International monetary system refers to a system that forms rules and standards for facilitating international trade among the nations.

It helps in reallocating the capital and investment from one nation to another.

It is the global network of the government and financial institutions that determine the exchange rate of different currencies for international trade. It is a governing body that sets rules and regulations by which different nations exchange currencies with each other.

With the growing complexity in the international trade and financial market, the international monetary system is necessary to assign a standard value of the international currencies. The rules and regulations set by the international monetary system to regulate and control the exchange value of the currencies are agreed upon by the respective governments of the nations. Thus, the government’s stand may affect the decision making of the international monetary system. For example, change in the trade policy of a government may affect the international trade of goods and services.

International monetary system motivates and encourages the nations to participate in the international trade to improve their BOP and minimize the trade deficit. It has grown over the years as a single architectural body with a vision to integrate the global economy. Some of the important achievements of the international monetary system over the years have been the establishment of World Bank and International Monetary Fund in the year 1944.

The establishment of IMF and World Bank is the result of the agreement among nations to set a body, which promotes and supports the international trade. Now, let’s discuss the evolution of international monetary system. Earlier in 1870 to 1914, trade was carried with the help of gold and silver without any institutional support. At that time, monetary system was decentralized and market based and money played a minor role as compared to gold in international trade.

The use of gold declined after World War I as war increased expenditure and inflation. In such a scenario, countries planned to revive the standard of gold but failed due to great depression. Thus, in 1944, 730 representatives of 44 nations met at Bretton Woods, New Hampshire, United States to create a new international monetary system.

This was called as the Bretton Woods system, which became a turning point in the history of international trade. The aim of new international monetary system is to create a stabilized international currency system and ensure a monetary stability for all the nations.

It was decided that since the United States held most of the world’s gold, thus all the nations would determine the values of their currencies in terms of dollar. The central banks of nations were given the task of maintaining fixed exchange rates with respect to dollar for each currency.

The Bretton Woods system ended in 1971 as the trade deficit and growing inflation undermined the value of dollar in the whole world. In 1973, the floating exchange rate system, also known as flexible exchange rate system was developed that was market based.

Paper Currency Standard & Purchasing Power Parity

With the breakdown of the gold standard during the period of the First World War, gold parities and free movements of gold ceased, therefore the mint par of exchange lost significance in the exchange markets.

Exchange rates fluctuated far beyond the traditional gold points and there was complete confusion. Hence, to explain this phenomenon and the problem of determination of the equilibrium exchange between inconvertible currencies, the theory of purchasing power parity was enunciated.

The basic idea underlying the purchasing power parity theory is that the foreign currencies are demanded by the nationals of a country because it has power to command goods in its own country.

When domestic currency of a nation is exchanged for foreign currency, what is in fact done is that domestic purchasing power is exchanged for foreign purchasing power. It follows that the main factor determining the exchange rate is the relative purchasing power of the two currencies.

For, when two currencies are exchanged, what is exchanged, in fact, is the internal purchasing power of the two currencies.

Thus, the equilibrium rate of exchange should be such that the exchange of currencies would involve the exchange of the equal amounts of purchasing power. It is the parity of the purchasing power that determines the exchange rate. Thus, the purchasing power theory states that exchange rate tends to rest at the point at which there is equality between the respective purchasing power of the currencies. In other words, rate of exchange between two inconvertible paper currencies tends to close to their purchasing power ratio. Hence,

The Purchasing Power Theory

(PPT) seeks to explain that under the system of autonomous paper standard the external value of a currency depends ultimately and essentially on the domestic purchasing power of that currency relative to that of another currency.

The PPT has been presented in two versions, namely

- Absolute Version of Purchasing Power Parity and

- Relative Version of Purchasing Power Parity.

-

Absolute Purchasing Power Parity

The absolute version of the purchasing power parity theory stresses that the exchange rates should normally reflect the relation between the internal purchasing power of the various national currency units.

The price of a tradable commodity in one country should theoretically be equal to the price of the same commodity in another country, after adjusting for the foreign exchange rate. The theory is known as the international law of one price. When the international law one price applied to the representative good or basket of goods, it is called the absolute purchasing power parity condition.

To illustrate the point, let us assume that a representative collection of goods costs Rs.9,625/- in India and US$ 195 in USA. As per the Absolute PPP theory, the exchange rate between US$ and Indian Rupee is the ratio of two price indices.

Spot price (In Indian Rupee) = Price Index of India/ Price Index of USA

Spot Rate = PRupee / PUSA

As per the example mentioned above, the exchange rate would be;

Spot (in Rupee) = 9625/195 = Rs.47.5128

The theoretical argument behind the Absolute PPP condition is that a country’s goods are relatively cheap internationally; goods market arbitrage would create pressure on both foreign prices and goods prices to correct, and thereby conform to uniform international prices.

-

Relative Purchasing Power Parity

Purchasing Power for two currencies can be different not because of differences in their internal purchasing power, but some other factors also.

