Cost of Capital, Introduction, Meaning, Definitions, Features, Sources, Significance, Types and Advantages

by

by Cost of Capital is the required return necessary to make a capital budgeting project, such as building a new factory, worthwhile. When analysts and investors discuss the cost of capital, they typically mean the weighted average of a firm’s cost of debt and cost of equity blended together.

As it is evident from the name, cost of capital refers to the weighted average cost of various capital components, i.e. sources of finance, employed by the firm such as equity, preference or debt. In finer terms, it is the rate of return, that must be received by the firm on its investment projects, to attract investors for investing capital in the firm and to maintain its market value.

The factors which determine the cost of capital are:

- Source of finance

- Corresponding payment for using finance

On raising funds from the market, from various sources, the firm has to pay some additional amount, apart from the principal itself. The additional amount is nothing but the cost of using the capital, i.e. cost of capital which is either paid in lump sum or at periodic intervals.

Meaning of Cost of Capital

The Cost of Capital refers to the minimum rate of return that a business must earn on its investments to maintain its market value and satisfy its investors. It represents the cost of obtaining funds—whether through equity, debt, or retained earnings—to finance business operations or projects. In simple terms, it is the price a firm pays for using financial resources.

Since different sources of finance have different costs, the cost of capital helps managers choose the most economical mix. It also serves as a benchmark for evaluating investment proposals and determining whether a project will add value to the firm. A project is considered beneficial only if it earns more than its cost of capital. Thus, it is an essential tool in financial planning, capital budgeting, and corporate decision-making.

Definitions Cost of Capital

1. According to Solomon Ezra

“Cost of capital is the minimum return a firm must earn on its investments to keep its market value unchanged.”

2. According to James C. Van Horne

“Cost of capital is the required rate of return that a firm must achieve to cover all its financing costs.”

3. According to John J. Hampton

“Cost of capital is the rate of return the firm must earn on its investment projects to maintain the market value of its shares.”

4. According to Gitman

“Cost of capital is the firm’s weighted average cost of the various sources of funds used.”

5. General Definition

Cost of capital is the opportunity cost of using funds for a specific purpose, representing the return that could have been earned if funds were invested elsewhere.

Features of Cost of Capital

- Minimum Required Rate of Return

Cost of capital represents the minimum rate of return that a company must earn on its investments to satisfy investors and creditors. It serves as a benchmark against which the profitability of projects is measured. If the return generated by a project is lower than the cost of capital, the investment may reduce shareholder wealth and should generally be rejected. This feature helps management make informed investment decisions and ensures that funds are allocated only to projects capable of generating adequate returns. Thus, it acts as a fundamental standard for evaluating financial performance and investment opportunities.

- Based on Investor Expectations

The cost of capital is largely determined by the expectations of investors who provide funds to the company. Shareholders expect dividends and capital appreciation, while lenders expect timely interest payments and repayment of principal. These expectations vary according to the level of risk associated with the investment. Higher risk generally leads to higher expected returns and, consequently, a higher cost of capital. This feature highlights the importance of understanding investor behavior and market perceptions. Companies must meet these expectations to attract and retain capital from investors and maintain their financial reputation.

- Composed of Different Sources of Finance

Cost of capital is not derived from a single source but consists of the costs associated with various financing sources. These sources include equity shares, preference shares, debentures, long-term loans, and retained earnings. Each source has a different cost because the risks and return expectations vary among providers of capital. The overall cost of capital is determined by combining the individual costs of these sources. This feature emphasizes the need for companies to carefully analyze the cost of each financing option before making capital structure decisions. Proper management of financing sources can reduce overall capital costs.

- Forward-Looking Concept

Cost of capital is a future-oriented concept because it is based on expected returns rather than past performance. Investors provide funds with the expectation of earning future benefits, and companies evaluate projects based on anticipated cash flows. Therefore, the cost of capital reflects future market conditions, risk levels, and return expectations. This feature makes it an essential tool in financial planning and forecasting. By considering future possibilities, businesses can make strategic decisions that improve long-term profitability and sustainability. It helps management focus on future growth opportunities rather than relying solely on historical financial data.

