Preliminaries in establishing system of Standard Costing

by

by Following preliminaries should be gone through before a standard costing system is established:

- Establishment of cost centres

- Types of standard

- Setting the standards

Establishment of Cost Centres:

As defined earlier in this book, a cost centre is a location, person or item of equipment for which costs may be ascertained and used for the purpose of cost control. Establishment of cost centres is necessary for fixing responsibilities for unfavourable variances.

Types of Standard:

There are three types of standards:

(a) Current Standard:

A standard which is related to current conditions and is established for use over a short period of time. This standard may be fixed on the basis of ideal standard or expected standard.

Ideal Standard:

This is the standard which can be attained under the most favourable conditions possibly. In other words, this standard is based upon a very high degree of efficiency which is rather impossible to achieve.

In this standard, it is assumed that there will be the most desirable conditions of performance and that there will be no wastage of materials or time and no inefficiencies in the manufacturing processes. This standard is not likely to be achieved because ideal conditions of performance will not prevail. It is, therefore, a theoretical standard.

The utility of this standard is that it sets a target which, though not attainable in practice, is always aimed at. The criticism of the standard is that when actual costs are compared with such standard costs, large unfavourable variances are shown and these variances become a permanent feature of the concern.

The ideal standard will breed frustration among employees because such standard is never to be attained. Nobody will pay serious attention to such standard and setting up of this standard will become a farce.

Expected or Attainable Standard, This is the standard which is anticipated during a future specified budget period. In fixing this type of standard present conditions and circumstances prevailing within a particular industry are taken into consideration. Besides, due weight-age is given to the expected changes in the present circumstances and conditions.

In setting up this standard, a reasonable allowance is also made for unavoidable (normal) wastages. This standard is, therefore, considered to be more realistic than the ideal standard because this standard is based on realities rather than on the most ideal conditions. Hence, this type of standard is best suited from control point of view because this standard reveals real variances from the attainable performance.

(b) Basic Standard:

It is a standard which is established for use unaltered over a long period of time. This standard is fixed for long periods so as to help forward planning. Basic standard is established for some base year and is not changed for a long period of time as material prices, labour rates and other expenses change.

Deviations of actual costs from basic standards will not serve any practical purpose because basic standards remain unaltered over a long period of time and are not adjusted to current market conditions. Thus, this type of standard is not suitable from cost control point of view. However, variances calculated on the basis of basic standards will help in studying the trends in manufacturing costs over a long period of time.

Comparison of Current Standard and Basic Standard:

Current standards relate to current conditions and operate only for a short period before they are revised when conditions change. On the other hand, basic standards are set for a long period and there is no need for constant revision for such standards. Deviation of actual costs from basic standard costs will not serve any practical purpose because standards are not adjusted to current market conditions.

However, such standards will be helpful in studying the trends of variances over a long period of time which is not possible in case of current standards which go on changing. Current standards will take care of inflationary tendencies because they are adjusted to current market conditions. On the other hand, basic standards are static and do not take care of inflationary tendencies.

(c) Normal Standard:

This standard is defined as “the average standard which it is anticipated can be attained over a future period of time, preferably long enough to cover one trade cycle”. Such standards are established on the basis of average estimated performance over a future period of time (say 5 years) covering one trade cycle.

It is difficult to follow normal standards in practice as it is not possible to forecast performances with a reasonable degree of accuracy for a long period of time. Such standards are attainable under anticipated normal conditions and are not attainable if anticipated conditions do not prevail over a future period of time. That is why normal standards may not be a useful device for the purpose of cost control.

Setting the Standards or Establishment of Standard Cost:

Just like a Budget Committee, there should be a Standard Committee which should be entrusted with the work of setting standard costs. This Committee will include General Manager, Purchase Officer, Production Engineer, Production Manager, Sales Manager, Cost Accountant, and other functional heads, if any.

Of all the persons, the cost accountant plays a very important role in setting the standards because he is to supply the necessary costs figures and coordinate the activities of the committee so that standards set are as accurate as possible.

It may be noted that standards set should neither be too high nor too low. Nobody will take interest in the standards if these are too high because such standards are not capable of being achieved and employees will always have an opportunity to excuse the failure to reach such standards.

Such standards are not realistic and, therefore, cannot be used in inventory valuation, product costing and pricing, planning and control, and capital investment decisions.

Low standards, on the other hand, will not induce employees and management to put more efforts because they can be achieved very easily. They defeat the objectives of standard costing and fail to disclose inefficiencies because they can be attained by poor performance.

As a general rule, currently attainable standards should be set which can be attained if employees and management become more efficient or put some more efforts. Such standards motivate employees and are most appropriate for performance appraisal, cost control and decision making.

According to the National Association of Accountants (U.S.A.), “Such standards provide definite goals which employees can usually be expected to reach and also appear to be fair bases from which to measure deviations for which the employees are held responsible. A standard set at a level which is high yet still attainable with reasonable diligent effort and attentive to the correct methods of doing the job may also be effective for stimulating efficiency.”

