Preparation of Final accounts of General insurance

by

by The financial statements of general insurance companies must be in conformity with the regulations of IRDA, Schedule B.

It has three parts: viz:

(a) Revenue Account;

(b) Profit and Loss Account, and

(c) Balance Sheet.

Revenue Account (Form B-RA):

The Revenue Account of general insurance companies must be prepared in conformity with the regulations of IRDA, Regulations 2002, as per the requirements of Schedule B. It has already been stated above that separate Revenue Account is to be prepared for each individual unit i.e. for Marine, Fire, and Accident.

These individual revenue accounts will highlight the result of operation of each individual unit for a particular accounting period. It also reveals the incomes and expenditures of each individual unit. Like Revenue Account of a life insurance company, Revenue Account is prepared under Mercantile System of Accounting.

Items appearing in Revenue Account:

Premiums:

It has already been stated above that general insurance policies are issued for a short period, say, for a year. As a result, many of them may be unexpired at the end of the year. Therefore, the entire premium so received cannot be treated as an income for the current year only. A portion of that amount should be carried forward to the next year in order to cover the unexpired risks. This is what is known as Reserve for Unexpired Risks.

As per Schedule IIB of the IRDA the Reserve for Unexpired Risks should be provided for out of net premium so received as:

(a) 50% for Fire Insurance business;

(b) 50% for Miscellaneous Insurance business;

(c) 50% for Marine Insurance business other than Marine Hull business, and

(d) 100% for Marine Hull business.

In addition to the above, if any company wants to maintain more than this level, it can do so. The same is known as Additional Reserve.

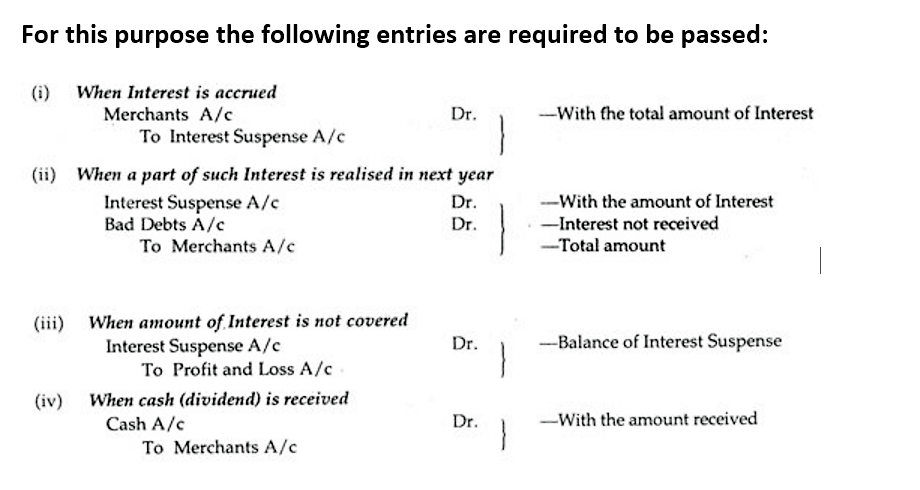

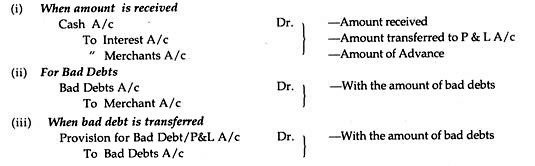

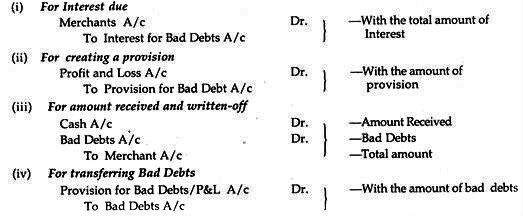

Claims Incurred (Net):

It is the first item that appears in the expenditure side of the Revenue Account of an insurance company. Claims mean the amount which is payable by the insurer, to the insured for the loss suffered by the latter against which the insurance was made.

Claims can be divided into:

(a) Claims intimated but not yet accepted and paid;

(b) Claims intimated, accepted but not paid;

(c) Claims intimated, accepted and paid; and

(d) Claims rejected. But if there is only ‘Claims intimated’ the same is to be treated like (b). That is why, in order to find out the outstanding claims, claims that have been intimated (whether paid or unpaid) should be considered.

