefore, a variance based on quantity purchased is basically an earlier report than a variance based on quantity actually used. This is quite beneficial from the viewpoint of performance measurement and corrective action. An early report will help the management in measuring the performance so that poor performance can be corrected or good performance can be expanded at an early date.

Recognizing material price variances at the time of purchase lets the firm carry all units of the same materials at one price—the standard cost of the material, even if the firm did not purchase all units of the materials at the same price. Using one price for the same materials facilities management control and simplifies accounting work.

If a direct materials price variance is not recorded until the materials are issued to production, the direct materials are carried on the books at their actual purchase prices. Deviations of actual purchase prices from the standard price may not be known until the direct materials are issued to production.

2 thoughts on “Material Variances, Material Price Variance, Material Usage Variance, Material Mix and Yield Variance”