Relative purchasing power parity relates the change in two countries’ expected inflation rates to the change in their exchange rates. Inflation reduces the real purchasing power of a nation’s currency.

If a country has an annual inflation rate of 5%, that country’s currency will be able to purchase 5% less real goods at the end of one year. Relative purchasing power parity examines the relative changes in price levels between two countries and maintains the exchange rates, which will compensate for inflation differentials between the two countries.

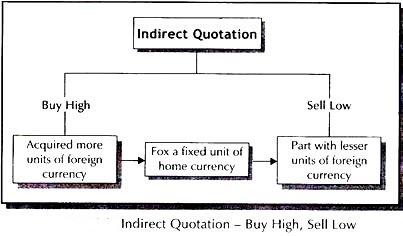

The relationship can be expressed as follows, using indirect quotes:

St / S0 = (1 + iy) ÷ (1 + ix) t

Where,

S0 is the spot exchange rate at the beginning of the time period (measured as the “y” country price of one unit of currency x)

St is the spot exchange rate at the end of the time period.

iy is the expected annualized inflation rate for country y, which is considered to be the foreign country.

Ix is the expected annualized inflation rate for country x, which is considered to be the domestic country.

Example

The annual inflation rate is expected to be 8% in the India and that for the US is 3%. The current exchange rate is Rs.46.5500/- per US $. What would the expected spot exchange rate be in six months for Indian Rupee relative to US$.

Answer:

So the relevant equation is:

St / S0 = (1 + iy) ÷ (1 + ix)

= S6month ÷ Rs.46.5500 = (1.08 ÷ 1.03)0.5

Which implies S6month = (1.023984) × Rs.46.550 = Rs.47.6665.

So the expected spot exchange rate at the end of six months would be Rs.47.6665 per US$.

Inflation, taxes, quality of products, and other circumstances that change the market also have bearing on the price or internal purchasing power. All these factors need to be adjusted while estimating the exchange rate under in-convertible paper currency standard. PPP theory may not reflect the true exchange rate in the short-run however; it actually indicates the fundamental equilibrium exchange rate in the long-run.

International Monetary System: The Bretton Woods System

Attempts were initiated to revive the Gold Standard after the World War I, but it collapsed entirely during the Great Depression of the 1930s.

It was felt that adherence to the Gold Standard prevented countries from expanding the money supply significantly so as to revive economic activity.

However, after the Second World War, representatives of most of the world’s leading nations met at Bretton Woods, New Hampshire, in 1944 to create a new international monetary system.

United States of America, at that time, was accounted for over half of the world’s manufacturing capacity and held most of the world’s gold, the leaders decided to tie world currencies to the US dollar, which, in turn, they agreed should be convertible into gold at $35 per ounce. Under the Bretton Woods system, Central Banks of participating countries were given the task of maintaining fixed exchange rates between their currencies and the US-dollar.

They did this by intervening in foreign exchange markets. If a country’s currency was too high relative to the US-dollar, its central bank would sell its currency in exchange for US-dollars, driving down the value of its currency. Conversely, if the value of a country’s money was too low, the country would buy its own currency, thereby driving up the price. The purpose of the Bretton Woods meeting was to set up new system of rules, regulations, and procedures for the major economies of the world.

The principal goal of the agreement was economic stability for the major economic powers of the world. The system was designed to address systemic imbalances without upsetting the system as a whole.

The Bretton Woods System continued until 1971. By that time, high inflation and trade deficit in the USA were undermining the value of the dollar. Americans urged Germany and Japan, both of which had favorable payments balances, to appreciate their currencies.

But those nations were reluctant to take that step, since raising the value of their currencies would increase prices for their goods and hurt their exports. Finally, the USA abandoned the fixed value of the US-dollar and allowed it to “float” against other currencies, which led to collapse of the Bretton Woods System.

The Bretton Woods system established the US Dollar as the reserve currency of the world. It also required world currencies to be pegged to the US-dollar rather than gold. The demise of Bretton woods started in 1971 when Richard Nixon took the US off of the Gold Standard to stem the outflow of gold. By 1976 the principles of Bretton Woods were abandoned all together and the world currencies were once again free floating.

World leaders tried to revive the system with the so-called “Smithsonian Agreement” in

1971, but the effort could not yield. Economists call the resulting system a “managed float regime,” meaning that even though exchange rates most currencies float, central Banks till intervene to prevent sharp changes.

As in 1971, countries with large trade surpluses often sell their own currencies in an effort to prevent them from appreciating. Similarly, countries with large trade deficits buy their own currencies in order to prevent depreciation, which raises domestic prices. But there are limits to what can be accomplished through intervention, especially for countries with large trade deficits. Eventually, a country that intervenes to support its currency may deplete its international reserves, making it unable to continue support the currency and potentially leaving it unable to meet its international obligations.

