Cost is the monetary value of resources sacrificed or consumed for achieving a particular objective. Every business organization incurs various types of costs while producing goods, rendering services, managing operations, and achieving organizational goals. For effective planning, control, decision-making, and performance evaluation, it is essential to classify costs into meaningful categories. Cost classification is the process of grouping costs according to their common characteristics. Different classifications are used for different managerial purposes. Proper classification helps management understand cost behavior, determine product costs, prepare budgets, control expenses, evaluate efficiency, and formulate business strategies. Since a single cost may belong to more than one category, costs are classified from different viewpoints. The classification of costs is therefore one of the most important foundations of Cost Management and Cost Accounting.

1. Classification According to Nature or Elements of Cost

Under this classification, costs are grouped according to the basic elements involved in the production process. This is one of the simplest and most widely used methods of cost classification.

(a) Material Cost

Material cost refers to the cost of physical substances used in manufacturing a product. It includes raw materials, components, spare parts, consumables, and supplies required for production. Materials may be direct or indirect. Direct materials become a part of the finished product and can be directly identified with a specific unit of output. Indirect materials are used in the production process but cannot be directly traced to a particular product. Material cost often forms a significant portion of total production cost. Effective material cost control helps reduce wastage, improve efficiency, and increase profitability. Techniques such as inventory control, material budgeting, and standard costing are commonly used to manage material costs effectively.

(b) Labour Cost

Labour cost refers to the remuneration paid to employees for their services. It includes wages, salaries, bonuses, incentives, allowances, and other employee benefits. Labour may be direct or indirect. Direct labour is directly involved in the manufacturing process and can be identified with specific products. Indirect labour supports production activities but cannot be directly traced to individual products. Labour cost plays a critical role in determining total production cost and operational efficiency. Effective labour management improves productivity and reduces unnecessary expenditure. Organizations use various techniques such as time studies, performance evaluation, and labour budgeting to control labour costs and improve workforce utilization.

(c) Expenses

Expenses include all costs other than material and labour costs incurred during business operations. These may include rent, insurance, depreciation, power, maintenance, legal charges, and administrative expenses. Expenses may be direct or indirect depending on their relationship with production activities. Proper control of expenses is necessary to ensure profitability and efficient resource utilization. Businesses regularly monitor expenses to identify unnecessary costs and improve operational performance. Expenses form an important component of total cost and significantly influence organizational profitability.

2. Classification According to Function

Costs may be classified according to the functions or activities for which they are incurred.

(a) Production Cost

Production cost refers to the total cost incurred in manufacturing goods. It includes direct material cost, direct labour cost, and manufacturing overheads. Production costs are directly associated with the conversion of raw materials into finished products. Accurate determination of production cost is important for pricing, inventory valuation, and profitability analysis. Managers use production cost information to control manufacturing expenses and improve operational efficiency. Reducing production costs without compromising quality helps organizations gain a competitive advantage. Therefore, production cost is a crucial classification that supports cost control and effective decision-making in manufacturing organizations.

(b) Administration Cost

Administration cost consists of expenses incurred for planning, directing, coordinating, and controlling organizational activities. Examples include office salaries, office rent, legal expenses, audit fees, and administrative supplies. These costs are necessary for managing business operations but are not directly related to production or selling activities. Effective control of administration costs helps improve organizational efficiency and profitability. Management continuously evaluates administrative expenditures to eliminate unnecessary costs and enhance productivity. Administration costs support the smooth functioning of the organization and contribute to achieving business objectives through proper planning and control of resources.=

(c) Selling Cost

Selling cost refers to expenses incurred for promoting and selling products or services. Examples include advertising expenses, sales commissions, promotional campaigns, sales staff salaries, and market research costs. These costs are aimed at increasing sales volume and attracting customers. Selling costs play a vital role in maintaining competitiveness and expanding market share. Proper management of selling costs ensures that marketing activities generate sufficient returns on investment. Organizations continuously monitor selling expenses to evaluate the effectiveness of promotional efforts. Therefore, selling costs are an important classification that helps management assess marketing efficiency and profitability.

