Financial Planning is the process of estimating the capital required for a business and determining its sources. It involves forecasting future financial needs, preparing policies related to procurement, investment, and administration of funds. It ensures that adequate funds are available at the right time and used efficiently for achieving business objectives. Financial planning aims to balance financial resources with the company’s long-term and short-term requirements.

Financial Planning is the process of setting financial goals, developing strategies, and managing resources to achieve business objectives efficiently. It involves budgeting, forecasting, investment planning, risk assessment, and fund allocation. Proper financial planning ensures liquidity, profitability, and business growth while minimizing financial risks. It helps organizations optimize capital usage, control costs, and make informed financial decisions. In India, businesses follow structured financial planning to comply with regulatory requirements and maximize shareholder value. By aligning financial strategies with market conditions and organizational goals, financial planning ensures long-term stability, operational efficiency, and sustainable business success in a competitive environment.

Objectives of Financial Planning

One of the primary objectives of financial planning is to ensure that sufficient funds are available for business operations and expansion. Organizations need funds for working capital, investments, and growth opportunities. A well-structured financial plan identifies funding requirements in advance, helping businesses secure capital through equity, debt, or retained earnings. Proper financial planning ensures a steady cash flow, prevents liquidity crises, and maintains business stability. By forecasting financial needs accurately, companies can avoid financial shortages and ensure smooth operational continuity.

Financial planning aims to allocate resources efficiently to maximize profitability and reduce wastage. Organizations must ensure that funds are invested in high-yield projects and used productively. This includes managing capital expenditure, operational costs, and investments to achieve financial efficiency. Effective financial planning prevents underutilization or overutilization of resources, ensuring that funds are used where they generate the best returns. By optimizing financial resources, businesses can enhance their financial stability, improve productivity, and achieve long-term growth while minimizing unnecessary expenditures.

A key objective of financial planning is to ensure adequate liquidity for smooth business operations. Liquidity management involves maintaining a balance between current assets and liabilities to meet short-term financial obligations. Without proper financial planning, businesses may face cash flow shortages, leading to operational disruptions or financial distress. By forecasting cash inflows and outflows, financial planning helps organizations maintain a healthy liquidity position. This ensures timely payments to suppliers, employees, and creditors, preventing financial instability and fostering business sustainability.

Financial planning helps mitigate risks related to market fluctuations, economic downturns, and unexpected financial crises. Businesses face uncertainties such as inflation, changing interest rates, or global financial instability. A well-structured financial plan includes risk assessment and contingency measures to safeguard against potential financial losses. Techniques like diversification, insurance, and hedging are incorporated into financial planning to manage risks effectively. By reducing financial uncertainties, companies can protect their assets, ensure operational continuity, and maintain investor confidence in their financial stability.

One of the fundamental objectives of financial planning is to boost profitability and drive business growth. Proper planning ensures that funds are invested in high-return projects and cost-effective operations. Businesses set financial goals to increase revenue, minimize costs, and enhance profit margins. Through financial forecasting and budgeting, companies can identify opportunities for expansion and innovation. By aligning financial strategies with business objectives, financial planning supports long-term profitability and competitive advantage in a dynamic business environment.

Financial planning determines the right mix of debt and equity to finance business operations. A well-balanced capital structure reduces the cost of capital while maintaining financial stability. Organizations need to decide the proportion of funds to be raised through equity, loans, or retained earnings. Financial planning helps businesses evaluate borrowing options, interest rates, and repayment capabilities to maintain financial health. Proper capital structure management ensures that companies can meet their financial obligations without excessive debt burdens or dilution of ownership.

Financial planning supports long-term business growth by allocating resources for expansion strategies such as entering new markets, launching new products, or upgrading technology. A company’s sustainability depends on continuous financial planning that aligns investment decisions with future business goals. By setting financial targets and securing necessary funding, organizations can sustain their growth momentum. Proper financial planning also helps businesses adapt to economic changes, technological advancements, and market trends, ensuring their long-term viability and success in a competitive landscape.

