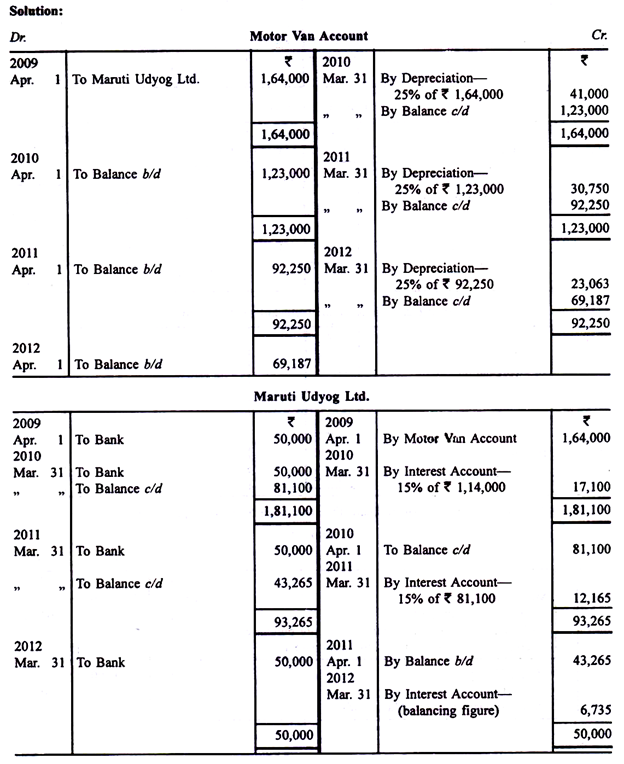

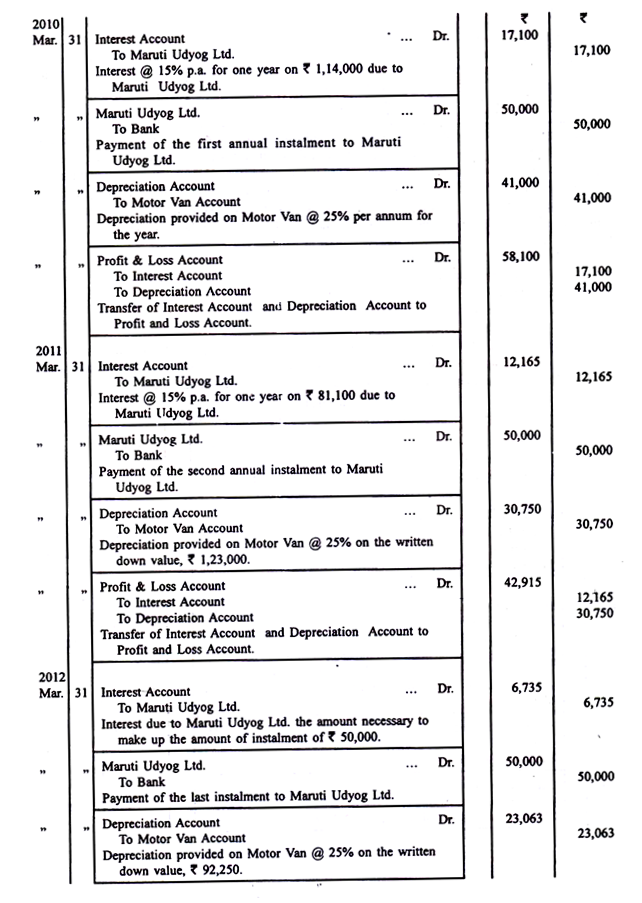

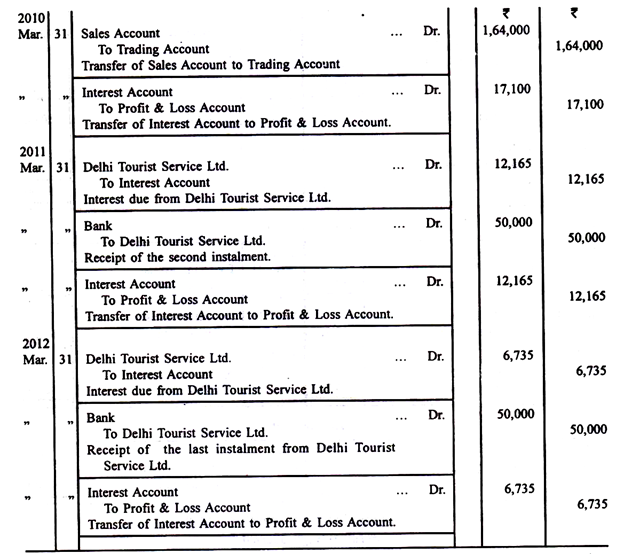

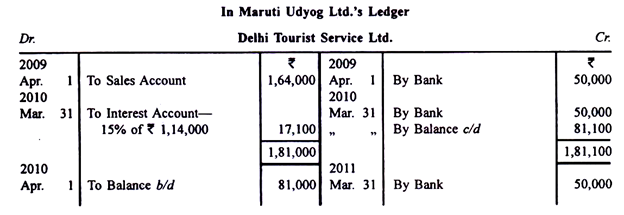

Valuation of Rights Issue of Share

by

by Rghts issue allows existing shareholders to maintain their proportionate ownership in a company by purchasing additional shares at a discounted price before they are offered to the public. This method ensures that shareholders are not diluted due to the issuance of new shares. It is an effective way for companies to raise funds without incurring debt. Shareholders can either exercise their rights, sell them in the market, or let them lapse if they do not wish to participate in the offering.

Need for Valuation of Rights Issue:

-

It helps in determining the fair price of the rights and whether it is beneficial for shareholders to subscribe.

-

Ensures transparency and fairness in the issuance process.

-

Helps investors decide whether to subscribe, sell, or ignore the rights.

-

Assists companies in setting the right issue price to attract sufficient subscription.

-

Prevents market distortions by ensuring that the issue price is competitive.

Formula for Valuation of Rights Issue:

The theoretical value of rights is calculated using the following formula:

Theoretical Ex-Rights Price (TERP) = [(Old Shares × Market Price) + (New Shares × Issue Price)]Total Shares After Issue

Value of Right per Share = Market Price Before Rights Issue − TERP

Where:

-

Market Price = The prevailing market price of the share before the rights issue.

-

Issue Price = The price at which new shares are issued.

-

Old Shares = Number of shares already held.

-

New Shares = Number of shares issued under the rights offer.

Methods of Valuation of Rights Issue:

1. Theoretical Ex-Rights Price (TERP) Method

The Theoretical Ex-Rights Price (TERP) method calculates the adjusted market price of a share after the rights issue. It assumes that the total value of shares remains unchanged, but the price per share decreases due to the increased number of shares. The formula used is:

TERP = [(Old Shares × Market Price) + (New Shares × Issue Price)] / Total Shares After Issue

This method provides a theoretical benchmark for post-rights share price, allowing investors to compare whether the market price aligns with expectations. It helps in understanding the potential impact of the rights issue on the company’s valuation.

