by

by Break-Even Analysis is a financial and risk analysis technique used to determine the level of sales, production, or revenue at which a project or business neither earns a profit nor incurs a loss. The point at which total revenue equals total cost is known as the Break-Even Point (BEP). In capital budgeting, break-even analysis helps managers assess the minimum level of performance required for a project to recover its costs and become financially viable.

This technique is useful for evaluating project risk because it shows how sensitive profitability is to changes in sales volume, costs, or prices. A project with a lower break-even point is generally considered less risky because it can cover its costs with lower sales. Therefore, break-even analysis is an important tool for investment planning, pricing decisions, cost control, and risk assessment.

Formula of Break-Even Analysis

Break-Even Point (Units)

BEP (Units) = Fixed Costs ÷ Contribution per Unit

Where:

Contribution per Unit = Selling Price per Unit − Variable Cost per Unit

Break – Even Point (Sales Value)

BEP (Sales) = Fixed Costs ÷ P/V Ratio

Where:

P/V Ratio = Contribution ÷ Sales × 100

Example of Break-Even Analysis

Suppose:

- Fixed Costs = ₹2,00,000

- Selling Price per Unit = ₹100

- Variable Cost per Unit = ₹60

Step 1: Calculate Contribution per Unit

Contribution = ₹100 − ₹60

Contribution = ₹40

Step 2: Calculate Break-Even Point

BEP = ₹2,00,000 ÷ ₹40

BEP = 5,000 Units

Interpretation: The company must sell 5,000 units to cover all costs. Sales beyond this point will generate profit.

Features of Break-Even Analysis

- Identifies the No-Profit No-Loss Point

A major feature of break-even analysis is that it identifies the no-profit no-loss point of a business or project. This point is known as the break-even point, where total revenue equals total costs. At this stage, the organization neither earns a profit nor incurs a loss. It helps managers understand the minimum level of sales or production required to recover all fixed and variable costs. By determining this critical point, businesses can establish realistic sales targets and evaluate whether a project is financially feasible before committing resources to long-term investments.

- Measures the Risk Level of a Project

Break-even analysis serves as an effective tool for measuring project risk. A project with a high break-even point requires greater sales to cover costs and is therefore considered riskier. Conversely, a lower break-even point indicates lower risk because fewer sales are needed to avoid losses. This feature helps managers assess the financial vulnerability of investment projects. By understanding how much sales volume is necessary to reach profitability, organizations can evaluate whether projected demand is sufficient and make informed decisions regarding project acceptance or rejection.

- Focuses on Cost-Volume-Profit Relationship

An important feature of break-even analysis is its emphasis on the relationship between costs, sales volume, and profits. It examines how changes in production levels, selling prices, fixed costs, and variable costs affect profitability. This cost-volume-profit relationship helps managers understand the impact of operational decisions on financial performance. By analyzing these relationships, businesses can identify the most profitable production and sales levels. This feature makes break-even analysis a valuable planning and control tool for improving efficiency, maximizing profits, and managing business operations effectively.

- Helps in Profit Planning

Break-even analysis is useful not only for identifying the no-profit no-loss point but also for profit planning. Once the break-even point is known, managers can determine the level of sales required to achieve specific profit targets. This feature helps organizations set realistic revenue goals and evaluate whether projected sales volumes are sufficient to generate desired returns. Profit planning through break-even analysis supports strategic decision-making and helps businesses align operational activities with financial objectives. As a result, it contributes to improved profitability and long-term business success.

- Assists in Pricing Decisions

Another significant feature of break-even analysis is its role in pricing decisions. By understanding the relationship between selling price, costs, and profitability, managers can determine appropriate pricing strategies. If costs increase, break-even analysis helps estimate how much the selling price should be adjusted to maintain profitability. Similarly, it assists in evaluating the impact of price reductions on sales requirements and profits. This feature enables businesses to make informed pricing decisions that balance competitiveness with financial sustainability, ensuring that products remain profitable while meeting market demands.

- Facilitates Cost Control

Break-even analysis provides valuable insights into cost behavior and facilitates effective cost control. It separates costs into fixed and variable components, helping managers understand how each type of cost affects profitability. By analyzing cost structures, businesses can identify opportunities to reduce unnecessary expenses and improve operational efficiency. This feature supports better resource utilization and helps maintain financial stability. Effective cost control through break-even analysis contributes to lower break-even points, increased profitability, and improved competitiveness in the market, making it an essential tool for financial management.