(d) Distribution Cost

Distribution cost includes expenses incurred in delivering products from the manufacturer to customers. Examples include transportation charges, warehousing costs, packing expenses, loading and unloading charges, and delivery expenses. These costs ensure that products reach customers efficiently and on time. Effective control of distribution costs improves customer satisfaction and reduces overall operating expenses. Organizations seek to optimize logistics and supply chain operations to minimize distribution costs. Proper management of these costs enhances competitiveness and profitability. Distribution costs are therefore an important component of total cost and a significant area of managerial attention.

(e) Research and Development Cost

Research and development cost refers to expenditure incurred on developing new products, improving existing products, and discovering innovative production methods. These costs support technological advancement and long-term business growth. Examples include laboratory expenses, research staff salaries, testing costs, and prototype development expenses. Although research and development costs may not generate immediate benefits, they contribute significantly to future profitability and competitiveness. Organizations invest in research and development to meet changing customer needs and adapt to market trends. Effective management of these costs helps businesses maintain innovation and achieve sustainable growth.

3. Classification According to Identifiability

This classification is based on the ability to identify costs with a specific product, department, process, or activity.

(a) Direct Cost

Direct costs are costs that can be directly identified and assigned to a specific product, service, department, or activity. Examples include direct materials, direct labour, and direct expenses. These costs form an integral part of product costing and are easily traceable. Accurate identification of direct costs is essential for determining product profitability and pricing decisions. Since direct costs are directly associated with production, they can be measured and controlled effectively. Proper management of direct costs helps improve efficiency and reduce unnecessary expenditures. Therefore, direct costs play a significant role in cost determination and management.

(b) Indirect Cost

Indirect costs are costs that cannot be directly traced to a particular product, service, or activity. Examples include factory rent, electricity, supervision costs, and maintenance expenses. These costs benefit multiple products or departments and are allocated using appropriate methods. Indirect costs are also known as overheads. Effective allocation and control of indirect costs are important for accurate cost determination and profitability analysis. Managers regularly monitor overhead expenses to improve efficiency and reduce wastage. Indirect costs support business operations and must be managed carefully to ensure organizational profitability and cost effectiveness.

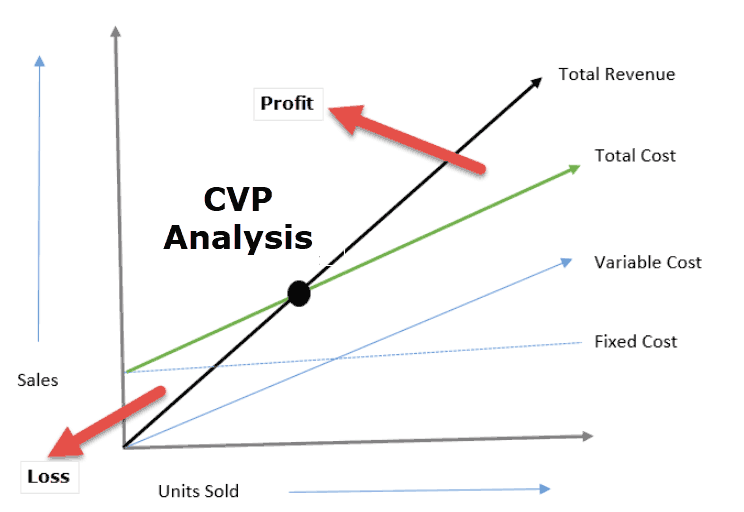

4. Classification According to Behavior

Cost behavior refers to how costs respond to changes in production volume or activity level.

(a) Fixed Cost

Fixed cost refers to costs that remain constant irrespective of changes in production volume or business activity within a relevant range. These costs do not fluctuate with the number of units produced and must be incurred even when production is zero. Examples include factory rent, insurance premiums, property taxes, and salaries of permanent employees. Fixed costs provide stability in business operations but can affect profitability if production levels decline significantly. Managers analyze fixed costs to determine break-even points and profit potential. Effective management of fixed costs helps organizations maintain financial stability and improve long-term planning and resource allocation.

