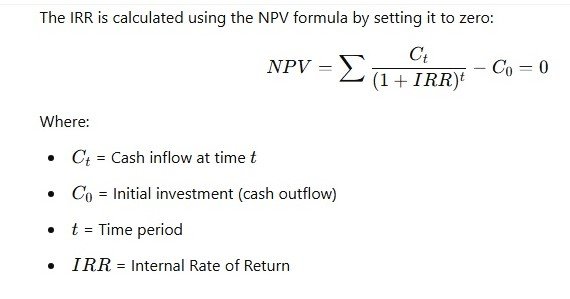

Capital Budgeting is the process of evaluating and selecting long-term investment projects that align with a company’s financial goals. It involves analyzing potential investments in fixed assets, such as new plants, machinery, or expansion projects, to determine their profitability and feasibility. Businesses use techniques like Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to assess investment decisions. Effective capital budgeting ensures optimal resource allocation, minimizes financial risks, and maximizes shareholder value. By carefully planning capital expenditures, organizations can achieve sustainable growth and maintain a competitive edge in the market.

Meaning of Capital Budgeting

Capital budgeting is the process of planning, evaluating, and selecting long-term investment projects that require large amounts of funds and yield benefits over several years. It involves decisions related to investment in fixed assets such as land, buildings, machinery, plant expansion, research and development, and new product lines.

Since capital investments involve huge costs, long gestation periods, and irreversible commitments, careful analysis is essential. Capital budgeting helps management assess the expected returns, risk, and feasibility of proposed projects. The main objective of capital budgeting is to maximize the wealth of shareholders by selecting projects that provide returns greater than the cost of capital while ensuring optimal utilization of financial resources.

Definitions of Capital Budgeting

1. R. C. Osborn

“Capital budgeting is the process of long-term planning for making and financing proposed capital outlays.”

2. Charles T. Horngren

“Capital budgeting is concerned with the allocation of firm’s scarce resources among available market opportunities.”

3. Weston and Brigham

“Capital budgeting is the process of analyzing potential additions to fixed assets which are expected to produce benefits over a period of time.”

4. Lynch

“Capital budgeting is the process of evaluating and selecting long-term investments consistent with the firm’s goal of maximizing owners’ wealth.”

5. Gitman

“Capital budgeting is the process of evaluating and selecting long-term investments that are consistent with the firm’s goal of maximizing shareholder value.”

Example of Capital Budgeting

A manufacturing company plans to expand its production facility by purchasing new machinery. The company evaluates the investment using Net Present Value (NPV) and Internal Rate of Return (IRR) to determine profitability. If the projected cash flows exceed the initial cost and meet the desired return rate, the expansion is approved. This decision helps increase production capacity, reduce costs per unit, and improve overall efficiency, ensuring long-term growth and competitiveness in the market.

A consumer goods company considers launching a new product line. The management conducts a capital budgeting analysis to assess development costs, market potential, and expected revenue. Using techniques like Payback Period and Profitability Index, the company determines if the project is financially viable. If the expected returns justify the investment, the new product is introduced. This decision helps diversify the company’s portfolio, capture new market segments, and boost overall revenue and brand recognition.

A company plans to install solar panels to reduce electricity costs and promote sustainability. The investment requires a significant upfront cost but offers long-term savings through reduced energy expenses. By applying NPV and IRR methods, the company evaluates whether the project’s future cash flows outweigh initial costs. If the return is positive, the investment is approved. This decision not only lowers operational expenses but also enhances the company’s corporate social responsibility (CSR) image and sustainability efforts.

A large retail chain considers acquiring a smaller competitor to expand its market presence. Before finalizing the acquisition, the company conducts a capital budgeting analysis, assessing the competitor’s financial health, potential synergies, and projected returns. Using methods like Discounted Cash Flow (DCF) and IRR, the company determines if the acquisition is a profitable investment. If the expected benefits outweigh costs, the deal is completed. This strategic move helps increase market share, enhance economies of scale, and improve overall profitability.