At present almost all countries having their own paper currencies standard which is neither linked to gold or US-dollar or any other foreign currencies and they have adopted the currency system which is “managed floating” in nature.

The Mint Par Parity Theory

This theory is associated with the working of the international gold standard. Under this system, the currency in use was made of gold or was convertible into gold at a fixed rate. The value of the currency unit was defined in terms of certain weight of gold, that is, so many grains of gold to the rupee, the dollar, the pound, etc. The central bank of the country was always ready to buy and sell gold at the specified price.

The rate at which the standard money of the country was convertible into gold was called the mint price of gold.

If the official British price of gold was £6 per ounce and of the US price of gold $12 per ounce, they were the mint prices of gold in the respective countries. The exchange rate between dollar and pound would be fixed at $12/£6 =2, which in other words, one pound is equal to two dollar.

This rate is called mint parity rate or mint par of exchange because it was based on the mint price of gold. However, the actual exchange rate between these currencies would vary above or below the mint parity rate by the cost of shipping gold between two countries. To illustrate this, suppose the US has a deficit in its balance of payments with Britain. The difference between the value of imports and exports will have to be paid in gold by the US importers because the demand for pounds exceeds the supply of pounds. But the transshipment of gold involves cost. Suppose the shipping cost of gold from the US to Britain is 5 cents. So the US importers would have to pay $2.05 per £1. This is exchange rate, which is equivalent to US gold

Because currencies were convertible in gold, then nations could ship gold among themselves to adjust their “balance of payments.”

In theory, all nations should have an optimal balance of payments of zero, i.e. they should not have either a trade deficit or trade surplus.

For example, in a bilateral trade relationship between Australia and Brazil, if Brazil had a trade deficit with Australia, then Brazil could pay Australia gold. Now that Australia had more gold, it could issue more paper money since it now had a greater supply of gold to support new bills.

With an increase of paper bills in the Australian economy, inflation, i.e. a rise in prices due to an overabundance of money, would occur. The rise in prices would subsequently lead to a drop in exports, because Brazil would not want to buy the more expensive Australian goods.

Subsequently, Australia would then return to a zero balance of payments because its trade surplus would disappear.

Likewise, when gold leaves Brazil, the price of its goods should decline, making them more attractive for Australia. As a result, Brazil would experience an increase in exports until its balance of payments reached zero. Therefore, the gold standard would ideally create a natural balancing effect to stabilize the money supply of participating nations.

The Gold Standard in Operation

However, the operation of the gold standard in reality caused many problems. When gold left a nation, the ideal balancing effect would not occur immediately. Instead, recessions and unemployment would often occur. This was because nations with a balance of payments deficit often neglected to take appropriate measures to stimulate economic growth. Instead of altering tax rates or increasing expenditures – measures which should stimulate growth – governments opted to not interfere with their nations’ economies. Thus, trade deficits would persist, resulting in chronic recessions and unemployment.

With the outbreak of the First World War in 1914, the international trading system broke down and nations valued their currencies by fiat instead, i.e. governments took their currencies off the gold standard and simply dictated the value of their money. Following the war, some nations attempted to reinstate the gold standard at pre-war rates, but drastic changes in the global economy made such attempts futile. Britain, which had previously been the world’s financial leader, reinstated the pound at its pre-war gold value, but because its economy was much weaker, the pound was overvalued by approximately 10%. Consequently, gold swept out of Britain, and the public was left with valueless notes, creating a surge in unemployment. By the time of the Second World War, the inherent problems of the gold standard became apparent to governments and economists alike.

Following the second world war, the International Monetary Fund replaced the gold standard as a means for nations to address balance of payments problems with what became a “gold-exchange” standard.

Currencies would be exchangeable not in gold but in the predominant post-war currencies of the allied nations: British sterling, or more importantly, the U.S. dollar. Under the new International Monetary Fund approach, governments had a more pronounced role in managing their economies. Ideally, governments would hold dollars in “reserve.” If an economy needed an influx of money because of a balance of payments deficit, the government could exchange its reserve dollars for its own currency, and then inject this money into its economy. The dollar would ideally remain stable since the U.S. government agreed to exchange dollars for gold at a price of $35 an ounce. Thus, world currencies were officially off the gold standard. However, they were exchangeable for dollars. Because dollars were still exchangeable for gold, the “gold-exchange” standard became the prevailing monetary exchange system for many years.

The effect of the gold-exchange system was to make the United States the center for international currency exchange. However, due to the inflationary effects of the Vietnam War and the resurgence of other economies, the United States could no longer comply with its obligation to exchange dollars for gold. Its own gold supply was rapidly declining. In 1971,

President Richard Nixon removed the dollar from gold, ending the predominance of gold in the international monetary system.

In retrospect, the gold standard had many weaknesses. Its foremost problem was that its theoretical balancing effect rarely worked in reality. A much more efficient means to resolve balance of payments problems is through government intervention in their economies and the exchange of reserve currencies. Today, very few commentators propose a return to the gold standard.

by

by