Business Environment, Meaning, Characteristics, Scope, Significance, Components

by

by Business Environment encompasses all internal and external factors that affect the operations and performance of a company. Internally, this includes elements such as organizational culture, management structure, and resources. Externally, it involves factors like economic conditions, market trends, technological advancements, legal and regulatory frameworks, and socio-cultural influences. A favorable business environment can foster growth and innovation, while unfavorable conditions may pose challenges and risks. Companies often conduct thorough analyses of the business environment to make informed decisions, mitigate risks, and seize opportunities, ultimately shaping their strategies and outcomes in the competitive landscape.

Significance of Business Environment:

-

Strategic Planning:

Understanding the business environment helps in formulating effective strategies by identifying opportunities and threats. Businesses can capitalize on favorable conditions and prepare for challenges.

-

Risk Management:

Assessing the business environment enables businesses to anticipate risks and take proactive measures to mitigate them. This includes regulatory changes, economic fluctuations, and competitive pressures.

-

Competitive Advantage:

A deep understanding of the business environment allows companies to differentiate themselves from competitors. By leveraging unique opportunities and adapting to market dynamics, they can gain a competitive edge.

- Innovation:

The business environment often presents opportunities for innovation. By staying abreast of technological advancements, market trends, and consumer preferences, businesses can develop innovative products and services to meet evolving demands.

- Adaptability:

Business environment is dynamic and constantly evolving. Businesses that are adaptable and responsive to changes can thrive amidst uncertainty and volatility.

-

Regulatory Compliance:

Compliance with legal and regulatory requirements is crucial for business sustainability. Understanding the regulatory landscape helps businesses navigate complex legal frameworks and avoid penalties.

-

Resource Allocation:

Knowledge of the business environment guides effective resource allocation. Businesses can allocate resources such as capital, manpower, and technology strategically to capitalize on opportunities and address challenges.

-

Stakeholder Management:

Businesses operate within a network of stakeholders including customers, investors, employees, and communities. Understanding the business environment enables businesses to effectively engage with stakeholders and build mutually beneficial relationships.

Characteristics of the Business Environment:

- Dynamic:

Business environment is constantly changing due to factors such as technological advancements, market trends, and regulatory developments. This dynamism requires businesses to remain flexible and adaptable.

- Uncertain:

Business environment is inherently uncertain, with factors such as economic fluctuations, political instability, and unexpected events influencing operations and outcomes. Businesses must manage and mitigate uncertainties to minimize risks.

- Competitive:

Competition is a defining characteristic of the business environment. Companies must contend with rivals for market share, customers, and resources, driving innovation, efficiency, and strategic positioning.

- Interconnected:

Various elements of the business environment are interconnected and interdependent. Changes in one area, such as economic conditions or consumer preferences, can have ripple effects across industries and regions.

- Multi-dimensional:

Business environment encompasses a wide range of dimensions, including economic, social, political, technological, legal, and environmental factors. Businesses must consider the interactions and impacts of these dimensions on their operations.

- Global:

In an increasingly interconnected world, the business environment extends beyond national boundaries. Globalization has opened up opportunities and challenges for businesses to operate in diverse markets and cultures.

- Regulatory:

Regulations and laws shape the business environment by governing aspects such as trade, labor relations, environmental protection, and consumer rights. Compliance with regulatory requirements is essential for business operations and sustainability.

- Opportunistic:

Despite challenges, the business environment also presents opportunities for growth, innovation, and expansion. Businesses must proactively identify and capitalize on opportunities to achieve success amidst dynamic and competitive conditions.

Scope of the Business Environment:

-

Economic Environment:

Factors such as economic growth, inflation, interest rates, exchange rates, and fiscal policies impact business decisions, demand for goods and services, and overall market conditions.

-

Social and Cultural Environment:

Demographic trends, cultural norms, lifestyle changes, and societal values influence consumer behavior, market preferences, and business strategies.

-

Political and Legal Environment:

Government policies, regulations, political stability, taxation, trade policies, and legal frameworks shape the operating environment for businesses, affecting market entry, competition, and compliance requirements.

-

Technological Environment:

Advances in technology, innovation, automation, and digitalization impact business processes, product development, service delivery, and competitiveness in the market.