- Simple and Easy to Understand

One of the key features of break-even analysis is its simplicity. The method is easy to understand and apply because it uses basic financial information such as costs, sales prices, and production volumes. Managers, investors, and students can easily interpret the results without requiring advanced statistical knowledge. Graphical representations such as break-even charts further enhance understanding by visually showing the relationship between costs, revenue, and profits. This simplicity makes break-even analysis a widely used tool for evaluating business performance, planning operations, and making investment decisions.

- Useful for Planning and Decision Making

Break-even analysis is an important planning and decision-making tool. It provides valuable information about the sales volume required to cover costs and achieve profitability. Managers use this information when evaluating investment projects, expanding operations, introducing new products, or making production decisions. The analysis helps compare different alternatives and assess their financial implications. By providing a clear understanding of cost and revenue relationships, break-even analysis supports informed decision-making and reduces uncertainty. This feature makes it an essential component of financial planning, budgeting, and strategic business management.

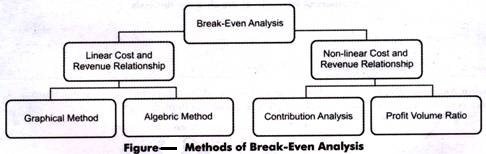

Methods of Break Even Analysis

1. Graphical Method of Break-Even Analysis

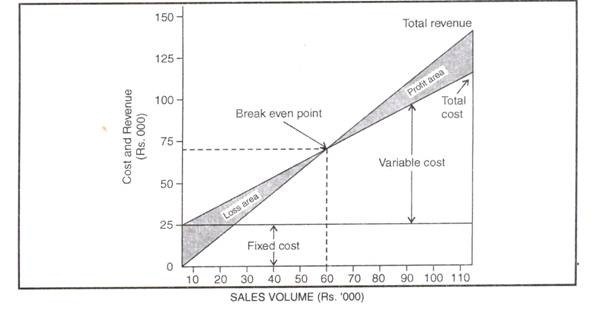

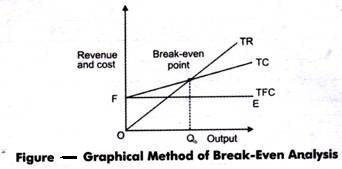

The Graphical Method is a visual technique used to determine the break-even point through a chart known as the Break-Even Chart. In this method, sales volume is represented on the horizontal (X) axis, while costs and revenue are represented on the vertical (Y) axis. Separate lines are drawn for total cost and total revenue. The point where these two lines intersect is called the Break-Even Point (BEP). At this point, total revenue equals total cost, resulting in neither profit nor loss.

The graphical method provides a clear visual representation of profits, losses, and the margin of safety. It helps managers easily understand the relationship between costs, sales, and profitability. Although simple and effective, it may become less accurate when dealing with multiple products or complex cost structures.

Steps in the Graphical Method

- Draw X-axis for sales volume and Y-axis for costs and revenue.

- Plot the fixed cost line.

- Plot the total cost line (Fixed Cost + Variable Cost).

- Plot the total revenue line.

- Identify the intersection point of total cost and total revenue.

- The intersection point represents the Break-Even Point.

Formula Used

Break-Even Point (Units) = Fixed Costs ÷ Contribution per Unit

Example

- Fixed Costs = ₹1,50,000

- Selling Price per Unit = ₹100

- Variable Cost per Unit = ₹70

Contribution per Unit

= ₹100 − ₹70

= ₹30

Break-Even Point

= ₹1,50,000 ÷ ₹30

= 5,000 Units

On the graph, the Total Revenue Line and Total Cost Line intersect at 5,000 units, indicating the break-even point.

As shown in Fig. TFC is equals to FE, which is a fixed cost line. The vertical distance between TC and TFC line equals TVC. As quantity of output increases, the vertical distance between TC and TFC increases. This implies that TVC increases with change in TC and TFC.

Until Qb of the quantity is produced, total cost exceeds the total revenue, which implies that an organization will suffer losses if it produces less than Qb. At Qb output level, total revenue equals total cost. At this point, an organization never makes profit nor loss implying that it is a break-even point. Thus, Qb is a break-even level of output. Producing more than Qb will be profitable for organizations as TR is greater than TC.

2. Algebraic Method of Break-Even Analysis

The Algebraic Method is a mathematical approach used to calculate the break-even point using formulas. It determines the level of sales or production where total revenue equals total cost. This method is more accurate than the graphical method because it provides exact numerical results. It is widely used in financial planning, budgeting, and capital budgeting decisions.