At the end of the year the entry for the purpose will be:

Claims A/c Dr.

To Claims Intimated Accepted but Not Paid A/c

Claims Intimated but Not Accepted and Not Paid A/c

A reverse entry should be passed at the beginning of the next year for which there will be no effect in Claims Account. But, if any claim is rejected subsequently, the amount is to be transferred to Profit and Loss Account and Claims Account must be credited for the purpose.

Commissions:

Insurance Regulatory and Development Authority Act, 1999, regulates the amount of commission which is payable on policies to the agents.

Operating Expenses:

Operating expenses will come under Schedule 4 of the Act. All revenue expenses other than the commission and claims will appear under this head.

Some of the operating expenses are:

Training Expenses; Rent, Rates and Taxes; Repairs; Printing and Stationery; Legal and Professional Expenses; Advertisement and Publicity, Interest on Bank Charges, etc.

Profit and Loss Account (Form B-Pl):

In order to find out the overall performance or results of the operating of general insurance business Profit and Loss Account of the General Insurance Companies is prepared. It also takes into account the income from investment by way of interest, dividend, Rent Profit/Loss on sale of investments. Provision for Taxations and Provision for Doubtful Debts, if any, should also be provided for.

Similarly, other expenses related to insurance business and bad debts written-off also will be adjusted to this account. However, appropriation section of Profit and Loss Account will contain payment of interim dividend; proposed dividend; transfer to any reserve i.e. appropriation items.

Balance Sheet (Form B-Bs):

The Balance Sheet of a general insurance company as per IRDA format is divided into two parts, viz. Source of Funds and Application of Funds. It is prepared in vertical form.

Sources of Funds:

It consists of:

(i) Share Capital (Schedule 5):

Various classes of Share Capital viz. Authorized Capital, Issued, Subscribed, Called-up and Paid up capital are separately shown.

(ii) Reserves & Surplus- (Schedule 6):

All kinds of reserves will appear under this head, viz. Securities Premium, Balance of Profit and Loss Account, General Reserve, Capital Redemption Reserve, Capital Reserve, etc.

(iii) Borrowings (Schedule 7):

Long term borrowings viz. Bonds, Debentures, Bank Loans, taken from various financial institutes will appear under this head.

Applications of Funds:

It consists of:

(i) Investments — (Schedule 8):

All kinds of investments, whether long-term or short-term, will appear under this schedule.

(ii) Loans— (Schedule 9):

Different kinds of loans clearly specified, viz. (a) Security-wise, Borrower-wise, performance-wise, and maturity-wise classification.

(iii) Fixed Assets (Schedule 10):

All fixed assets viz. Goodwill, Intangibles, Land and Building, Freehold/Leasehold Property, Furniture & Fixture, etc. will appear in this schedule.

(iv) Current Assets:

This section has two parts:

(a) Cash and Bank Balances (Schedule 11):

All cash and bank balances lying at Deposit Account and Current Account, Money-at-call and short notice etc. will appear in the Schedule.

(b) Advances and Other Assets (Schedule 12):

All advances (short-term) and other assets, if any, will appear in this Schedule.

(v) Current Liabilities (Schedule 14):

All current liabilities viz., Agents’ balances, Premium Received in Advance, Sundry Creditors, Claims Outstanding etc.

(vi) Provisions— (Schedule 15):

All kinds of provisions viz., Reserve for Unexpired Risk; Provision for Taxation, Proposed Dividend, Others.

New Format for Financial Statement:

According to Insurance Regulatory and Development Authority (Preparation of Financial Statements and Auditors’ Report of Insurance Companies) Regulations, 2002, every general insurance company must prepare as per Schedule B of the Regulations the following three statements for preparation and presentation of financial statements:

For General Insurance:

Revenue Account— Form B-RA

Profit and Loss Account — Form B-PL

Balance Sheet — Form B-BS

Thus, in short, every general insurance company is required to prepare a Revenue Account (Form B-RA); Profit and Loss Account (Form B-PL) and Balance Sheet (Form B-BS).