- Influenced by Risk

Risk is one of the most significant factors affecting the cost of capital. Investors demand higher returns when they perceive greater uncertainty regarding future earnings and cash flows. Business risk, financial risk, market risk, and economic risk all contribute to variations in the cost of capital. A company operating in a stable industry may enjoy a lower cost of capital, while a firm facing uncertain conditions may experience higher financing costs. This feature highlights the direct relationship between risk and required return. Effective risk management can help reduce the cost of capital and improve financial performance.

- Dynamic and Flexible in Nature

The cost of capital is not constant; it changes according to economic conditions, market trends, interest rates, inflation, and company performance. As these factors fluctuate, investor expectations and borrowing costs also change. For example, rising interest rates increase the cost of debt, while favorable market conditions may reduce the cost of equity. This dynamic nature requires companies to continuously monitor financial markets and update their calculations. The flexibility of the cost of capital ensures that financial decisions remain relevant and realistic. Businesses must adapt their strategies to changing circumstances to maintain financial efficiency.

- Basis for Capital Budgeting Decisions

One of the most important features of the cost of capital is its use in capital budgeting decisions. It serves as the discount rate for evaluating investment proposals through techniques such as Net Present Value (NPV) and Internal Rate of Return (IRR). Projects that generate returns exceeding the cost of capital are generally accepted because they add value to the firm. Conversely, projects with lower returns are rejected. This feature helps ensure efficient allocation of financial resources and supports wealth maximization objectives. By providing a clear benchmark, the cost of capital improves the quality of investment decision-making.

- Helps in Determining Optimal Capital Structure

Cost of capital plays a crucial role in designing an optimal capital structure. Companies seek a combination of debt and equity that minimizes the overall cost of capital while maximizing firm value. Excessive reliance on debt may increase financial risk, whereas excessive equity financing may be expensive due to higher shareholder expectations. By analyzing the costs of different financing sources, management can determine the most economical mix of funds. This feature contributes to efficient financial management and enhances long-term profitability. An optimal capital structure enables businesses to achieve financial stability and competitive advantage.

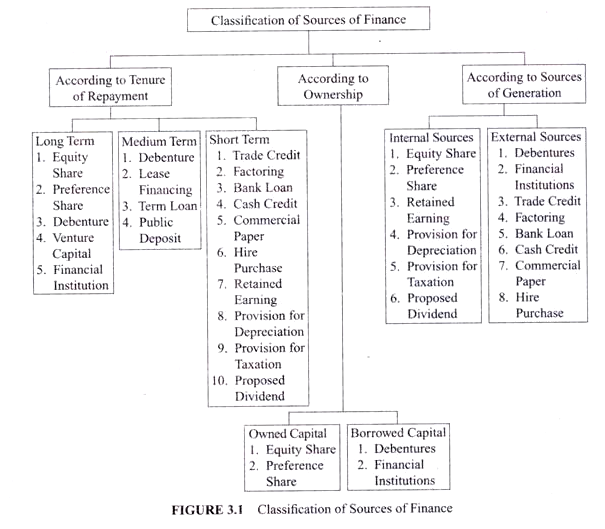

Sources of Capital

1. Equity Share Capital

Equity share capital is one of the most important sources of long-term finance for a company. It is raised by issuing shares to investors who become owners of the business. Equity shareholders have voting rights and participate in major company decisions. They receive dividends based on the company’s profitability, but dividend payments are not compulsory. Since there is no obligation to repay equity capital during the life of the company, it is considered a permanent source of finance. Equity capital strengthens the financial base of a company and helps in raising additional funds from other sources.

2. Preference Share Capital

Preference share capital is obtained by issuing preference shares to investors who receive a fixed rate of dividend. Preference shareholders enjoy priority over equity shareholders in receiving dividends and repayment of capital during liquidation. However, they generally do not possess voting rights in company management. Preference shares are useful for companies that need long-term funds without significantly affecting ownership control. They combine features of both equity and debt financing. This source helps companies raise capital while maintaining financial flexibility and reducing the burden of sharing management powers with additional equity shareholders.

3. Retained Earnings

Retained earnings are profits that a company keeps within the business instead of distributing them as dividends to shareholders. This is an internal source of finance and does not require borrowing or issuing new securities. Retained earnings provide funds for expansion, modernization, research, and business development. Since there are no interest payments or flotation costs involved, it is one of the most economical sources of capital. It improves the company’s financial strength and reduces dependence on external funding. Efficient utilization of retained earnings contributes significantly to long-term growth and financial stability.