The success of standard costing depends upon the establishment of correct standards. Thus, every possible care should be taken in the establishment of standards and standards should be established for each element of cost as follows:

(a) Direct Material Cost:

Standard material cost for each product should be predetermined. This will include:

(i) Determination of standard quantity of materials needed for the production.

(ii) Determination of standard price per unit of material.

In ascertaining standard quantity of materials, the standard specification of materials should be planned by the engineering department after consulting the past records. While setting standards an allowance should be made for the normal wastage of materials.

The purpose of determining standard quantities of materials should be to achieve maximum economies in material usage.

A detailed listing of all materials required for a product is made on a Standard Material specification, the specimen of which may be as follows:

| Standard Material Specification | |||

| No…… | Date…… | ||

| Description of the Product………. | |||

| Code No. | Description of The Product | Quantity of the Product per Material | Remarks |

| Prepared By… | |||

| Checked By… | |||

The standard prices of materials should be determined for the various types of material needed for the production. This is done by the cost accountant in collaboration with the purchase officer. Standard price for each item of material is established after carefully studying the market conditions and forecasting the trend of prices for a future period.

While setting standard material price, the cost of purchasing and storekeeping should also be included in the price of materials. The object of fixing standard prices of materials is to increase efficiency in the purchasing so that prices of materials may be kept down.

Any difference between standard price and actual price is to be referred to the Purchasing Department for explanation, so before setting standards for material prices, it is advisable to see that purchasing functions are efficiently managed. Setting up of standard prices of materials required is a difficult task because it depends on so many factors beyond anybody’s control. Generally standard prices are based on current prices adjusted to expected changes in future.

(b) Direct Labour Cost:

Determination of standard direct labour cost will include determination of:

(i) Standard time.

(ii) Standard rate.

It becomes necessary to standardise the time to be taken for each category of labour and for each operation involved. Time and motion study will determine how much time is to be allowed for each operation involved. While fixing the standard time, due allowance should be made for fatigue, tool setting, receiving instructions and normal idle time. Standard time can also be determined on the basis of the average of the past performance. Though this method is simple, it is not scientific.

Thus, standard time is established on the basis of time and motion study and this is done in conjunction with the work study engineers. Standard times established according to time and motion study are independent of previous performances. It is good for the development of objective standards. Standard time can also be set by taking trial runs for new products. This method is not satisfactory as real conditions are not available in such runs.

The fixation of standard labour rates is not as difficult as the fixation of standard prices of materials is because labour rates are usually pre-established.

Standard rates of pay should be established for every category of labour. Labour rates in the past may not be reliable basis for determination of rates if the labour rates are subject to fluctuating demand and supply of the labour force. Any expected increase in rates should be considered in the determination of standard rates.

Establishment of standard rates of pay do not present ay problem in those industries where wage rates have been fixed by contracts, Law, Wages Tribunals and Wages Boards. Fixation of standard rates will depend upon the method of wage payment.

Standard rates per hour or per day will be fixed if wages are paid according to time wages system and when the method of wage payment is piece rate, standard wages per piece will be fixed. Personnel department will help the cost accountant in determining standard rates of pay.

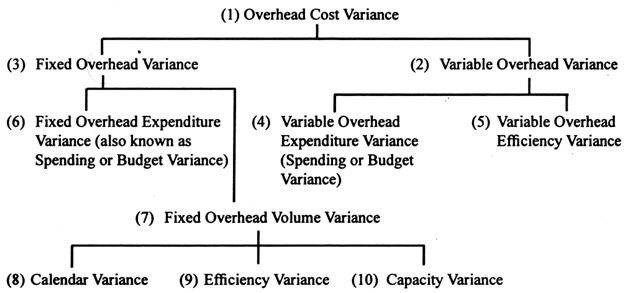

Overheads:

Broadly speaking overheads are segregated into fixed and variable and standard overhead rate should be determined for fixed as well as variable overhead. Standard fixed overhead rate and standard variable overhead rate should also be determined according to the function-wise classification of overheads manufacturing, administrative and selling and distribution so that exact place of overhead variance may be located and corrective action may be taken.

Standard overhead rate is determined keeping in view past experience, present conditions and future trends. Fixation of standard overhead rate involves determination of standard overhead costs, estimation of standard level of production reduced to a common base such as units of production, direct labour hours, machine hours, etc. and finally determination of standard overhead rate by dividing standard overhead costs by standard level of production.

The formula for the calculation of standard rate is:

Standard variable overhead rate:

Standard Hours:

Production is generally expressed in physical units such as kilos, tons, gallons, units, dozens etc. But it is difficult to express all the products in one common unit when different types of products which are measured in different units are manufactured in a factory. In such a case, it is essential to have a common unit in which all the products can be measured.

Time factor is common to all the products, and, therefore, production can be expressed in standard hours. A standard hour can be defined as an hour which measures the amount of work that should be performed in one hour under standard conditions.

cessing systems, management information systems, executive information systems and enterprise resource planning systems.

cessing systems, management information systems, executive information systems and enterprise resource planning systems.