Objectives of Capital Budgeting

- Maximization of Shareholders’ Wealth

The primary objective of capital budgeting is to maximize shareholders’ wealth by selecting investment projects that generate returns higher than the firm’s cost of capital. Proper evaluation ensures that funds are invested in profitable projects, leading to increased earnings, higher dividends, and improved market value of shares. Sound capital budgeting decisions strengthen investor confidence and contribute to the long-term financial success of the organization.

- Efficient Allocation of Financial Resources

Capital budgeting ensures the effective and optimal utilization of limited financial resources by allocating funds to the most productive investment opportunities. Since capital is scarce, projects are evaluated and ranked based on expected returns, risk, and strategic importance. This prevents wastage of funds and ensures maximum benefit from investments, thereby improving operational efficiency and supporting sustainable business growth.

- Long-Term Growth and Expansion

Another important objective of capital budgeting is to promote long-term growth and expansion of the business. Investments in new machinery, plants, technology, and product development help firms increase production capacity and enter new markets. Capital budgeting ensures that such expansion plans are financially viable and strategically sound, enabling firms to maintain competitiveness and achieve steady growth over time.

- Minimization of Investment Risk

Capital budgeting helps minimize investment risk by systematically evaluating proposed projects using scientific techniques such as NPV, IRR, and risk analysis. It assesses future cash flows, uncertainty, and potential losses before committing large funds. By carefully analyzing risk-return relationships, management can avoid unprofitable or risky investments and ensure that projects contribute positively to the firm’s financial stability.

- Effective Planning and Control

Capital budgeting acts as a tool for effective financial planning and control. It helps management estimate future capital requirements, forecast cash flows, and plan investments efficiently. Once projects are approved, they serve as benchmarks for performance evaluation. Comparing actual results with expected outcomes allows management to exercise control, take corrective actions, and maintain financial discipline.

- Coordination Among Departments

Capital budgeting promotes coordination among various departments such as finance, production, marketing, and research. Investment decisions require collective inputs, ensuring that projects align with organizational goals. This coordination avoids duplication of efforts and conflicting priorities, ensuring smooth implementation of projects. It also helps integrate long-term strategic planning with day-to-day operational activities.

- Competitive Advantage and Technological Advancement

Capital budgeting enables firms to invest in advanced technology, automation, and innovation, helping them gain a competitive edge in the market. Evaluating such investments ensures adoption of cost-effective and efficient technologies. Technological advancements improve productivity, reduce costs, enhance product quality, and strengthen the firm’s ability to compete effectively in a dynamic business environment.

- Enhancement of Corporate Value and Reputation

Sound capital budgeting decisions enhance the overall value and reputation of the firm. Profitable investments improve financial performance, stability, and growth prospects. This builds confidence among investors, lenders, and other stakeholders. A firm known for prudent investment decisions enjoys easier access to capital, better market image, and long-term sustainability.

Significance of Capital Budgeting

- Facilitates Long-Term Investment Decisions

Capital budgeting plays a vital role in evaluating long-term investment decisions that involve heavy capital expenditure. Since such decisions affect the firm’s operations and profitability for many years, capital budgeting ensures careful assessment of costs, benefits, and risks. It helps management choose projects that support long-term objectives and avoid unprofitable or risky investments that may harm the firm’s financial position.

- Maximizes Profitability and Shareholders’ Wealth

One of the major significances of capital budgeting is the maximization of profitability and shareholders’ wealth. By selecting projects with higher returns than the cost of capital, the firm increases earnings and market value. Efficient capital budgeting leads to higher dividends, improved share prices, and enhanced investor confidence, contributing to the overall growth and stability of the organization.

- Ensures Optimal Utilization of Scarce Resources

Capital resources are limited, and capital budgeting ensures their optimal utilization. By evaluating and ranking projects based on profitability, risk, and strategic relevance, management can allocate funds to the most productive investments. This prevents wastage of financial resources and ensures that available capital is used efficiently to generate maximum benefits for the organization.

