Technological Impact in Banking Operation

by

by Banking industry is a backbone of Indian financial system and it is afflicted by many challenging forces. One such force is revolution of information technology. In today’s era, technology support is very important for the successful functioning of the banking sector. Without IT and communication we cannot think about the success of banking industry, it has enlarged the role of banking sector in Indian economy. For creating an efficient banking system, which can respond adequately to the needs of growing economy, technology has a key role to play. In past 10 years, banks in India have invested heavily in the technology such as Tele banking, mobile banking, net banking, ATMs, credit cards, debit cards, electronic payment systems and data warehousing and data mining solutions, to bring improvements in quality of customer services and the fast processing of banking operation. Heavy investments in IT have been made by the banks in the expectation of improvement in their performance. But important in the performance depends upon, differences in the deployment, use and effectiveness of IT.

Information technology in banking sector refers to the use of sophisticated information and communication technologies together with computer science to enable banks to offer better services to its customers in a secure, reliable and affordable manner and sustain competitive advantage over other banks. The significance of technology is greatly felt in the financial sector in view of the competitive advantage for banks resulting in the efficient customer service.

In the development of Indian Economy, Banking sector plays a very important and crucial role. With the use of technology there had been an increase in penetration, productivity and efficiency. It has not only increased the cost effectiveness but also has helped in making small value transactions viable. Electronic delivery channels, ATMs, variety of cards, web based banking, and mobile banking are the names of few outcomes of the process of automation and computerization in Indian banking sector.

Transformation of Indian Banking

Indian banking has undergone a total transformation over the last decade. Moving seamlessly from a manual, scale-constrained environment to a technological leading position, it has been a miracle. Such a transformation takes place in such a short span of time with such a low cost.

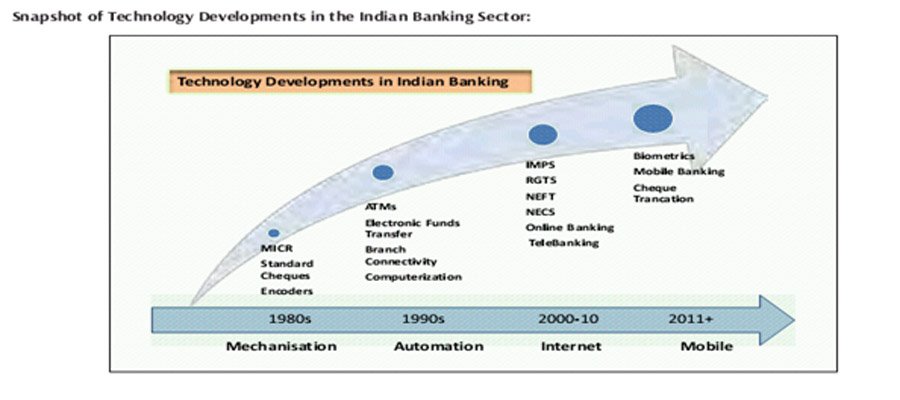

Entry of technology in Indian banking industry can be traced back during the 1990s, the banking sector witnessed various liberalization measure. One of the major objectives of Indian banking sector reforms was to encourage operational self-sufficiency, flexibility and competition in the system and to increase the banking standards in India to the international best practises. With the ease of licensing norms, new private and foreign banks emerged-equipped with latest technology. Deregulation has opened up new opportunities to banks to increase revenues by diversifying into investment banking, insurance, credit cards, mortgage financing, depository services etc. The role of banking is redefined from a mere intermediary to service provider of various financial services under one roof acting like a financial supermarket.

Important events in evolution of Information Technology:-

- Introduction of MICR based cheque processing

- Arrival of card based payments

- Introduction of Electronic Clearing Services

- Introduction of RTGS/NEFT

- Introduction of Cheque Truncation System (CTS) or Image-based Clearing System (ICS)

- Introduction of Core Banking Solutions (CBS)

- Introduction of Automated Teller Machine (ATMs)

- Introduction of Phone and Tele Banking

- Introduction of Internet and Mobile Banking

Recent IT Trends of Indian banks

The banking industry is going through a period of rapid change to meet competition, challenges of technology and the demand of end user. Clearly technology is a key differentiator in the performance of banks. Banks need to look at innovation not just for product but for process also.

Today, technology is not only changing the environment but also the relationship with customers. Technology has not broken barriers but has also brought about superior products and channels. This has brought customer relationship into greater focus. It is also viewed as an instrument of cost reduction and effective communication with people and institutions associated with the banking business. The RBI has assigned priority to the up gradation of technological infrastructure in financial system. Technology has opened new products and services, new market and efficient delivery channels for banking industry. IT also provides the framework for banking industry to meet challenges in the present competitive environment. IT enables to cut the cost of global fund transfer.

Some of the recent IT devices described as below:

-

Electronic Payment and Settlement System

The most common media of receipts and payment through banks are negotiable instruments like cheques. These instruments could be used in place of cash. The inter bank cheques could be realized through clearing house systems. Initially there was a manual system of clearing but the growing volume of banking transaction emerged into the necessity of automating the clearing process.

-

Use of MICR Technology

MICR overcomes the limitation of clearing the cheques within banking hours and thus enables the customer to get the credit quickly. These are machine – readable codes added at the bottom of every cheque leaf which helped in bank and branch-wise sorting of cheques for smooth delivery to the respective banks on whom they are drawn. This no doubt helped in speeding up the clearing process, but physical delivery of cheques continued even under this partial automation.