(b) Variable Cost

Variable cost refers to costs that change directly in proportion to the level of production or business activity. As output increases, variable costs increase, and as output decreases, they decrease accordingly. Examples include raw materials, direct labour paid on a piece-rate basis, packaging costs, and sales commissions. Variable costs are important in pricing decisions, cost-volume-profit analysis, and production planning. Understanding variable cost behavior helps managers estimate future expenses and make informed decisions. Efficient control of variable costs contributes to higher profitability and improved operational efficiency, making this classification highly relevant in cost management.

(c) Semi-Variable Cost

Semi-variable costs, also known as mixed costs, contain both fixed and variable components. A portion of the cost remains constant regardless of activity levels, while another portion varies according to usage or output. Examples include electricity bills, telephone expenses, and maintenance costs. Businesses pay a fixed charge plus additional charges based on consumption. Understanding semi-variable costs is important because they do not behave entirely as fixed or variable costs. Managers often separate the fixed and variable portions for budgeting and forecasting purposes. Proper analysis of semi-variable costs improves planning accuracy and supports effective cost control measures.

(d) Step Cost

Step cost refers to costs that remain fixed within a specific range of activity but increase suddenly when activity exceeds that range. These costs rise in steps rather than gradually. Examples include hiring additional supervisors, purchasing extra equipment, or expanding warehouse capacity. Step costs are important in capacity planning and resource allocation. Managers must anticipate increases in activity levels and plan accordingly to avoid operational disruptions. Understanding step costs helps organizations determine the most efficient production levels and avoid unnecessary expenditure. This classification supports strategic planning and efficient utilization of organizational resources.

5. Classification According to Controllability

Costs may be classified according to the degree of control exercised by management.

(a) Controllable Cost

Controllable costs are costs that can be influenced or regulated by a manager within a specific period. Examples include material consumption, overtime wages, maintenance expenses, and utility usage. Managers are held accountable for these costs because they have authority to control them. Effective management of controllable costs improves efficiency, reduces wastage, and enhances profitability. Organizations often use budgetary control and performance evaluation systems to monitor controllable costs. By identifying areas where expenses can be reduced, managers can contribute significantly to organizational success. Controllable costs therefore play a vital role in responsibility accounting and performance management.

(b) Uncontrollable Cost

Uncontrollable costs are costs that cannot be influenced by a particular manager within a given period. Examples include allocated corporate overheads, government taxes, insurance premiums determined by external factors, and depreciation charges. Since managers have little or no authority over these costs, they are generally excluded from performance evaluations. Understanding uncontrollable costs helps ensure fair assessment of managerial performance. Although these costs cannot be directly controlled, organizations still monitor them to understand their impact on profitability. Proper classification of uncontrollable costs supports effective responsibility accounting and realistic performance measurement systems.

6. Classification According to Normality

This classification distinguishes costs based on whether they occur under normal or abnormal circumstances.

(a) Normal Cost

Normal costs are costs incurred under ordinary and expected operating conditions. These costs arise regularly during the normal course of business activities and are considered part of standard production processes. Examples include normal material wastage, routine maintenance expenses, and standard labour costs. Normal costs are included in product cost calculations and are anticipated during budgeting and planning. Effective management of normal costs helps maintain operational efficiency and profitability. Organizations establish standards and benchmarks for normal costs to monitor performance and identify deviations. Understanding normal costs is essential for accurate cost determination and financial planning.

(b) Abnormal Cost

Abnormal costs arise due to unusual events, inefficiencies, or unforeseen circumstances that are not part of normal business operations. Examples include losses caused by fire, theft, strikes, accidents, machine breakdowns, floods, and natural disasters. These costs are generally excluded from product costs because they do not represent normal operating conditions. Instead, they are treated separately in financial statements. Proper identification of abnormal costs helps management evaluate exceptional situations and take corrective action. Analyzing abnormal costs also assists in risk management and improving internal controls. This classification ensures more accurate cost measurement and performance evaluation.

7. Classification According to Time

Costs can also be classified according to the time period involved.