The algebraic method is based on the concept of contribution margin, which is the difference between selling price and variable cost per unit. By dividing fixed costs by contribution per unit, managers can determine the number of units that must be sold to cover all costs. This method is simple, reliable, and suitable for business decision-making.

Formula: Break-Even Point (Units)

BEP = Fixed Costs ÷ Contribution per Unit

Where:

Contribution per Unit = Selling Price − Variable Cost

Break-Even Point (Sales Value)

BEP (Sales) = Fixed Costs ÷ P/V Ratio

Where:

P/V Ratio = (Contribution ÷ Sales) × 100

Example

- Fixed Costs = ₹2,00,000

- Selling Price per Unit = ₹120

- Variable Cost per Unit = ₹80

Step 1: Calculate Contribution

Contribution per Unit

= ₹120 − ₹80

= ₹40

Step 2: Calculate Break-Even Point

BEP

= ₹2,00,000 ÷ ₹40

= 5,000 Units

Interpretation: The company must sell 5,000 units to cover all fixed and variable costs. Any sales beyond this level will generate profit.

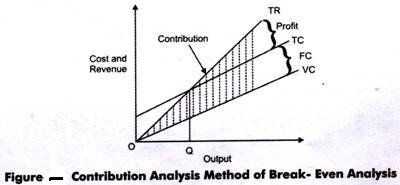

3. Contribution Margin Method

The Contribution Margin Method determines the break-even point by calculating the contribution made by each unit sold toward covering fixed costs. Contribution is the difference between selling price and variable cost per unit. Once fixed costs are fully covered, the remaining contribution becomes profit. This method is widely used because it directly focuses on the profitability of individual products and helps managers evaluate pricing and production decisions.

Formula

Contribution per Unit = Selling Price − Variable Cost

Break-Even Point (Units) = Fixed Costs ÷ Contribution per Unit

Example

- Fixed Costs = ₹2,00,000

- Selling Price = ₹100

- Variable Cost = ₹60

Contribution = ₹40

Break-Even Point

= ₹2,00,000 ÷ ₹40

= 5,000 Units

Fixed costs are addition to variable costs. Thus, TC line is parallel to the variable costs line. In the fig. OQ is the break-even point. TC minus VC equals FC. Below OQ, contribution is less than fixed cost whereas beyond OQ, contribution exceeds faxed cost. The shaded portion between TR and VC is the contribution.

4. Profit-Volume (P/V) Ratio Method

The Profit-Volume Ratio Method uses the contribution-to-sales relationship to determine the break-even point. The P/V ratio indicates how much contribution is generated from each rupee of sales. A higher P/V ratio indicates better profitability and a lower break-even point. This method is particularly useful for comparing products and evaluating the effect of changes in price and costs on profitability.

Formula

P/V Ratio = (Contribution ÷ Sales) × 100

Break-Even Sales = Fixed Costs ÷ P/V Ratio

Example

- Sales = ₹5,00,000

- Contribution = ₹2,00,000

- Fixed Costs = ₹80,000

P/V Ratio

= (2,00,000 ÷ 5,00,000) × 100

= 40%

Break-Even Sales

= ₹80,000 ÷ 40%

= ₹2,00,000

5. Margin of Safety Method

The Margin of Safety Method measures the difference between actual sales and break-even sales. It indicates the extent to which sales can decline before the business starts incurring losses. A higher margin of safety suggests lower risk, while a lower margin indicates greater financial vulnerability. This method helps managers evaluate business stability and assess the risk associated with sales fluctuations.

Formula: Margin of Safety = Actual Sales − Break-Even Sales

Margin of Safety Ratio = (Margin of Safety ÷ Actual Sales) × 100

Example

- Actual Sales = ₹8,00,000

- Break-Even Sales = ₹5,00,000

Margin of Safety

= ₹8,00,000 − ₹5,00,000

= ₹3,00,000

Margin of Safety Ratio

= (₹3,00,000 ÷ ₹8,00,000) × 100

= 37.5%

6. Cash Break-Even Analysis

Cash Break-Even Analysis focuses only on cash expenses and excludes non-cash costs such as depreciation. It determines the level of sales required to cover cash operating costs. This method is particularly useful for evaluating liquidity and ensuring that the business can meet its cash obligations. It is often used in project appraisal and financial planning where cash flow considerations are important.

Formula: Cash Break-Even Point = Cash Fixed Costs ÷ Contribution per Unit

Example

- Cash Fixed Costs = ₹1,20,000

- Contribution per Unit = ₹40

Cash Break-Even Point

= ₹1,20,000 ÷ ₹40

= 3,000 Units

This means the business must sell 3,000 units to cover all cash expenses.