2. Market Price Adjustment Method

This method assumes that the market price of shares adjusts based on the new supply of shares from the rights issue. It is based on the principle that the market will determine the fair price of shares post-issue, depending on demand and investor sentiment. The value of the right is calculated as:

Value of Right = Market Price Before Rights Issue − TERP

This method helps investors determine whether exercising their rights is beneficial compared to purchasing shares in the open market. It is useful when market fluctuations impact the perceived value of the rights issue.

3. Net Present Value (NPV) Method

Net Present Value (NPV) method values the rights issue by estimating the present value of future cash flows generated from the newly issued shares. It considers expected dividends, potential capital appreciation, and the time value of money. The formula used is:

NPV = ∑ [Expected Cash Flows / (1+r)^t]

where r is the discount rate, and t is the time period. This method is useful for long-term investors who want to assess whether the rights issue will generate sufficient returns over time. It provides a comprehensive view of the financial benefits of subscribing to the rights issue.

4. Book Value Method

Book Value Method calculates the value of rights based on the company’s book value (net assets) before and after the rights issue. It considers the net worth per share and determines how the issue affects the company’s financial position. The value of the right is calculated as:

Book Value Per Share = Total Equity / Number of Shares Outstanding

This method is suitable for conservative investors who focus on the intrinsic value of shares rather than market speculation. It provides an objective way to assess whether the rights issue is fairly priced.

5. Earnings Per Share (EPS) Adjustment Method

EPS Adjustment Method evaluates how the rights issue affects the company’s earnings per share (EPS). Since issuing new shares increases the total number of shares, EPS may decline unless the additional capital leads to higher profits. The adjusted EPS is calculated as:

Adjusted EPS = Net Profit / Total Shares After Issue

Investors use this method to determine whether the rights issue enhances or dilutes earnings potential. If the company utilizes the raised capital effectively, EPS may remain stable or increase, making the rights issue attractive.