(a) Historical Cost

Historical cost refers to the actual cost incurred in the past and recorded in accounting records. It represents the amount paid for acquiring assets, materials, labour, or services at the time of the transaction. Historical costs provide valuable information about past performance and serve as a basis for financial reporting and analysis. Managers use historical cost data to compare current performance with previous periods and identify trends. Although historical costs are useful for evaluation, they may not reflect current market conditions. Nevertheless, they remain an important source of information for budgeting, forecasting, and decision-making.

(b) Predetermined Cost

Predetermined cost refers to the estimated cost calculated before actual production or business activities begin. Examples include standard costs and budgeted costs. These costs are based on expected conditions, historical data, and future projections. Predetermined costs help organizations plan operations, prepare budgets, and establish performance standards. Managers compare actual costs with predetermined costs to identify variances and take corrective actions. This classification supports effective cost control and performance evaluation. By anticipating future expenses, organizations can allocate resources efficiently and minimize financial risks. Predetermined costs are therefore essential tools in modern cost management systems.

8. Classification According to Association with Products

This classification distinguishes costs according to their relationship with products.

(a) Product Cost

Product costs are costs directly associated with manufacturing goods or providing services. They include direct materials, direct labour, and manufacturing overheads. Product costs are assigned to inventory and become expenses only when the products are sold. Accurate determination of product costs is essential for pricing decisions, profitability analysis, and inventory valuation. Managers use product cost information to evaluate production efficiency and identify opportunities for cost reduction. Proper classification of product costs ensures compliance with accounting standards and supports effective business decision-making. Product costs are fundamental to cost accounting and manufacturing management.

(b) Period Cost

Period costs are costs that are charged against revenue in the accounting period in which they are incurred. They are not directly associated with manufacturing products and therefore are not included in inventory valuation. Examples include administrative expenses, selling expenses, office rent, and marketing costs. Period costs help support business operations and generate revenue during a specific period. Proper management of period costs is important for maintaining profitability and controlling overhead expenses. Managers regularly review these costs to identify inefficiencies and improve financial performance. Understanding period costs is essential for accurate income measurement and financial reporting.

9. Classification According to Decision-Making

Managers frequently classify costs according to their usefulness in decision-making.

(a) Relevant Cost

Relevant costs are costs that influence a particular managerial decision and vary among alternatives. Only costs that change as a result of selecting one option over another are considered relevant. Examples include additional production costs, incremental costs, and opportunity costs. Relevant costs are important in decisions such as pricing, outsourcing, product selection, and investment analysis. Managers focus on relevant costs because they directly affect future outcomes. Proper identification of relevant costs improves decision quality and reduces the risk of errors. This classification plays a crucial role in managerial accounting and strategic planning.

(b) Irrelevant Cost

Irrelevant costs are costs that do not affect a particular decision because they remain unchanged regardless of the alternative selected. Examples include sunk costs and certain fixed costs that cannot be altered in the short term. Since irrelevant costs have no impact on future outcomes, managers should exclude them from decision-making processes. Failure to distinguish irrelevant costs may result in poor business decisions. Understanding this classification helps management focus only on meaningful information and improve analytical accuracy. Irrelevant costs are therefore important in cost analysis because they help simplify and strengthen managerial decision-making.

(c) Opportunity Cost

Opportunity cost represents the value of the next best alternative sacrificed when one course of action is chosen over another. Although it does not involve actual cash expenditure, it is highly relevant in decision-making. For example, using a building for production may involve sacrificing rental income that could have been earned from leasing it. Opportunity cost helps managers evaluate alternative uses of resources and select the most beneficial option. Considering opportunity costs leads to more rational and profitable decisions. This classification is particularly important in strategic planning, investment analysis, and resource allocation decisions.

(d) Sunk Cost

Sunk cost refers to a cost that has already been incurred and cannot be recovered regardless of future actions. Examples include research expenses already spent, obsolete inventory costs, and non-refundable deposits. Since sunk costs cannot be changed, they should not influence future decisions. However, managers often mistakenly consider sunk costs when evaluating alternatives. Proper understanding of sunk costs helps avoid biased decision-making and promotes rational analysis. This classification is essential in managerial accounting because it encourages decision-makers to focus on future costs and benefits rather than past expenditures.

