EBIT-EPS analysis for Capital Structure Decision

by

by EBIT-EPS Analysis is a financial tool used to determine the impact of different financing options (debt and equity) on a company’s Earnings Per Share (EPS) at various levels of Earnings Before Interest and Taxes (EBIT). It helps in capital structure decision-making, allowing firms to choose between debt financing (which increases financial leverage) and equity financing (which avoids fixed interest costs but dilutes ownership). The analysis involves computing EPS for different EBIT levels to identify the indifference point, where EPS remains the same regardless of financing choice. Companies aim to maximize EPS while managing financial risk and shareholder value.

Meaning of EBIT

Earnings Before Interest and Taxes (EBIT) refers to the operating profit of the firm.

It is the income earned from business operations before deducting interest on loans and income tax.

EBIT = OperatingRevenue – OperatingExpenses

It measures the earning capacity of the firm independent of financing decisions.

Meaning of EPS

Earnings Per Share (EPS) represents the earnings available to each equity shareholder.

It indicates the profitability of the company from the shareholders’ point of view.

EPS = Earnings available to equity shareholders / Number of equity shares

Higher EPS means higher return to shareholders and increased market value of shares.

Financial Leverage and EBIT–EPS

The analysis is closely related to financial leverage.

Financial leverage means the use of debt in capital structure to increase return to equity shareholders.

-

If EBIT is high → Debt financing increases EPS

-

If EBIT is low → Debt financing decreases EPS

Therefore, proper use of debt can increase shareholders’ wealth.

Advantages of EBIT-EPS Analysis

Although EBIT–EPS analysis is a useful technique for selecting an appropriate financing plan and capital structure, it is not free from defects. The analysis mainly concentrates on earnings per share and ignores several practical aspects of financial decision-making. Therefore, it should not be used as the only basis for financing decisions.

The major limitations of EBIT–EPS analysis are explained below:

- Ignores Business Risk

EBIT–EPS analysis assumes that the operating income (EBIT) is known and stable. In reality, business earnings fluctuate due to changes in demand, competition, economic conditions and technology. If EBIT decreases unexpectedly, the company may not be able to meet interest obligations on debt. Hence, the analysis does not properly consider business risk, which is an important factor in financial planning.

- Focuses Only on EPS

The technique gives importance only to earnings per share. However, maximizing EPS does not always mean maximizing shareholders’ wealth. Shareholders are also concerned with share price, dividends, safety of investment and future growth. A plan with higher EPS may involve higher risk and may reduce the market value of shares. Therefore, EPS alone is not a complete measure of financial performance.

- Neglects Financial Risk

EBIT–EPS analysis encourages the use of debt because it often increases EPS at higher levels of EBIT. However, excessive debt increases financial risk and the possibility of insolvency. The company must pay interest regardless of profit. The analysis does not give adequate weight to the risk arising from heavy borrowing, which may endanger the long-term stability of the firm.

- Assumes Constant Interest and Tax Rates

The analysis assumes that interest rates and tax rates remain constant. In actual business conditions, interest rates change due to market fluctuations and government policies. Similarly, tax rates may also vary. Changes in these rates directly affect EPS and the cost of capital. Hence, results of the analysis may become unrealistic or misleading.

- Ignores Market Conditions

EBIT–EPS analysis does not consider the condition of the capital market. Sometimes it may not be possible to issue shares or debentures due to unfavorable market situations. Investor preferences, economic recession and stock market trends also affect financing decisions. Since these practical aspects are ignored, the analysis may not always be applicable in real situations.

- No Consideration of Control

Issue of equity shares reduces the ownership control of existing shareholders. Many companies avoid issuing new shares to maintain management control. EBIT–EPS analysis does not consider this important aspect. It only compares EPS and ignores the effect of financing decisions on voting rights and managerial control.

- Unrealistic Assumption of Fixed EBIT Levels

The technique compares financing plans at different EBIT levels, but predicting exact EBIT in advance is difficult. Business profits are uncertain and affected by several external factors. If the actual EBIT differs from estimated EBIT, the selected financing plan may not be suitable. Therefore, the analysis may lead to wrong decisions when profit estimates are inaccurate.