4. Debentures

Debentures are long-term debt instruments issued by companies to raise funds from investors. Debenture holders are creditors of the company and receive a fixed rate of interest regardless of business profits. They do not have ownership rights or voting powers. Debentures may be secured or unsecured and are generally redeemed after a specified period. They provide a reliable source of long-term finance at a comparatively lower cost than equity capital. Companies often use debentures for financing expansion projects, purchasing fixed assets, and meeting capital expenditure requirements while retaining ownership control.

5. Term Loans from Banks and Financial Institutions

Term loans are borrowed funds obtained from commercial banks and financial institutions for a fixed period. These loans are generally used to finance long-term assets such as land, buildings, machinery, and equipment. Borrowers are required to repay the principal amount along with interest according to agreed schedules. Term loans provide substantial capital for business expansion and modernization. They are flexible and can be tailored to meet specific financing needs. This source is widely preferred because it offers predictable repayment terms and allows businesses to access large amounts of funds efficiently.

6. Public Deposits

Public deposits are funds raised directly from the public by companies for a specified period at a predetermined rate of interest. This source of finance is particularly useful for meeting medium-term financial requirements. Public deposits are often less expensive than institutional loans and involve fewer formalities. They help companies diversify their funding sources and reduce dependence on banks. However, maintaining investor confidence is essential for successfully attracting deposits. Companies must comply with regulatory guidelines and ensure timely repayment to maintain their reputation and financial credibility among depositors.

7. Trade Credit

Trade credit is a short-term source of finance provided by suppliers who allow businesses to purchase goods and services on credit. Instead of making immediate payment, the buyer pays after an agreed credit period. Trade credit is a convenient and flexible method of financing day-to-day business operations. It helps maintain working capital and improves cash flow management. This source does not usually require collateral or complex documentation. Small and large businesses alike depend on trade credit to support inventory purchases and operational needs, making it a vital component of business financing.

8. Commercial Paper

Commercial paper is an unsecured short-term money market instrument issued by financially sound companies to raise funds. It is usually issued at a discount and redeemed at face value upon maturity. Commercial paper is commonly used to meet working capital requirements and other short-term financial obligations. Because it is unsecured, only companies with strong credit ratings can issue it successfully. This source offers lower borrowing costs compared to traditional bank loans and provides flexibility in obtaining funds. Commercial paper plays an important role in efficient corporate cash management and liquidity planning.

9. Venture Capital

Venture capital is a source of finance provided to startups and high-growth businesses with innovative ideas and strong future potential. Venture capitalists invest funds in exchange for an ownership stake in the company. In addition to financial support, they often provide managerial expertise, strategic guidance, and industry connections. Venture capital is especially useful for businesses that may not qualify for traditional bank financing due to high risk or lack of operating history. It encourages innovation, entrepreneurship, and business development. Many successful companies have achieved rapid growth with the assistance of venture capital funding.

10. Lease Financing

Lease financing is an arrangement in which a business acquires the right to use an asset without purchasing it outright. The lessee pays periodic lease rentals to the owner of the asset, known as the lessor. Leasing is commonly used for machinery, equipment, vehicles, and technology assets. It helps businesses conserve cash and avoid large initial investments. Lease financing provides flexibility, facilitates access to modern equipment, and reduces the risk of technological obsolescence. This source is particularly beneficial for companies seeking to expand operations while preserving working capital and maintaining financial liquidity.

Significance of Cost of Capital

-

Capital Allocation and Project Evaluation

The cost of capital is paramount in capital allocation decisions. Companies must decide where to invest their limited resources, and the cost of capital serves as a benchmark for evaluating potential projects. By comparing the expected returns of a project with the cost of capital, firms can make informed investment decisions that align with shareholder value maximization.

-

Financial Performance Measurement

It serves as a yardstick for assessing financial performance. A company’s ability to generate returns above its cost of capital indicates operational efficiency and effective resource utilization. Shareholders and investors often scrutinize this metric as it reflects the company’s capacity to create value and generate sustainable profits.

