Dividend Discount Model (DDM) is a stock valuation method used to estimate the intrinsic value of a company’s share based on the present value of its expected future dividends. The model assumes that the value of a share is equal to the total present value of all future dividend payments received by shareholders. Since dividends represent the cash flow earned from owning a share, they are discounted to their present value using the required rate of return. The Dividend Discount Model is most suitable for companies that pay regular and stable dividends. Investors use DDM to determine whether a stock is undervalued or overvalued by comparing its intrinsic value with its current market price, thereby supporting informed investment decisions.

Types of Dividend Discount Model

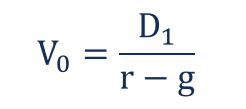

1. Gordon Growth Model (Costant)

The Gordon Growth Model (GGM) is one of the most commonly used variations of the dividend discount model. The model is called after American economist Myron J. Gordon, who proposed the variation.

The GGM is based on the assumptions that the stream of future dividends will grow at some constant rate in future for an infinite time. Mathematically, the model is expressed in the following way:

Where:

- V0 – the current fair value of a stock

- D1 – the dividend payment in one period from now

- r – the estimated cost of equity capital (usually calculated using CAPM)

- g – the constant growth rate of the company’s dividends for an infinite time

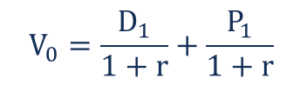

2. One-period Dividend Discount Model

The one-period discount dividend model is used much less frequently than the Gordon Growth model. The former is applied when an investor wants to determine the intrinsic price of a stock that he or she will sell in one period from now. The one-period dividend discount model uses the following equation:

Where:

- V0 – the current fair value of a stock

- D1 – the dividend payment in one period from now

- P1 – the stock price in one period from now

- r – the estimated cost of equity capital

3. Multi-period Dividend Discount Model

The multi-period dividend discount model is an extension of the one-period dividend discount model wherein an investor expects to hold a stock for the multiple periods. The main challenge of the multi-period model variation is that forecasting dividend payments for different periods is required. The model’s mathematical formula is below:

Assumption of Dividend Discount Model

- Regular Dividend Payments

The Dividend Discount Model assumes that the company pays dividends regularly to its shareholders. Since the model values a share based on future dividend payments, companies that do not distribute dividends cannot be accurately valued using this method. Regular dividend payments provide a predictable stream of cash flows that can be discounted to determine the intrinsic value of the share. Therefore, the model is most suitable for established companies with a consistent dividend policy. Stable dividend payments enable investors to estimate future returns more accurately and make reliable investment decisions using the Dividend Discount Model.

- Constant Dividend Growth Rate

The Dividend Discount Model assumes that dividends grow at a constant rate every year. This assumption is particularly important in the constant growth version of the model, also known as the Gordon Growth Model. It assumes that the company’s earnings and dividend payments increase steadily over the long term. A constant growth rate simplifies the valuation process and allows investors to estimate the present value of future dividends. Although actual dividend growth may fluctuate, the model assumes long term stability. This assumption is most appropriate for mature companies with stable earnings and predictable dividend growth patterns.

- Required Rate of Return Remains Constant

The model assumes that the investor’s required rate of return remains constant throughout the investment period. The required rate of return reflects the minimum return expected by investors for the level of risk associated with the investment. It is used as the discount rate to calculate the present value of future dividends. A constant discount rate simplifies the valuation process and ensures consistency in calculations. Changes in interest rates, market conditions, or business risk are not considered under this assumption. Therefore, the model works best when the required return remains relatively stable over time.

- Growth Rate is Lower than the Required Rate of Return

The Dividend Discount Model assumes that the dividend growth rate is always lower than the required rate of return. This condition ensures that the mathematical formula produces a meaningful and positive share value. If the growth rate becomes equal to or greater than the required return, the model cannot calculate a valid intrinsic value. In practice, mature companies generally experience sustainable growth rates that remain below investors’ required returns. This assumption makes the model suitable for stable businesses with moderate long term growth rather than rapidly growing companies with highly uncertain future earnings and dividend patterns.