- Reduces Investment Risk and Uncertainty

Capital budgeting involves systematic analysis of future cash flows, uncertainties, and risks associated with investment projects. Techniques such as Net Present Value and Internal Rate of Return help in assessing project feasibility. This scientific approach reduces the chances of losses and enables management to make informed decisions, thereby minimizing the overall investment risk faced by the firm.

- Improves Financial Planning and Control

Capital budgeting contributes significantly to financial planning and control by estimating future capital requirements and expected cash flows. Once projects are approved, they serve as performance benchmarks. Comparing actual outcomes with planned results helps management exercise control, identify deviations, and take corrective measures, ensuring better financial discipline and efficiency.

- Supports Strategic and Expansion Decisions

Capital budgeting supports major strategic decisions such as expansion, diversification, modernization, and replacement of assets. It ensures that such decisions are aligned with the firm’s long-term objectives and financial capacity. Proper evaluation helps firms expand operations confidently while maintaining stability, competitiveness, and sustainable growth.

- Enhances Coordination Among Departments

Capital budgeting promotes coordination among various departments like finance, production, marketing, and research. Investment decisions require collective inputs, ensuring feasibility and alignment with organizational goals. This coordination avoids duplication of efforts, reduces conflicts, and ensures smooth execution of investment projects across the organization.

- Strengthens Market Image and Creditworthiness

Firms that follow systematic capital budgeting practices develop a reputation for sound financial management. This improves their market image and enhances creditworthiness. Investors and lenders view such firms as reliable and stable, making it easier to raise funds on favorable terms and ensuring long-term sustainability.

Features of Capital Budgeting

Capital budgeting focuses on long-term investment decisions that impact a company’s financial health for years. These investments include purchasing new machinery, expanding production facilities, or launching new products. Since these decisions require substantial capital, businesses must carefully analyze risks, returns, and cash flow projections. Poor investment choices can lead to financial losses, while well-planned investments enhance profitability and sustainability. Capital budgeting ensures that funds are allocated to projects that maximize shareholder value and align with the company’s strategic goals, making it a crucial aspect of financial planning and decision-making.

Capital budgeting decisions require significant financial resources due to the high costs associated with acquiring fixed assets, such as land, equipment, or technology upgrades. These expenditures are irreversible and cannot be recovered easily if the investment fails. Businesses must carefully evaluate each investment’s feasibility using techniques like Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period. Proper capital budgeting ensures that funds are not wasted on unprofitable ventures, helping the organization maintain financial stability and optimize its capital structure for long-term growth and sustainability.

Capital budgeting decisions involve long-term investments that, once made, are difficult to reverse without incurring significant losses. Fixed asset purchases, infrastructure development, or mergers and acquisitions require careful analysis, as selling or modifying these assets later can be costly and complex. Businesses must thoroughly evaluate risk factors, projected cash flows, and market conditions before committing to such investments. The irreversible nature of capital expenditures makes capital budgeting a critical process to ensure financial stability, strategic alignment, and efficient resource allocation for sustainable business operations and profitability.

Capital budgeting decisions are subject to high levels of risk and uncertainty due to changing market conditions, economic fluctuations, and technological advancements. Businesses must analyze factors such as inflation, interest rates, competition, and regulatory changes when evaluating investment projects. Techniques like sensitivity analysis and scenario analysis help assess potential risks and their impact on expected returns. Since capital investments are long-term commitments, predicting future cash flows accurately is challenging. Effective capital budgeting requires thorough research and risk management strategies to minimize uncertainties and enhance decision-making for sustainable financial growth.

Capital budgeting involves forecasting and analyzing future cash flows from an investment to determine its feasibility. Since these investments typically yield returns over several years, accurate estimation of cash inflows and outflows is crucial. Businesses use financial models like Discounted Cash Flow (DCF) analysis, Net Present Value (NPV), and Internal Rate of Return (IRR) to assess profitability. Errors in cash flow projections can lead to poor investment decisions. By thoroughly evaluating expected revenues, operating costs, and potential risks, companies can make informed choices that maximize financial returns and ensure long-term success.