-

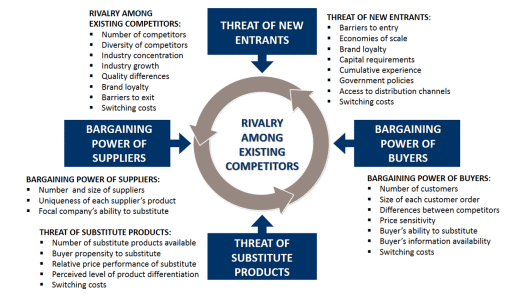

Competitive Environment:

Industry structure, market dynamics, competitor actions, and bargaining power of suppliers and customers define the competitive landscape within which businesses operate.

-

Natural Environment:

Environmental factors such as climate change, natural disasters, resource availability, and sustainability concerns influence business operations, supply chains, and corporate responsibility practices.

-

Global Environment:

Globalization, international trade, geopolitical developments, and cross-border interactions present opportunities and challenges for businesses operating in diverse markets and regions.

Components of Business Environment:

-

Economic Environment

The economic environment refers to all the external economic factors that influence a business’s operations and decisions. It includes elements such as the level of economic development, economic policies, interest rates, inflation, taxation system, monetary and fiscal policies, income distribution, and the overall economic stability of a country. Businesses depend heavily on the economic conditions of a nation, as they directly affect demand, supply, costs, and profitability. For example, during inflation, purchasing power decreases, leading to a fall in demand, while low interest rates may encourage investment. A stable and growing economy offers opportunities for expansion, while economic instability poses risks. Thus, understanding the economic environment helps managers in planning, forecasting, and adopting strategies for sustainable growth.

-

Political Environment

The political environment consists of laws, regulations, government policies, and the overall political stability of a country. It includes the ideology of the ruling party, the government’s attitude towards businesses, and the extent of state intervention in the economy. Political decisions influence taxation, trade policies, labor laws, industrial licensing, and foreign investments. A politically stable nation encourages business confidence, while instability or frequent policy changes create uncertainty and risk. For example, a government that supports liberalization, privatization, and globalization encourages entrepreneurship and foreign investments. On the other hand, restrictive trade policies and high regulation may discourage business operations. Therefore, businesses must monitor political trends closely, as their survival and growth often depend on political support and legal frameworks.

-

Social Environment

The social environment refers to the cultural, demographic, and social values within which businesses operate. It includes traditions, customs, beliefs, lifestyles, population growth, education levels, income distribution, attitudes toward work, and consumer preferences. These factors determine the demand for goods and services and influence workforce behavior. For example, in societies with a growing youth population, there is higher demand for technology, fashion, and entertainment products. Similarly, rising health consciousness creates opportunities for fitness and organic food industries. Understanding social trends helps businesses align their products, marketing strategies, and human resource policies. Failure to adapt to social changes can result in business failure, as customer expectations and societal values directly shape business success.

-

Technological Environment

The technological environment refers to the scientific advancements, innovations, and technological changes that impact businesses. It includes automation, artificial intelligence, digitalization, research and development, new production methods, and communication technologies. Rapid technological progress can make existing products or processes obsolete while creating opportunities for new business models. For example, the rise of e-commerce platforms has transformed retail, while automation and robotics have changed manufacturing. Businesses that adopt the latest technologies gain a competitive edge, improve efficiency, reduce costs, and enhance customer satisfaction. Conversely, businesses that fail to adapt may lose market share. Thus, continuous monitoring and investment in technology are crucial for long-term competitiveness and survival in a dynamic business environment.

-

Legal Environment

The legal environment includes the set of laws, regulations, rules, and judicial decisions that govern business operations. It covers areas such as consumer protection, labor laws, company law, environmental regulations, taxation policies, foreign trade regulations, and competition law. Compliance with legal provisions is mandatory for businesses to operate smoothly, avoid penalties, and maintain goodwill. For example, consumer protection laws safeguard buyers from unfair practices, while labor laws ensure fair wages and working conditions. Legal reforms, such as GST implementation in India, significantly influence business strategies. An unpredictable legal framework can increase risks and operational difficulties. Hence, businesses must stay updated with changing laws and ensure full compliance to operate ethically, sustainably, and without disruption.

-

Environmental/Natural Environment

The natural environment refers to ecological and geographical factors that affect business operations. It includes availability of natural resources, climate conditions, environmental policies, sustainability issues, and ecological balance. Increasing awareness of environmental protection and sustainable development has made businesses more accountable for their impact on nature. Issues like pollution control, waste management, renewable energy use, and climate change have become central to business strategy. For example, industries dependent on raw materials such as oil, coal, and minerals are directly affected by resource availability. Moreover, governments and consumers increasingly demand eco-friendly products and processes. Businesses that adopt green technologies and corporate social responsibility gain goodwill and long-term sustainability. Thus, natural environment factors are crucial in modern business decisions.