The Dividend Discount Model assumes that the capital market operates efficiently, meaning that investors have equal access to relevant information and securities are fairly priced based on available data. It also assumes that share prices eventually reflect the intrinsic value determined by expected future dividends. Although short term market prices may fluctuate due to investor sentiment or temporary factors, the model assumes that prices move toward their fair value over time. This assumption allows investors to compare the calculated intrinsic value with the current market price and identify undervalued or overvalued shares for investment decisions.

Importance of Dividend Discount Model

- Helps in Determining Cost of Equity Capital

The Dividend Discount Model (DDM) is widely used to calculate the cost of equity capital. It estimates the return expected by shareholders based on future dividends and dividend growth. This information helps financial managers determine the minimum return that must be earned on investments financed through equity funds. Accurate estimation of the cost of equity is essential for making sound financial decisions and maintaining shareholder satisfaction. By providing a clear measure of shareholder expectations, the DDM supports effective capital budgeting and financial planning while ensuring that the company creates value for its owners.

- Assists in Share Valuation

One of the major importance of the Dividend Discount Model is its ability to estimate the intrinsic value of a company’s shares. The model calculates share value by discounting expected future dividends to their present value. Investors compare this intrinsic value with the current market price to determine whether a stock is overvalued or undervalued. This helps them make informed investment decisions. Companies and analysts also use the model for valuation purposes during mergers, acquisitions, and investment analysis. Thus, DDM serves as a useful tool for determining the fair worth of equity shares.

- Supports Investment Decision-Making

The Dividend Discount Model provides valuable information for evaluating investment opportunities. Investors use the model to identify stocks that offer attractive returns relative to their market prices. If the intrinsic value calculated through DDM exceeds the market price, the stock may be considered a good investment. Similarly, financial managers use the model to assess whether equity-financed projects can generate sufficient returns. By offering a systematic approach to evaluating investments, the model reduces uncertainty and improves the quality of financial decisions. This contributes to better resource allocation and enhanced profitability.

- Facilitates Capital Budgeting Decisions

Capital budgeting involves selecting projects that maximize shareholder wealth. The Dividend Discount Model helps determine the cost of equity, which serves as an important component of the discount rate used in capital budgeting techniques such as Net Present Value (NPV). By providing an estimate of shareholder-required returns, the model helps management evaluate whether proposed investments are financially viable. Projects generating returns above the cost of equity are generally accepted, while those generating lower returns are rejected. Therefore, DDM contributes to efficient investment appraisal and supports long-term financial growth.

- Reflects Shareholder Expectations

The Dividend Discount Model is based on dividends, which represent the actual cash returns received by shareholders. As a result, the model closely reflects investor expectations regarding future income and growth. Understanding these expectations is important for companies seeking to attract and retain investors. By considering expected dividends and growth rates, DDM provides insight into the returns shareholders require for bearing investment risk. This feature enables management to align financial strategies with investor interests and maintain confidence in the company’s performance and future prospects.

- Useful in Financial Planning

Financial planning requires accurate estimates of financing costs and future capital requirements. The Dividend Discount Model helps managers forecast the cost of equity and assess the impact of dividend policies on shareholder value. By understanding how dividend payments and growth rates affect equity costs, companies can design effective financing strategies. The model also assists in determining whether retained earnings or external equity financing should be used for future investments. Consequently, DDM contributes to comprehensive financial planning and helps organizations achieve their long-term objectives while maintaining financial stability.

- Encourages Dividend Policy Evaluation

Dividend policy plays a significant role in determining shareholder returns and company valuation. The Dividend Discount Model highlights the relationship between dividends, growth, and share value. This encourages management to evaluate dividend policies carefully and understand their impact on investor perceptions. Companies can use the model to analyze how changes in dividend payouts affect the cost of equity and market valuation. Such analysis helps management formulate dividend policies that balance shareholder expectations with business financing needs. Therefore, DDM serves as an important tool for dividend decision-making and corporate financial management.

- Enhances Wealth Maximization Objective

The primary financial objective of a company is the maximization of shareholder wealth. The Dividend Discount Model contributes to this objective by helping management identify investments and financing decisions that increase share value. By estimating intrinsic stock value and cost of equity, the model ensures that resources are allocated to projects capable of generating adequate returns. It also helps investors make rational investment choices that maximize their wealth. Through better valuation, investment analysis, and financial planning, DDM supports value creation and strengthens the company’s ability to achieve sustainable growth and long-term shareholder prosperity.