Capital budgeting aims to invest in projects that enhance business profitability and long-term growth. Companies analyze investment options to ensure they generate positive returns, improve efficiency, and strengthen market position. Choosing the right projects leads to increased production capacity, cost savings, and competitive advantage. Methods like Payback Period, Profitability Index, and IRR help assess the financial viability of projects. A well-executed capital budgeting process ensures optimal utilization of funds, balancing risks and rewards to maximize shareholder wealth while achieving sustainable development and financial stability in an ever-changing business environment.

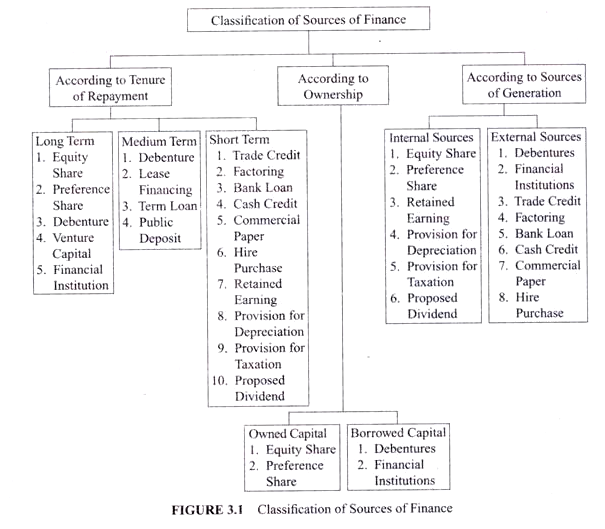

Need of Capital Budgeting

- Large Investment Requirement

Capital budgeting is needed because investment in fixed assets such as land, machinery, buildings, and technology requires huge capital outlay. Such investments cannot be reversed easily once made. Therefore, careful evaluation is essential to ensure that funds are invested in projects that yield long-term benefits and do not create financial burden for the organization.

- Long-Term Commitment of Funds

Capital expenditure decisions involve long-term commitment of funds, often for many years. Since capital once invested remains locked for a long period, improper decisions can adversely affect liquidity and profitability. Capital budgeting ensures that long-term funds are invested wisely and generate adequate returns over the life of the project.

- Limited Availability of Financial Resources

Financial resources are always scarce and must be used judiciously. Capital budgeting helps management prioritize investment projects and allocate limited funds to the most profitable opportunities. This ensures optimum utilization of capital and avoids wastage of resources on low-return or risky projects.

- High Degree of Risk and Uncertainty

Future cash flows from capital investments are uncertain and subject to risks such as market changes, technological obsolescence, and economic fluctuations. Capital budgeting techniques help evaluate risk and uncertainty by estimating future returns and analyzing feasibility. This reduces chances of financial losses and improves decision quality.

- Impact on Profitability and Growth

Capital budgeting decisions have a direct impact on the firm’s profitability and growth. Investment in the right projects improves production capacity, efficiency, and market competitiveness. Wrong decisions can lead to poor performance and financial distress. Hence, capital budgeting is essential to ensure sustainable growth and profitability.

- Irreversibility of Investment Decisions

Most capital investments are irreversible or difficult to reverse without heavy losses. Once machinery or plant is installed, it cannot be easily sold or converted into cash. Capital budgeting ensures thorough evaluation before committing funds, reducing the risk of irreversible losses.

Capital budgeting is needed to support strategic decisions such as expansion, modernization, diversification, and replacement of assets. These decisions determine the long-term direction of the firm. Proper capital budgeting ensures alignment between investment decisions and organizational objectives.

- Improved Financial Planning and Control

Capital budgeting aids in effective financial planning by forecasting capital needs and expected returns. It also helps in performance evaluation by comparing actual results with planned estimates. This improves control, accountability, and financial discipline within the organization.

