Different aspects of Strategic cost Management

by

by Strategic cost management initiative is taken at the top and a dedicated team should be involved in the whole process of formulation, implementation and monitoring process.

A control standard is a target against which subsequent performance will be compared. Standards are the criteria that enable managers to evaluate future, current, or past actions. They are measured in a variety of ways, including physical, quantitative, and qualitative terms. Five aspects of the performance can be managed and controlled: quantity, quality, time, cost, and behavior.

Organization should have its own policy regarding recording and reporting of following information:

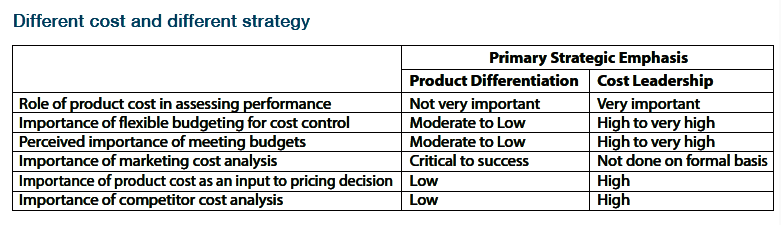

- Choice of strategic positioning, cost leadership or product differentiation;

- Choice of cost drivers, structural or executional;

- Cost reduction strategies with reference to value analysis;

- Value chain related activities;

- Periodic evaluation report;

- Strategic cost management framework for the firm

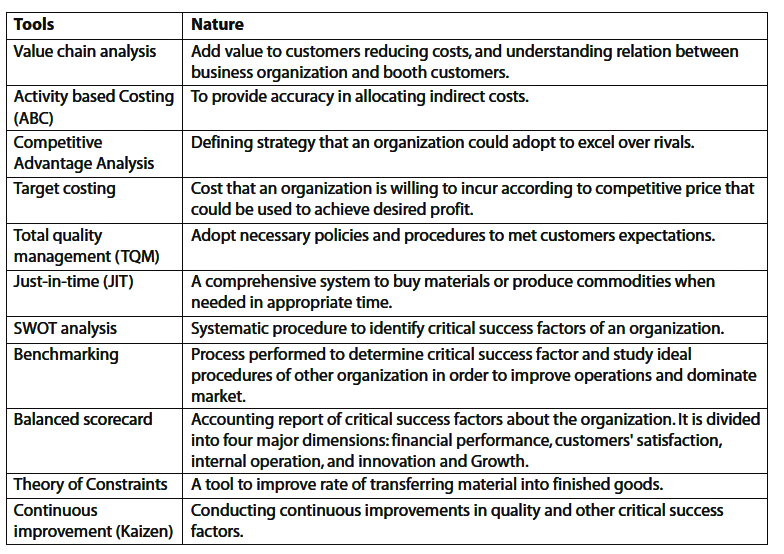

- List of tools applied by the firm as a part of strategic cost management.

- Any other types of reporting as required.

Effective control systems tend to have certain qualities in common. These can be stated thus:

- Suitable: The control system must be suitable to the needs of an organisation. It must conform to the nature and needs of the job and the area to be controlled. For example, the control system used in production department will be different from that used in sales department.

- Simple: The control system should be easy to understand and operate. A complicated control system will cause unnecessary mistakes, confusion and frustration among employees. When the control system is understood properly, employees can interpret the same in a right way and ensure its implementation.

- Selective: To be useful, the control system must focus attention on key, strategic and important factors which are critical to performance. Insignificant deviations need not be looked into. By concentrating attention on important aspects, managers can save their time and meet problems head-on in an effective manner.

- Sound and economical: The system of control should be economical and easy to maintain. Any system of control has to justify the benefits that it gives in relation to the costs it incurs. To minimize costs, management should try to impose the least amount of control that is necessary to produce the desired results.

- Flexible: Competitive, technological and other environmental changes force organizations to change their plans. As a result, control should be necessarily flexible. It must be flexible enough to adjust to adverse changes or to take advantage of new opportunities.