(e) Differential Cost

Differential cost is the difference in total cost between two or more alternatives. It represents the additional or reduced cost resulting from selecting one option over another. Differential cost analysis helps managers compare alternatives and identify the most profitable choice. Examples include comparing the cost of manufacturing a product internally versus purchasing it from an external supplier. Differential costs are particularly useful in make-or-buy decisions, product mix decisions, and expansion planning. By focusing on cost differences, managers can make informed choices that maximize profitability and improve resource utilization.

(f) Incremental Cost

Incremental cost refers to the additional cost incurred when business activity, production volume, or service levels increase. It is closely related to differential cost and focuses specifically on cost increases resulting from expansion. Examples include the cost of producing additional units, hiring extra workers, or purchasing more materials. Incremental cost analysis helps managers evaluate the financial consequences of growth opportunities. Understanding incremental costs supports pricing decisions, capacity planning, and investment evaluation. Effective management of incremental costs ensures that business expansion generates sufficient benefits to justify the additional expenditure incurred.

(g) Decremental Cost

Decremental Cost refers to the reduction in total cost that occurs when the level of business activity, production volume, or operations decreases. It represents the amount by which costs decline as a result of reducing output, discontinuing a product line, closing a department, or eliminating a specific activity. Decremental cost is the opposite of incremental cost, which measures the additional cost arising from an increase in activity. This cost concept is important in managerial decision-making because it helps management evaluate the financial impact of reducing operations. For example, if a company decides to stop producing a particular product, the costs that can be avoided, such as direct materials, direct labour, and certain overhead expenses, constitute decremental costs. By identifying these costs, management can determine whether reducing or discontinuing an activity will improve profitability.

10. Classification According to Costing Techniques

Certain costs are classified according to the costing methods used for analysis.

(a) Marginal Cost

variable costs because fixed costs generally remain unchanged in the short run. Marginal cost analysis is widely used in pricing decisions, profit planning, and production management. By comparing marginal cost with additional revenue, managers can determine whether increased production will be profitable. Understanding marginal costs helps organizations optimize output levels and maximize profits. This classification is a fundamental concept in cost accounting and managerial economics and supports efficient decision-making in competitive business environments.

(b) Standard Cost

Standard cost is a predetermined cost established under normal operating conditions. It represents the expected cost of materials, labour, and overheads required to produce a product or service. Organizations use standard costs as benchmarks for performance evaluation and cost control. Actual costs are compared with standard costs to identify variances and determine corrective actions. Standard costing promotes efficiency, accountability, and continuous improvement. It also simplifies budgeting and planning processes. By establishing realistic performance targets, standard costs help organizations monitor operations effectively and maintain financial discipline.

(c) Actual Cost

Actual Cost refers to the cost that has actually been incurred in producing a product, providing a service, or carrying out a business activity. It represents the real amount spent on materials, labour, overheads, and other expenses during a specific period. Unlike predetermined or standard costs, actual costs are recorded only after the transaction has taken place and are based on factual data obtained from accounting records. Therefore, actual cost reflects the true financial resources consumed in business operations.=

11. Classification According to Traceability

(a) Traceable Cost

Traceable costs are costs that can be directly identified and assigned to a specific product, department, process, project, or activity. These costs arise solely because of the existence of a particular cost object and would disappear if that cost object did not exist. Examples include the salary of a department manager, materials used for a specific project, and machinery dedicated to a particular production line. Traceable costs provide accurate information about the profitability and performance of individual segments. Since they can be directly linked to a specific activity, they help management evaluate efficiency, control costs, and make informed decisions regarding resource allocation and operational improvement.

(b) Common Cost

Common costs are costs incurred for the benefit of multiple products, departments, processes, or activities and cannot be directly traced to any single cost object. These costs are shared among various segments of the organization and therefore require allocation using suitable methods. Examples include the salary of the chief executive officer, corporate office rent, security expenses, and general administrative costs. Common costs support overall business operations rather than any particular activity. Proper allocation of common costs is important for determining total cost and profitability. However, because allocation methods may vary, common costs can sometimes create challenges in performance evaluation and cost analysis.

by

by