Importance of Capital Budgeting

- Ensures Sound Investment Decisions

Capital budgeting is important because it helps management take sound and rational investment decisions. Since capital investments involve large funds and long-term commitment, careful evaluation is essential. Capital budgeting techniques analyze costs, returns, and risks to ensure that only financially viable projects are selected, thereby avoiding costly mistakes.

- Maximizes Shareholders’ Wealth

One of the key importance of capital budgeting lies in its ability to maximize shareholders’ wealth. By selecting projects that yield returns higher than the cost of capital, the firm enhances profitability and market value. Efficient capital budgeting leads to higher dividends and appreciation in share prices, increasing investors’ confidence in the company.

- Optimal Utilization of Financial Resources

Capital budgeting ensures effective utilization of limited financial resources. It helps management prioritize projects and allocate funds to investments that offer the highest returns. This avoids wastage of funds and ensures that scarce capital is invested in the most productive and profitable opportunities.

- Supports Long-Term Growth and Expansion

Capital budgeting plays a vital role in supporting long-term growth and expansion plans of a firm. Investments in new machinery, technology, and infrastructure help increase production capacity and market reach. Proper evaluation ensures that expansion projects are financially feasible and contribute to sustainable growth.

- Reduces Risk and Uncertainty

Future returns from capital investments are uncertain. Capital budgeting helps reduce risk by using scientific techniques such as NPV and IRR to assess project feasibility. This systematic analysis minimizes the chances of losses and helps management make informed decisions under uncertainty.

- Improves Financial Planning and Control

Capital budgeting is essential for effective financial planning and control. It helps forecast future capital requirements and expected cash flows. Approved projects serve as benchmarks for performance evaluation, enabling management to compare actual results with planned outcomes and take corrective actions when necessary.

- Enhances Coordination Among Departments

Capital budgeting encourages coordination among various departments such as finance, production, marketing, and research. Investment decisions require inputs from all functional areas, ensuring that projects align with organizational goals. This improves efficiency and smooth execution of investment plans.

- Strengthens Market Image and Creditworthiness

A firm that follows systematic capital budgeting practices gains a strong market image and improved creditworthiness. Investors and lenders view such firms as financially disciplined and stable. This makes it easier to raise funds at favorable terms and supports long-term sustainability.

Process of Capital Budgeting

The extent to which the capital budgeting process needs to be formalized and systematic procedures established depends on the size of the organization, number of projects to be considered, direct financial benefit of each project considered by itself, the composition of the firm’s existing assets and management’s desire to change that composition, timing of expenditures associated with the that are finally accepted.

Step 1. Planning

The capital budgeting process begins with the identification of potential investment opportunities. The opportunity then enters the planning phase when the potential effect on the firm’s fortunes is assessed and the ability of the management of the firm to exploit the opportunity is determined. Opportunities having little merit are rejected and promising opportunities are advanced in the form of a proposal to enter the evaluation phase.

Step 2. Evaluation

This phase involves the determination of proposal and its investments, inflows and outflows. Investment appraisal techniques, ranging from the simple pay back method and accounting rate of return to the more sophisticated discounted cash flow techniques, are used to appraise the proposals. The technique selected should be the one that enables the manager to make the best decision in the light of prevailing circumstances.

Step 3. Selection

Considering the returns and risk associated with the individual project as well as the cost of capital to the organization, the organization will choose among projects so as to maximize shareholders wealth.

Step 4. Implementation

When the final selection has been made, the firm must acquire the necessary funds, purchase the assets, and begin the implementation of the project.

Step 5. Control

The progress of the project is monitored with the aid of feedback reports. These reports will include capital expenditure progress reports, performance reports comparing actual performance against plans set and post completion audits.

Step 6. Review

When a project terminates, or even before, the organization should review the entire project to explain its success or failure. This phase may have implication for forms planning and evaluation procedures. Further, the review may produce ideas for new proposal to be undertaken in the future.

by

by