Investors and stakeholders seek financial transparency and strategic financial management before investing in a business. A well-structured financial plan demonstrates a company’s financial stability, growth potential, and ability to generate returns. By ensuring timely financial reporting, risk management, and profitability, financial planning enhances investor trust. It also strengthens the company’s market reputation, making it easier to attract new investments and business opportunities. A financially sound organization can maintain strong stakeholder relationships and sustain its credibility in the competitive market environment.

Need of Financial Planning

Financial planning helps a business determine the amount of funds required for starting and running operations. It estimates expenses such as purchase of assets, payment of wages and operating costs. By forecasting financial needs in advance, the firm avoids shortage of funds that may interrupt production and business activities. Adequate availability of funds enables smooth functioning of operations and helps management concentrate on productivity, growth and achievement of organizational objectives without financial stress.

Financial planning not only prevents shortage of funds but also avoids excess funds. Idle funds do not generate income and increase the cost of capital for the organization. Through proper estimation and budgeting, the finance manager raises only the necessary amount of capital. Efficient use of funds improves profitability and financial efficiency. Therefore, financial planning helps in maintaining an optimum level of funds and ensures that resources are neither wasted nor misused in the business.

- Helps in Proper Investment

Financial planning assists management in selecting suitable investment opportunities. It provides information about available funds and future financial commitments, enabling managers to invest wisely in profitable projects. The firm can evaluate various investment alternatives and choose those giving maximum returns with minimum risk. Proper investment decisions increase productivity and earning capacity of the business. Thus, financial planning ensures that funds are allocated to the most productive uses, supporting long-term growth and financial stability.

- Facilitates Business Expansion

A business aims to grow and expand over time. Financial planning helps in estimating future capital requirements for expansion such as opening new branches, introducing new products, or increasing production capacity. By forecasting future financial needs, the firm can arrange funds in advance through appropriate sources. This prevents delays in expansion activities. Hence, financial planning supports continuous development and enables the organization to take advantage of profitable opportunities in the market at the right time.

- Maintains Proper Cash Flow

Financial planning helps in controlling cash inflows and outflows within the business. It ensures that sufficient cash is available to meet day-to-day expenses like wages, salaries, and operating costs. Proper planning prevents liquidity problems and avoids situations where the firm cannot pay its obligations on time. By maintaining a balanced cash flow, the company strengthens its financial position and improves its goodwill and creditworthiness in the market.

Uncertainty is a common feature of business. Financial planning helps in predicting possible financial problems and taking precautionary measures. By analyzing future conditions, the firm can prepare for economic changes, price fluctuations and unexpected expenses. It provides a safety margin and reduces dependence on emergency borrowings. As a result, financial planning minimizes financial risk and protects the organization from losses, thereby ensuring stability and continuity of business operations.

- Helps in Coordination and Control

Financial planning promotes coordination among different departments such as production, marketing and human resources. Every department requires funds to perform its activities, and planning allocates funds according to priorities. It also establishes financial targets and standards for performance evaluation. By comparing actual performance with planned performance, management can take corrective actions. Therefore, financial planning acts as a tool of financial control and improves managerial efficiency within the organization.

Financial planning contributes to higher profitability by ensuring efficient utilization of resources. Proper allocation of funds, cost control and avoidance of wastage reduce unnecessary expenses. It helps the firm invest in profitable projects and maintain an optimum capital structure. As a result, the organization earns higher returns and improves shareholders’ wealth. Thus, financial planning plays a vital role in achieving the ultimate objective of the business, which is maximizing profitability and financial success.

Steps in Financial Planning

Step 1. Assessing Financial Needs

The first step in financial planning is to identify the financial needs of the business. This involves understanding the purpose for which funds are required—such as starting operations, expanding capacity, purchasing assets, or meeting working capital requirements. A thorough needs assessment considers both short-term and long-term financial demands. It also takes into account internal and external factors influencing fund requirements. Proper identification of needs ensures that planning begins with clarity, avoiding both shortages and excesses of funds.