- Forward-looking: An effective control system should be forward-looking. It must provide timely information on deviations. Any departure from the standard should be caught as soon as possible. This helps managers to take remedial steps immediately before things go out of gear.

- Reasonable: According to Robbins, controls must be reasonable. They must be attainable. If they are too high or unreasonable, they no longer motivate employees. On the other hand, when controls are set at low levels, they do not pose any challenge to employees. They do not stretch their talents. Therefore, control standards should be reasonable they should challenge and stretch people to reach higher performance without being demotivating.

- Objective: A control system would be effective only when it is objective and impersonal. It should not be subjective and arbitrary. When standards are set in clear terms, it is easy to evaluate performance. Vague standards are not easily understood and hence, not achieved in a right way. Controls should be accurate and unbiased. If they are unreliable and subjective, people will resent them.

- Responsibility for failures: An effective control system must indicate responsibility for failures.

Detecting deviations would be meaningless unless one knows where in the organisation they are occurring and who is responsible for them. The control system should also point out what corrective actions are needed to keep actual performance in line with planned performance.

- Acceptable: Controls will not work unless people want them to. They should be acceptable to chose to whom they apply, controls will be acceptable when they are:

- Quantified

- Objective

- Attainable

- Understood by everyone

Features

Allows for Risk Management

Risk management can be considered as a subset or a specific form of strategic management. Risk is the probability of a future loss and risk management involves formulating various strategies to combat the risks making risk management a form or variety of strategic management.

Strategic management in this form allows for identifying and eliminating the risks posed by various hazards to the business.

Conscious Process

Strategies are a product of the developed conscience and intellect that we humans proudly possess and employ. Strategic management implies the usage of the brain and the heart and is not a routine ever-continuing process. It requires great skill and experience to be carried out effectively and requires a full application of one’s conscience.

Requires Foresight

The future is uncertain. We cannot predict what will happen. However, on the basis of the information that is available to us, we will be able to presume certain things about the future.

For instance, a discovery that the item XYZ causes cancer can allow us to make a very reasonable presumption that the item XYZ will be banned in the near future. This presumption thus allows us to not make any investment in anything directly related to XYZ.

Drives Innovation

The development of strategy is not a simple process and requires making the best out of often very restrictive situations. This drives innovations and allows managers to approach problems from different angles and solve problems more efficiently. After all, necessity is the mother of all inventions.

Strategic Management as a process is quite complicated and requires years of experience and inherent skills to be carried out efficiently. The process is pervasive and is central to any business. It is a discipline in itself and requires more study for enthusiasts wanting to pursue management.

Goal-Oriented Process

The process of Strategic Management is a goal-oriented process. The process is done with the intention and goal of analyzing the various elements through SWOT analysis and other tools and to develop a plan or strategy that effectively allows the business to maneuver itself around every hurdle and make use of its strength.

This process also plays the role of making all other functions of the business goal-oriented as well.

Facilitates decision making

Strategic Management plays an integral role in making important decisions. Whenever a manager has to make a decision he has to think about the bearing of such a decision on the overall strategy and the business’ trajectory.

Thus, the strategies developed to act as a guide to making efficient and accurate decisions.

Primary Process

Strategic Management is the primary process in any business. The strategies that the business has to apply in its activities is developed at the initial stage itself and only after the creation of the strategy that other processes commence by making the strategy as its basis.

Pervasive Process

Strategic Management is a pervasive process seen in all levels of the business.

The core strategies are formulated for the entire business by the top-level management and strategies to efficiently achieve the overall goal so laid down by the top-level management is developed through the various lower business units.

Dependent on Personal Qualities

The above two considerations make it amply clear that Strategic Management is heavily dependent on the personal qualities of the managers occupying the top-level positions.

These personal qualities including skills and experience obtained over years of employment and observation cannot be imparted by training or coaching classes and require practical exposure for extended periods of time unless the person is born with the talent of strategizing (which is rare).