7. Multi-Product Break-Even Analysis

Multi-Product Break-Even Analysis is used when a company sells more than one product. Since different products have different contribution margins, a weighted average contribution is calculated. This method helps determine the combined sales level required to achieve break-even for the entire product mix. It is particularly useful for diversified businesses with multiple product lines.

Formula: Break-Even Point = Fixed Costs ÷ Weighted Average Contribution

Example

- Fixed Costs = ₹4,00,000

- Weighted Average Contribution = ₹80

Break-Even Point

= ₹4,00,000 ÷ ₹80

= 5,000 Units

The company must collectively sell 5,000 units of its product mix to break even.

8. Analytical Break-Even Method

The Analytical Break-Even Method combines financial calculations and managerial analysis to determine the break-even point and evaluate profitability. It considers changes in costs, prices, production levels, and market conditions. This method provides a deeper understanding of financial performance and supports strategic decision-making. Managers often use it for long-term planning and evaluating alternative business strategies.

Formula: Break-Even Point = Fixed Costs ÷ Contribution Margin

Example

- Fixed Costs = ₹3,00,000

- Contribution Margin = ₹60 per unit

Break-Even Point

= ₹3,00,000 ÷ ₹60

= 5,000 Units

This analysis helps managers understand how operational changes affect profitability and risk.

Importance of Break-Even Analysis

- Helps in Determining Minimum Sales Requirement

Break-even analysis helps businesses determine the minimum level of sales required to cover all fixed and variable costs. By identifying the break-even point, managers can set realistic sales targets and ensure that operations remain financially sustainable. It provides a clear understanding of how much revenue is needed before profits can be earned. This information is particularly useful for new businesses and investment projects, as it helps assess feasibility and financial viability. Therefore, break-even analysis serves as an essential tool for planning sales strategies and avoiding potential losses.

- Assists in Profit Planning

A significant importance of break-even analysis is its role in profit planning. Once the break-even point is known, managers can estimate the additional sales required to achieve specific profit objectives. This enables businesses to establish realistic financial goals and develop strategies to attain them. Profit planning also helps in budgeting, forecasting, and evaluating future business performance. By understanding the relationship between sales volume and profitability, organizations can make better operational decisions. Thus, break-even analysis supports effective profit management and contributes to long-term financial success.

- Facilitates Pricing Decisions

Break-even analysis plays an important role in determining appropriate pricing policies. It helps managers understand how changes in selling prices affect profitability and the break-even point. If production costs increase, businesses can evaluate whether price adjustments are necessary to maintain profits. Similarly, before offering discounts or promotional pricing, managers can assess the impact on sales requirements. This information helps organizations balance competitiveness and profitability. Therefore, break-even analysis provides valuable guidance for setting prices that support both market demand and financial objectives.

- Supports Cost Control

Another important benefit of break-even analysis is its contribution to cost control. By separating costs into fixed and variable components, it helps managers identify areas where expenses can be reduced. Understanding cost behavior allows businesses to improve operational efficiency and manage resources more effectively. Cost control is essential for lowering the break-even point and increasing profitability. Managers can evaluate the impact of cost-saving measures and make informed decisions regarding production processes. Consequently, break-even analysis promotes better financial management and enhances the overall performance of the organization.

- Measures Business Risk

Break-even analysis is an effective tool for measuring the risk associated with a business or project. A high break-even point indicates greater risk because higher sales volumes are required to cover costs. Conversely, a lower break-even point suggests lower risk and greater financial stability. By assessing risk levels, managers can evaluate the feasibility of investment projects and make informed decisions. This understanding helps businesses prepare for market fluctuations and economic uncertainties. Therefore, break-even analysis contributes significantly to risk assessment and financial planning.

- Aids in Capital Budgeting Decisions

In capital budgeting, break-even analysis helps managers evaluate investment projects by estimating the sales volume needed to recover costs. It provides valuable information about project feasibility and profitability before large investments are made. By comparing the break-even points of different projects, businesses can select the most suitable investment opportunities. This analysis reduces uncertainty and improves decision-making regarding long-term investments. As a result, break-even analysis supports efficient allocation of resources and contributes to the achievement of organizational objectives.

- Assists in Business Planning and Forecasting

Break-even analysis is an important planning and forecasting tool. It helps businesses estimate future sales requirements, revenue targets, and production levels. Managers can use the information to prepare budgets, allocate resources, and develop strategic plans. Forecasting future performance becomes easier when the relationship between costs, sales, and profits is clearly understood. This enables organizations to anticipate challenges and respond proactively to changing market conditions. Therefore, break-even analysis enhances planning accuracy and supports effective business management.

