Keynesian liquidity preference theory of interest

by

by The Liquidity Preference Theory says that the demand for money is not to borrow money but the desire to remain liquid. In other words, the interest rate is the ‘price’ for money.

John Maynard Keynes created the Liquidity Preference Theory in to explain the role of the interest rate by the supply and demand for money. According to Keynes, the demand for money is split up into three types; Transactionary, Precautionary and Speculative.

He also said that money is the most liquid asset and the more quickly an asset can be converted into cash, the more liquid it is.

In macroeconomic theory, liquidity preference is the demand for money, considered as liquidity. The concept was first developed by John Maynard Keynes in his book The General Theory of Employment, Interest and Money (1936) to explain determination of the interest rate by the supply and demand for money. The demand for money as an asset was theorized to depend on the interest foregone by not holding bonds (here, the term “bonds” can be understood to also represent stocks and other less liquid assets in general, as well as government bonds). Interest rates, he argues, cannot be a reward for saving as such because, if a person hoards his savings in cash, keeping it under his mattress say, he will receive no interest, although he has nevertheless refrained from consuming all his current income. Instead of a reward for saving, interest, in the Keynesian analysis, is a reward for parting with liquidity. According to Keynes, money is the most liquid asset. Liquidity is an attribute to an asset. The more quickly an asset is converted into money the more liquid it is said to be.

According to Keynes, demand for liquidity is determined by three motives:

- The transactions motive: people prefer to have liquidity to assure basic transactions, for their income is not constantly available. The amount of liquidity demanded is determined by the level of income: the higher the income, the more money demanded for carrying out increased spending.

- The precautionary motive: people prefer to have liquidity in the case of social unexpected problems that need unusual costs. The amount of money demanded for this purpose increases as income increases.

- Speculative motive: people retain liquidity to speculate that bond prices will fall. When the interest rate decreases people demand more money to hold until the interest rate increases, which would drive down the price of an existing bond to keep its yield in line with the interest rate. Thus, the lower the interest rate, the more money demanded (and vice versa).

The Transactions Demand for Money:

The transactions demand for money arises from the medium of exchange function of money in making regular payments for goods and services. According to Keynes, it relates to “the need of cash for the current transactions of personal and business exchange.” It is further divided into income and business motives.

The income motive is meant “to bridge the interval between the receipt of income and its disbursement.” Similarly, the business motive is meant “to bridge the interval between the time of incurring business costs and that of the receipt of the sale proceeds.”

If the time between the incurring of expenditure and receipt of income is small, less cash will be held by the people for current transactions, and vice versa. There will, however, be changes in the transactions demand for money depending upon the expectations of income recipients and businessmen. They depend upon the level of income, the interest rate, the business turnover, the normal period between the receipt and disbursement of income, etc.

Given these factors, the transactions demand for money is a direct proportional and positive function of the level of income, and is expressed as L=kY

where LT is the transactions demand for money, k is the proportion of income which is kept for transactions purposes, and Y is the income.

The Precautionary Demand for Money:

The precautionary motive relates to “the desire to provide for contingencies requiring sudden expenditures and for unforeseen opportunities of advantageous purchases.” Both individuals and businessmen keep cash in reserve to meet unexpected needs. Individuals hold some cash to provide for illness, accidents, unemployment and other unforeseen contingencies.

Similarly, businessmen keep cash in reserve to tide over unfavourable conditions or to gain from unexpected deals. Therefore, “money held under the precautionary motive is rather like water kept in reserve in a water tank.” The precautionary demand for money depends upon the level of income, business activities, opportunities for unexpected profitable deals, availability of cash, the cost of holding liquid assets in bank reserves, etc.

Keynes held that the precautionary demand for money, like transactions demand, was a function of the level of income. But the post-Keynesian economists believe that like transactions demand, it is inversely related to high interest rates.

The transactions and precautionary demand for money will be unstable, particularly if the economy is not at full employment level and transactions are, therefore, less than the maximum, and are liable to fluctuate up or down. Since precautionary demand, like transactions demand is a function of income and interest rates, the demand for money for these two purposes is expressed in the single equation LT = f (Y,r).

The Speculative Demand for Money:

The speculative (or asset or liquidity preference) demand for money is “for securing profit from knowing better than the market what the future will bring forth”. Individuals and businessmen having funds, after keeping enough for transactions and precautionary purposes, like to make a speculative gain by investing in bonds. Money held for speculative purposes is a liquid store of value which can be invested at an opportune moment in interest-bearing bonds or securities.

Liquidity Trap:

Keynes visualised conditions in which the speculative demand for money would be highly or even totally elastic so that changes in the quantity of money would be fully absorbed into speculative balances. This is the famous Keynesian liquidity trap. In this case, changes in the quantity of money have no effects at all on prices or income.