-

CTS (Cheque Truncation System)

Truncation means stopping the flow of the physical cheques issued by a drawer to the drawee branch. The physical instrument is truncated at some point on route to the drawee branch and an electronic image of the cheque is sent to the drawee branch along with the relevant information like the MICR fields, date of presentation, presenting banks etc. This would eliminate the need to move the physical instruments across branches, except in exceptional circumstances, resulting in an effective reduction in the time required for payment of cheques, the associated cost of transit and delays in processing etc., thus speeding up the process of collection or realization of cheques.

-

Electronic Clearing Services (ECS)

The ECS was the first version of “Electronic Payments” in India. It is a mode of electronic funds transfer from one bank account to another bank account using the mechanism of clearing house. It is very useful in case of bulk transfers from one account to many accounts or vice-versa. The beneficiary has to maintain an account with the one of the bank at ECS Centre.

There are two types of ECS (Electronic Clearing Service)

- ECS Credit: ECS Credit clearing operates on the principle of ‘single debit multiple credits’ and is used for transactions like payment of salary, dividend, pension, interest etc.

- ECS Debit: ECS Debit clearing service operates on the principle of ‘single credit multiple debits’ and is used by utility service providers for collection of electricity bills, telephone bills and other charges and also by banks for collections of principle and interest repayments.

-

Electronic Fund Transfer (EFT)

EFT was a nationwide retail electronic funds transfer mechanism between the networked branches of banks. NEFT provided for integration with the Structured Financial Messaging Solution (SFMS) of the Indian Financial Network (INFINET). The NEFT uses SFMS for EFT message creation and transmission from the branch to the bank’s gateway and to the NEFT Centre, thereby considerably enhancing the security in the transfer of funds.

-

Real Time Gross Settlement (RTGS)

RTGS system is a funds transfer mechanism where transfer of money takes place from one bank to another on a ‘real time’ and on ‘gross basis’. This is the fastest possible money transfer system through the banking channel. Settlement in ‘real time’ means payment transaction is not subjected to any waiting period. The transactions are settled as soon as they are processed. “Gross settlement” means the transaction is settled on one to one basis without bunching with any other transaction.

-

Core Banking Solutions (CBS)

Computerization of bank branches had started with installation of simple computers to automate the functioning of branches, especially at high traffic branches. Core Banking Solutions is the networking of the branches of a bank, so as to enable the customers to operate their accounts from any bank branch, regardless of which branch he opened the account with. The networking of branches under CBS enables centralized data management and aids in the implementation of internet and mobile banking. Besides, CBS helps in bringing the complete operations of banks under a single technological platform.

-

Development of Distribution Channels

The major and upcoming channels of distribution in the banking industry, besides branches are ATMs, internet banking, mobile and telephone banking and card based delivery systems.

-

Automated Teller Machine (ATM)

ATMs are perhaps most revolutionary aspect of virtual banking. The facility to use ATM is provided through plastic cards with magnetic strip containing information about the customer as well as the bank. In today’s world ATM are the most useful tool to ensure the concept of “Any Time Banking” and “Any Where Banking”.

-

Phone Banking

Customers can now dial up the banks designed telephone number and he by dialling his ID number will be able to get connectivity to bank’s designated computer. By using Automatic voice recorder (AVR) for simple queries and transactions and manned phone terminals for complicated queries and transactions, the customer can actually do entire non-cash relating banking on telephone: Anywhere, Anytime.

-

Tele Banking

It is another innovation, which provided the facility of 24 hour banking to the customer. Tele-banking is based on the voice processing facility available on bank computers. The caller usually a customer calls the bank anytime and can enquire balance in his account or other transaction history.

-

Internet Banking

Internet banking enables a customer to do banking transactions through the bank’s website on the internet. It is system of accessing accounts and general information on bank products and services through a computer while sitting in its office or home. This is also called virtual banking.

-

Mobile Banking

Mobile banking facility is an extension of internet banking. Mobile banking is a service provided by a bank or other financial institution that allows its customers to conduct financial transactions remotely using a mobile device. Unlike the related internet banking it uses software, usually called an App, provided by the financial institution for the purpose. Mobile banking is usually available on a 24 hour basis. Some financial institutions have restrictions on which accounts may be accessed through mobile banking, as well as a limit on the amount that can be transacted. Transactions through mobile banking may include obtaining account balances and lists of latest transactions, electronic bill payments, and fund transfers between a customer’s or another’s accounts.

Conclusion

Information Technology offers enormous potential and various opportunities to the Indian Banking sector. It provides cost-effective, rapid and systematic provision of services to the customer. The efficient use of technology has facilitated accurate and timely management of the increased transaction volumes of banks which comes with larger customer base. Indian banking industry is greatly benefiting from IT revolution all over the world.

Another concept i.e Virtual Banking or Direct Banking is now gaining importance all over the world. According to this concept Banks offer products, services and financial transaction only through electronic delivery channels generally without any physical branch. Owing to lower branch maintenance and manpower cost such banks are able to offer competitive pricing for their product and services as compared to traditional banks.

The Indian banks lag far behind the international banks in providing online banking. In fact, this is not possible without creating sufficient infrastructure or presence of sufficient number of users. Technology is going to hold the keys to future of banking. So banks should try to find out the trigger of change. Indian Banks need to focus on swift and continued infusion of technology.