- Improves Decision Making

One of the greatest advantages of break-even analysis is that it improves managerial decision-making. It provides reliable information regarding costs, revenues, profitability, and risk, enabling managers to make informed choices. Decisions related to pricing, production, expansion, product launches, and investment projects can be evaluated more effectively using break-even analysis. By reducing uncertainty and providing a clear financial picture, it enhances confidence in decision-making. Consequently, break-even analysis contributes to better financial performance, efficient resource utilization, and sustainable business growth.

Limitations of Break-Even Analysis

- Assumes Constant Selling Price

One major limitation of break-even analysis is that it assumes the selling price of a product remains constant at all levels of sales. In reality, businesses often change prices due to competition, market demand, discounts, seasonal variations, and economic conditions. A reduction in selling price can increase the break-even point, while a price increase may reduce it. Since actual market conditions rarely remain stable, this assumption limits the accuracy of break-even analysis. Therefore, the results obtained may not always reflect real business situations and profitability levels.

- Assumes Fixed and Variable Costs Remain Constant

Break-even analysis assumes that fixed costs and variable costs remain unchanged over the relevant range of production and sales. However, in practice, costs may change due to inflation, wage increases, changes in raw material prices, technological developments, or operational inefficiencies. Fixed costs may rise with business expansion, and variable costs may fluctuate depending on production volume. Because cost behavior is not always stable, the assumptions of break-even analysis may not accurately represent actual business conditions. This reduces its reliability for long-term financial planning and decision-making.

- Ignores Changes in Market Conditions

Another limitation of break-even analysis is that it does not consider changing market conditions. Factors such as competition, consumer preferences, economic cycles, government policies, and technological developments can significantly affect sales and profitability. The analysis assumes that products can be sold at expected levels without considering market uncertainties. In reality, businesses operate in dynamic environments where demand and supply conditions continuously change. Since break-even analysis ignores these external influences, it provides only a simplified view of profitability and may lead to inaccurate conclusions.

- Assumes All Units Produced Are Sold

Break-even analysis assumes that all units produced are sold immediately. This assumption simplifies calculations but does not always reflect actual business operations. Companies often maintain inventories due to seasonal demand, production scheduling, or market conditions. Unsold goods increase storage costs and affect cash flows. If production exceeds sales, the break-even calculations may not accurately indicate profitability. Therefore, the assumption that production and sales volumes are equal limits the practical applicability of break-even analysis, especially in businesses where inventory management plays a significant role.

- Not Suitable for Multi-Product Businesses

Break-even analysis is relatively simple when a company produces a single product. However, it becomes more complicated when multiple products with different selling prices, costs, and contribution margins are involved. In such cases, determining a single break-even point requires assumptions regarding product mix and sales proportions. Changes in the sales mix can significantly affect profitability and break-even calculations. Therefore, break-even analysis may not provide accurate results for diversified businesses. This limitation reduces its usefulness in organizations offering a wide range of products and services.

- Ignores the Time Value of Money

A significant limitation of break-even analysis is that it ignores the time value of money. The method treats all revenues and costs as if they occur at the same point in time. In reality, money received today is more valuable than money received in the future because of inflation and investment opportunities. Since break-even analysis does not discount future cash flows, it may not accurately evaluate long-term projects. This limitation is particularly important in capital budgeting, where timing of cash flows significantly affects investment decisions and project profitability.

- Oversimplifies Business Reality

Break-even analysis simplifies complex business operations by focusing primarily on costs, sales volume, and profits. It assumes predictable relationships among these variables and ignores many factors that influence business performance. Issues such as employee productivity, customer satisfaction, product quality, technological advancements, and management efficiency are not considered. Because actual business environments are far more complex, break-even analysis may provide an incomplete picture of financial performance. Therefore, it should be used alongside other analytical tools rather than as the sole basis for decision-making.

- Limited Usefulness for Long-Term Planning

Break-even analysis is generally more suitable for short-term decision-making than long-term planning. Over extended periods, changes in technology, consumer preferences, inflation, competition, and government regulations can significantly alter costs and revenues. The assumptions used in break-even calculations may no longer remain valid in the future. As a result, break-even estimates may become inaccurate over time. Therefore, while the technique is useful for operational planning and short-term decisions, its effectiveness is limited when evaluating long-term business strategies and investment projects.

4 thoughts on “Break Even Analysis, Meaning, Formula, Features, Methods, Importance and Limitations”