Limitations of Dividend Discount Model

- Applicable Only to Dividend-Paying Companies

One of the major limitations of the Dividend Discount Model (DDM) is that it can only be applied to companies that regularly pay dividends. Many growing companies, especially startups and technology firms, prefer to retain earnings for expansion rather than distribute dividends. In such cases, the model becomes ineffective because future dividends cannot be estimated. As a result, investors cannot use DDM to determine the value of shares or calculate the cost of equity. This restricts its applicability and makes it unsuitable for a large number of companies operating in modern financial markets.

- Assumption of Constant Dividend Growth

The Dividend Discount Model assumes that dividends will grow at a constant rate indefinitely. In reality, companies experience fluctuations in earnings, economic conditions, competition, and business cycles. As a result, dividend growth rates may vary significantly from year to year. A company may increase dividends rapidly during profitable periods and reduce them during economic downturns. Because of this unrealistic assumption, the valuation obtained through DDM may not accurately reflect actual market conditions. Therefore, the model may produce misleading results when dividend growth is unstable or unpredictable.

- Difficulty in Estimating Growth Rate

Accurately estimating the future growth rate of dividends is one of the most challenging aspects of the Dividend Discount Model. Growth depends on several uncertain factors such as profitability, market demand, economic conditions, management policies, and industry performance. Even small errors in estimating the growth rate can significantly affect the calculated value of shares and the cost of equity. Since future conditions cannot be predicted with complete accuracy, the reliability of DDM is often questioned. This limitation reduces the practical usefulness of the model in dynamic and rapidly changing business environments.

- Highly Sensitive to Input Variables

The Dividend Discount Model is extremely sensitive to changes in its key inputs, particularly the growth rate and required rate of return. A slight variation in either variable can lead to a substantial change in the estimated share value. This sensitivity may result in inconsistent valuations and unreliable investment decisions. For example, increasing the growth rate by just one percentage point can significantly increase the calculated value of a stock. Such dependence on assumptions makes the model vulnerable to estimation errors and reduces confidence in the accuracy of its results.

- Ignores Non-Dividend Factors

The Dividend Discount Model focuses solely on dividend payments and ignores several other important factors that influence a company’s value. Market conditions, asset values, earnings potential, technological innovations, competitive advantages, and management quality can all affect stock prices. Investors often consider these factors when making investment decisions. Since DDM does not incorporate such elements, it may fail to capture the complete picture of a company’s financial strength and growth prospects. Consequently, the model may underestimate or overestimate the actual value of shares in many situations.

- Not Suitable for High-Growth Companies

High-growth companies often reinvest their profits into expansion, research, development, and innovation rather than paying dividends. Because the Dividend Discount Model relies on expected dividend payments, it cannot accurately value such companies. Even if dividends are paid, rapid changes in growth rates make it difficult to apply the model effectively. Many successful companies experience different growth phases throughout their life cycles, which contradicts the model’s assumptions. Therefore, DDM is generally unsuitable for valuing growth-oriented firms and may provide unrealistic estimates of their market value.

- Assumes Infinite Life of the Company

The Dividend Discount Model assumes that a company will continue operating indefinitely and paying dividends forever. Although this assumption simplifies calculations, it may not always be realistic. Businesses can face financial difficulties, industry disruptions, mergers, acquisitions, or liquidation. Such events can affect future dividend payments and company survival. Since no business can be guaranteed to exist forever, the assumption of perpetual life may lead to inaccurate valuations. This limitation reduces the model’s practicality, particularly when evaluating companies operating in highly competitive or uncertain industries.

- Limited Use in Changing Market Conditions

Financial markets are influenced by economic cycles, inflation, interest rates, government policies, and investor sentiment. These factors can cause significant fluctuations in stock prices and investor expectations. However, the Dividend Discount Model assumes stable conditions and does not fully account for sudden market changes. As a result, the model may fail to reflect current market realities during periods of economic uncertainty or volatility. Investors relying solely on DDM may overlook important market signals and make inaccurate decisions. Therefore, the model should be used along with other valuation techniques for better results.

by

by