-

Cost of Debt and Equity Balancing

The cost of capital guides the balance between debt and equity in a firm’s capital structure. As companies strive to minimize their overall cost of capital, they navigate the trade-off between the lower cost of debt and the potential risks associated with increased leverage. Striking the right balance ensures an optimal capital structure that minimizes costs while maintaining financial flexibility.

-

Investor Expectations and Market Perception

It influences investor expectations and market perception. A company’s cost of capital is indicative of the returns investors require for providing funds. If a company consistently exceeds or falls short of this benchmark, it can impact investor confidence and influence stock prices. Managing and meeting these expectations are crucial for maintaining a positive market perception.

-

Risk Management

The cost of capital integrates risk considerations. The cost of equity, for instance, incorporates the risk premium investors demand for investing in a particular stock. Understanding these risk components aids in strategic decision-making and risk management. Companies can adjust their capital structure and investment strategies to mitigate risk and align with their cost of capital.

-

Capital Structure Optimization

It facilitates capital structure optimization. Achieving the right mix of debt and equity is essential for minimizing the cost of capital. Firms aim to find the optimal capital structure that maximizes shareholder value. This involves assessing the impact of various financing options on the overall cost of capital and choosing the combination that minimizes this metric.

-

Market Competitiveness

The cost of capital impacts a company’s competitiveness. In industries where access to capital is a critical factor, having a lower cost of capital can provide a competitive advantage. This advantage enables companies to undertake projects and investments that might be financially unfeasible for competitors with higher capital costs.

- Dividend Policy and Shareholder Returns

It guides dividend policy. Companies consider the cost of capital when determining whether to distribute profits as dividends or reinvest in the business. This decision affects shareholder returns and influences the overall attractiveness of the company’s stock to investors.

- Economic Value Added (EVA) and Shareholder Wealth

The cost of capital is integral to Economic Value Added (EVA), a measure of a company’s ability to generate wealth for shareholders. By deducting the cost of capital from the Net Operating Profit After Taxes (NOPAT), EVA provides a clear picture of whether a company is creating or eroding shareholder value.

- Strategic Planning and Long-Term Viability

It informs strategic planning and ensures long-term viability. By aligning investment decisions with the cost of capital, companies can focus on projects that contribute most significantly to shareholder value over the long term. This strategic alignment is crucial for sustainable growth and maintaining a competitive edge in the dynamic business environment.

Types of Cost of Capital

- Explicit Cost of Capital

Explicit cost refers to the actual, measurable cost a firm incurs to obtain funds. It is calculated as the rate of return required by investors or lenders. For example, interest paid on loans or dividends paid on preference shares represent explicit costs. This cost reflects the discount rate that equates the present value of cash inflows with the present value of cash outflows. It helps managers understand the real cost of raising funds from various sources for decision-making.

- Implicit Cost of Capital

Implicit cost represents the opportunity cost associated with choosing one financing option over another. It does not involve direct payment but reflects the return foregone by employing funds internally instead of investing them elsewhere. For instance, using retained earnings for a new project instead of distributing dividends involves an implicit cost equal to shareholders’ required return. It is crucial for evaluating internal financing decisions and ensures that resources are allocated to the best-returning opportunities.

- Specific Cost of Capital

Specific cost refers to the individual cost associated with each source of finance such as equity, debt, preference shares, or retained earnings. Since each source has different risk levels and expectations, their specific costs vary. For example, debt has interest cost, while equity has dividend expectations. Calculating specific costs helps a firm assess the relative cost-effectiveness of each financing option before deciding how much of each component to include in its capital structure.

- Composite or Weighted Average Cost of Capital (WACC)

WACC represents the average cost of all capital sources, weighted according to their proportion in the firm’s capital structure. It blends debt, equity, and other financing costs to show the overall required return for the business. WACC is essential for investment decisions, valuation of projects, and determining whether a project will create or destroy value. A lower WACC indicates cheaper financing and greater potential for profitable investments, making it a core measure in financial management.

- Marginal Cost of Capital

Marginal cost refers to the cost of raising one additional unit of capital. It changes as the company raises more funds, often increasing when attractive financing options are exhausted. It is important for decisions regarding incremental investments because it captures the current cost of acquiring new funds, not historical averages. Marginal cost helps firms determine the feasibility of expanding operations or initiating new projects under current market conditions, ensuring optimal financing decisions.