According to Keynes, this is likely to happen when the market interest rate is very low so that yields on bonds, equities and other securities will also below.

At a very low rate of interest, such as r2, in Figure 5, the Ls curve becomes perfectly elastic and the speculative demand for money is infinitely elastic. This portion of the Ls curve is known as the liquidity trap. At such a low rate, people prefer to keep money in cash rather than invest in bonds because purchasing bonds will mean a definite loss. People will not buy bonds so long as the interest rate remains at the low level and they will be waiting for the rate of interest to return to the “normal” level and bond prices to fall.

According to Keynes, as the rate of interest approaches zero, the risk of loss in holding bonds becomes greater. “When the price of bonds has been bid up so high that the rate of interest is, say, only 2 per cent or less, a very small decline in the price of bonds will wipe out the yield entirely and a slightly further decline would result in loss of the part of the principal.” Thus, the lower the interest rate, the smaller the earnings from bonds. Therefore, the greater the demand for cash holdings. Consequently, the Ls curve will become perfectly elastic.

Further, according to Keynes, “a long-term rate of interest of 2 per cent leaves more to fear than to hope, and offers, at the same time, a running yield which is only sufficient to offset a very small measure of fear.” This makes the Ls curve “virtually absolute in the sense that almost everybody prefers cash to holding a debt which yields so low a rate of interest.”

Prof. Modigliani believes that an infinitely elastic Ls curve is possible in a period of great uncertainty when price reductions are anticipated and the tendency to invest in bonds decreases, or if there prevails “a real scarcity of investment outlets that are profitable at rates of interest higher than the institutional minimum.”

The phenomenon of liquidity trap possesses certain important implications:

First, the monetary authority cannot influence the rate of interest even by following a cheap money policy. An increase in the quantity of money cannot lead to a further decline in the rate of interest in a liquidity trap situation.

Second, the rate of interest cannot fall to zero.

Third, the policy of a general wage cut cannot be efficacious in the face of a perfectly elastic liquidity preference curve, such as Ls in Figure 5. No doubt, a policy of general wage cut would lower wages and prices, and thus release money from transactions to speculative purpose, the rate of interest would remain unaffected because people would hold money due to the prevalent uncertainty in the money market.

Last, if new money is created, it instantly goes into speculative balances and is put into bank vaults or cash boxes instead of being invested. Thus there is no effect on income. Income can change without any change in the quantity of money. Thus, monetary changes have a weak effect on economic activity under conditions of absolute liquidity preference.

The Total Demand for Money:

According to Keynes, money held for transactions and precautionary purposes is primarily a function of the level of income, LT =f (Y), and the speculative demand for money is a function of the rate of interest, Ls = f (r). Thus the total demand for money is a function of both income and the interest rate:

LT+Ls =f (Y)+f (r)

or L =f(Y)+f (r)

or L =f(Y,r)

where L represents the total demand for money. Thus the total demand for money can be derived by the lateral summation of the demand function for transactions and precautionary purposes and the demand function for speculative purposes, as illustrated in Figure 6 (A), (B) and (C). Panel (A) of the Figure shows OT, the transactions and precautionary demand for money at Y level of income and different rates of interest. Panel (B) shows the speculative demand for money at various rates of interest.

It is an inverse function of the rate of interest. For instance, at r. rate of interest it is OS and as the rate of interest falls to r2, the Ls curve becomes perfectly elastic. Panel (C) shows the total demand curve for money L which is a lateral summation of LT and Ls curves: L=LT+LS. For example, at r rate of interest, the total demand for money is OD which is the sum of transactions and precautionary demand OT plus the speculative demand TD, OD=OT+TD, where TD = OS. At r2 interest rate, the total demand for money curve also becomes perfectly elastic, showing the position of liquidity trap.

Criticisms

In Man, Economy, and State (1962), Murray Rothbard argues that the liquidity preference theory of interest suffers from a fallacy of mutual determination. Keynes alleges that the rate of interest is determined by liquidity preference. In practice, however, Keynes treats the rate of interest as determining liquidity preference. Rothbard states “The Keynesians therefore treat the rate of interest, not as they believe they do as determine by liquidity preference but rather as some sort of mysterious and unexplained force imposing itself on the other elements of the economic system.”

Criticism emanates also from post-Keynesian economists, such as circuitist Alain Parguez, professor of economics, University of Besançon, who “reject[s] the keynesian liquidity preference theory … but only because it lacks sensible empirical foundations in a true monetary economy”.

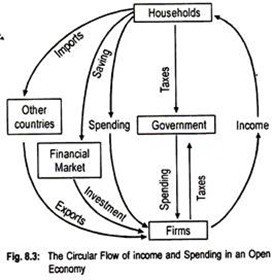

g. 8.3. Adding (X – M) in the above equation, we get

g. 8.3. Adding (X – M) in the above equation, we get