Step 2. Setting Financial Objectives

Once financial needs are assessed, the next step is to set clear, realistic financial objectives. These objectives may include maximizing profits, ensuring liquidity, reducing costs, improving return on investment, or maintaining solvency. Financial objectives must align with the overall goals of the business. Setting clearly defined goals helps management plan effectively and measure progress over time. These objectives act as guiding principles that direct financial decisions and strategies, ensuring the organization maintains a stable and progressive financial posture.

Step 3. Estimating the Volume of Funds Required

This step involves calculating how much money the business will need to achieve its objectives. The estimation includes both fixed capital requirements—such as land, buildings, and machinery—and working capital needs for day-to-day operations. Factors like production levels, credit policies, and operating cycles influence the amount of required funds. A realistic estimate prevents situations of underfunding, which hampers operations, or overfunding, which increases financial costs. Accurate estimation forms the foundation for all future financial decisions.

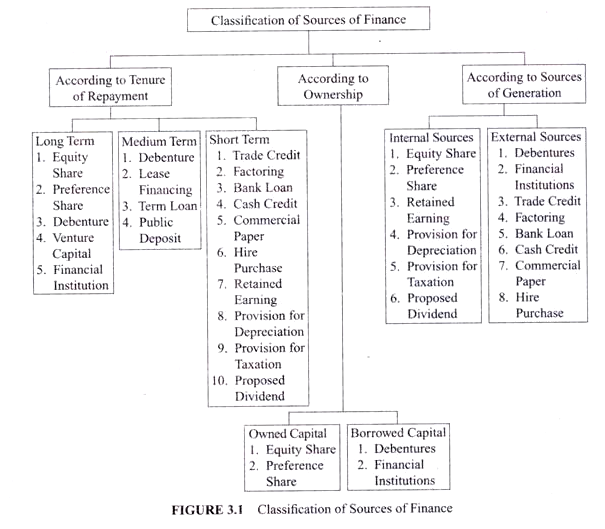

Step 4. Determining Sources of Finance

After estimating the fund requirement, the organization must identify suitable sources of finance. These may include equity, preference capital, debentures, bank loans, retained earnings, public deposits, or trade credit. Choosing appropriate sources depends on the cost of funds, risk, control considerations, and repayment capacity. A balanced mix of short-term and long-term sources is necessary to maintain financial stability. Careful selection helps minimize financial costs, maintain flexibility, and ensure the business can fund its plans without undue stress.

Step 5. Developing Financial Policies

This step involves drafting policies regarding procurement, investment, and management of funds. Policies may include guidelines on capital structure, debt-equity ratio, dividend distribution, credit terms, and cash management. Financial policies ensure consistency, transparency, and discipline in financial decisions. They help avoid impulsive decisions and provide a framework within which managers operate. Effective financial policies support long-term financial health and ensure that the company maintains a well-organized approach to planning and managing finances.

Step 6. Preparing Financial Plans

A financial plan outlines how the business will acquire and use funds over a certain period. It includes projected financial statements, such as cash flow statements, income statements, and balance sheets. The plan specifies when funds will be needed and how they will be allocated to various activities. A well-prepared financial plan ensures coordination among departments and aligns financial resources with business strategies. It also helps predict potential financial challenges and prepares the firm for future uncertainties.

Step 7. Implementing the Financial Plan

Implementation involves putting the financial plan into action. This includes acquiring funds from selected sources and allocating them to various business activities. Effective implementation requires coordination, timely decision-making, and continuous supervision. Management must ensure that funds are used efficiently and according to the plan. Implementation also involves communicating financial roles and responsibilities across departments. Successful execution converts financial strategies into practical results and supports the overall growth of the business.