- Average Cost of Capital

Average cost of capital is the simple average of costs from all capital sources, without applying weights. It provides a basic overview of the cost of funds but is less accurate than WACC, as it ignores proportional contributions of each source. This measure is sometimes used for quick estimations or in businesses where capital structure is fairly uniform. Although not ideal for major investment decisions, it is useful for preliminary evaluations and comparisons across firms.

- Historical Cost of Capital

Historical cost refers to the cost incurred in the past to raise existing capital. It is derived from previous financing arrangements and reflects conditions that existed at that time. While historical cost helps evaluate past financing policies, it is not reliable for future decision-making since market conditions, interest rates, and investor expectations change. It is mainly used for performance analysis, auditing, and understanding trends in the firm’s financial strategy over time.

- Future or Opportunity Cost of Capital

Future cost represents the expected cost of funds that the firm anticipates in the future. It considers projected market conditions, interest rate trends, investor expectations, and risk levels. Future cost is vital for strategic planning, capital budgeting, and forecasting the viability of long-term projects. By estimating future financing costs, firms can better manage risk, debt levels, and growth opportunities, ensuring financial stability and competitive advantage in dynamic markets.

Advantages of Cost of Capital

- Helps in Capital Budgeting Decisions

Cost of capital acts as a benchmark or discount rate for evaluating investment proposals. It helps firms determine whether a project will generate returns greater than the minimum required return. When the internal rate of return (IRR) is higher than the cost of capital, the project is accepted. Thus, it ensures that scarce financial resources are allocated to value-creating investments, improving long-term profitability and strategic growth.

- Aids in Designing an Optimal Capital Structure

A clear understanding of cost of capital enables firms to choose the most cost-effective mix of debt and equity. Companies can compare the costs and risks of each source and design a structure that minimizes the Weighted Average Cost of Capital (WACC). When WACC is minimized, firm value maximizes. This promotes efficient financing decisions and ensures that the company maintains a balanced, stable, and sustainable capital structure.

- Helps in Measuring Financial Performance

Cost of capital is a useful tool for assessing the performance of management and the effectiveness of financial decisions. By comparing actual returns with the cost of capital, firms can determine whether they are generating sufficient value for shareholders. It highlights whether operations are meeting expected standards and helps identify areas requiring improvement. Thus, it supports accountability, transparency, and improved financial discipline within the organization.

- Useful for Dividend Policy Decisions

Cost of equity, which is part of overall cost of capital, guides decisions relating to dividend distribution. Management can determine whether retained earnings will generate higher returns than the cost of equity. If returns exceed cost, retention is justified; otherwise, dividends should be paid. This ensures that shareholders’ wealth is maximized and that the firm’s earnings are used in the most efficient and profitable manner, balancing growth and investor expectations.

- Facilitates Better Financing Decisions

Cost of capital helps firms choose between alternative financing options such as debt, equity, preference shares, or retained earnings. By comparing the specific costs of each source, companies can select the one that offers the lowest financing cost with acceptable risk. This leads to efficient resource utilization, better financial planning, and stronger control over funding expenses. It also helps firms maintain financial stability and competitiveness in dynamic markets.

- Enhances Shareholders’ Wealth Maximization

A firm that effectively manages its cost of capital can increase its market value. Lowering the cost of capital increases the net present value (NPV) of future cash flows, making the firm more attractive to investors. When investment decisions consistently generate returns above the cost of capital, shareholders’ wealth increases. Thus, understanding and managing cost of capital directly supports the primary financial goal of maximizing shareholders’ wealth.

- Helps in Business Valuation

Cost of capital is a key input in valuation models such as Discounted Cash Flow (DCF). It serves as the discount rate to calculate the present value of future earnings. A lower cost of capital increases valuation, while a higher cost decreases it. Accurate valuation is essential for mergers, acquisitions, financial restructuring, and assessing the fair value of shares. Thus, cost of capital ensures more reliable and realistic valuation outcomes.

- Supports Long-Term Strategic Planning

Cost of capital provides insights into future financing costs, risk levels, and expected returns, helping firms shape their long-term financial strategies. It guides decisions regarding expansion, diversification, new ventures, and technological investments. By understanding the cost of acquiring funds, companies can align their plans with financial capabilities and market expectations. This leads to sustainable growth and effective strategic decision-making, ensuring long-term competitiveness and stability.