Step 8. Reviewing and Monitoring the Plan

The final step is continuous review and monitoring of the financial plan to track performance and identify deviations. This includes comparing actual financial performance with planned targets and analyzing reasons for differences. Monitoring helps identify financial weaknesses, inefficiencies, or changing market conditions that require adjustments. Regular review ensures that the business stays on track and adapts strategies when needed. This step makes financial planning a dynamic and ongoing process that supports long-term sustainability.

Importance of Financial Planning

Financial planning helps businesses maintain financial stability by ensuring a steady cash flow and proper fund allocation. It prevents liquidity crises and enables companies to meet their short-term and long-term financial obligations. By forecasting revenues and expenses, organizations can prepare for financial uncertainties and avoid financial distress. A stable financial position allows businesses to operate smoothly, manage debts effectively, and withstand economic fluctuations. Proper financial planning builds a strong foundation for sustainable growth and long-term financial success.

Financial planning ensures the efficient allocation of resources by prioritizing investments and expenditures. Businesses need to allocate funds wisely to maximize returns and minimize wastage. Proper financial planning helps organizations decide where to invest, how much to spend, and when to cut costs. By optimizing the use of financial resources, companies can improve productivity and profitability. Effective financial planning also prevents underutilization or overutilization of funds, ensuring that financial resources are directed toward the most strategic areas of business growth.

Every business faces financial risks such as market fluctuations, inflation, interest rate changes, and economic downturns. Financial planning helps organizations identify, assess, and manage these risks effectively. By incorporating risk management strategies like diversification, hedging, and insurance, businesses can safeguard their financial health. A well-prepared financial plan includes contingency measures to handle unexpected financial challenges. This proactive approach minimizes potential losses and ensures business continuity, giving organizations the confidence to make strategic financial decisions.

Financial planning plays a crucial role in business expansion by securing funds for growth opportunities. Whether a company wants to launch new products, enter new markets, or invest in technology, proper financial planning ensures the availability of necessary capital. Businesses need long-term financial strategies to scale operations without financial strain. By analyzing market trends, forecasting future earnings, and planning investments, organizations can expand sustainably. Effective financial planning supports innovation and competitive advantage, enabling businesses to grow successfully.

A key benefit of financial planning is enhancing profitability through effective cost management. By analyzing financial data, businesses can identify areas where expenses can be reduced without compromising efficiency. Budgeting, financial forecasting, and expense monitoring help organizations control unnecessary costs and improve profit margins. Financial planning also ensures that funds are allocated to high-return investments, leading to increased profitability. Through strategic cost control, companies can achieve financial efficiency while maintaining product quality and operational excellence.

Sound financial planning provides businesses with accurate financial data and insights, enabling informed decision-making. Companies need to make critical financial decisions regarding investments, capital structure, pricing, and resource allocation. Financial planning helps businesses evaluate different financial scenarios and choose the best course of action. By analyzing financial statements, market trends, and risk factors, organizations can make data-driven decisions that align with their long-term objectives. This strategic approach minimizes uncertainty and enhances overall business performance.

Businesses must comply with various financial laws, taxation policies, and regulatory requirements. Financial planning helps organizations stay updated with legal obligations and avoid penalties or legal complications. In India, companies must adhere to regulations set by SEBI, RBI, and tax authorities. A well-structured financial plan ensures timely tax payments, accurate financial reporting, and compliance with corporate governance standards. Proper financial planning also enhances transparency and accountability, strengthening investor confidence and market reputation.

Investors and stakeholders seek financial stability, transparency, and growth potential before investing in a business. Financial planning enhances investor confidence by demonstrating a company’s financial health and long-term sustainability. Proper financial management ensures timely financial reporting, risk mitigation, and efficient fund utilization. Businesses with well-defined financial plans attract investors, secure funding, and establish credibility in the market. A strong financial plan reassures stakeholders about the company’s financial future, fostering long-term partnerships and business growth opportunities.

by

by