- Does Not Consider Cash Flow Position

EBIT–EPS analysis is based on accounting profits rather than cash flows. However, interest and loan repayments require actual cash payments. A firm may show high EPS but may still face cash shortage. Ignoring liquidity position may create financial difficulties and even bankruptcy.

- Short-Term Perspective

The analysis mainly focuses on immediate effect on EPS and does not consider long-term consequences such as growth opportunities, financial flexibility and sustainability. A financing plan beneficial in the short run may harm the company in the long run. Therefore, it provides only a partial view of financial decision-making.

Indifference Points:

The indifference point, often called as a breakeven point, is highly important in financial planning because, at EBIT amounts in excess of the EBIT indifference level, the more heavily levered financing plan will generate a higher EPS. On the other hand, at EBIT amounts below the EBIT indifference points the financing plan involving less leverage will generate a higher EPS.

Indifference points refer to the EBIT level at which the EPS is same for two alternative financial plans. According to J. C. Van Home, ‘Indifference point refers to that EBIT level at which EPS remains the same irrespective of debt equity mix’. The management is indifferent in choosing any of the alternative financial plans at this level because all the financial plans are equally desirable. The indifference point is the cut-off level of EBIT below which financial leverage is disadvantageous. Beyond the indifference point level of EBIT the benefit of financial leverage with respect to EPS starts operating.

The indifference level of EBIT is significant because the financial planner may decide to take the debt advantage if the expected EBIT crosses this level. Beyond this level of EBIT the firm will be able to magnify the effect of increase in EBIT on the EPS.

In other words, financial leverage will be favorable beyond the indifference level of EBIT and will lead to an increase in the EPS. If the expected EBIT is less than the indifference point then the financial planners will opt for equity for financing projects, because below this level, EPS will be more for less levered firm.

- Computation:

We have seen that indifference point refers to the level of EBIT at which EPS is the same for two different financial plans. So the level of that EBIT can easily be computed. There are two approaches to calculate indifference point: Mathematical approach and graphical approach.

- Graphical Approach:

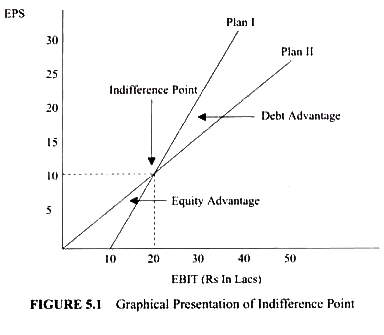

The indifference point may also be obtained using a graphical approach. In Figure 5.1 we have measured EBIT along the horizontal axis and EPS along the vertical axis. Suppose we have two financial plans before us: Financing by equity only and financing by equity and debt. Different combinations of EBIT and EPS may be plotted against each plan. Under Plan-I the EPS will be zero when EBIT is nil so it will start from the origin.

The curve depicting Plan I in Figure 5.1 starts from the origin. For Plan-II EBIT will have some positive figure equal to the amount of interest to make EPS zero. So the curve depicting Plan-II in Figure 5.1 will start from the positive intercept of X axis. The two lines intersect at point E where the level of EBIT and EPS both are same under both the financial plans. Point E is the indifference point. The value corresponding to X axis is EBIT and the value corresponding to 7 axis is EPS.

These can be found drawing two perpendiculars from the indifference point—one on X axis and the other on Taxis. Similarly we can obtain the indifference point between any two financial plans having various financing options. The area above the indifference point is the debt advantage zone and the area below the indifference point is equity advantage zone.

Above the indifference point the Plan-II is profitable, i.e. financial leverage is advantageous. Below the indifference point Plan I is advantageous, i.e. financial leverage is not profitable. This can be found by observing Figure 5.1. Above the indifference point EPS will be higher for same level of EBIT for Plan II. Below the indifference point EPS will be higher for same level of EBIT for Plan I. The graphical approach of indifference point gives a better understanding of EBIT-EPS analysis.

Financial Breakeven Point:

In general, the term Breakeven Point (BEP) refers to the point where the total cost line and sales line intersect. It indicates the level of production and sales where there is no profit and no loss because here the contribution just equals to the fixed costs. Similarly financial breakeven point is the level of EBIT at which after paying interest, tax and preference dividend, nothing remains for the equity shareholders.

In other words, financial breakeven point refers to that level of EBIT at which the firm can satisfy all fixed financial charges. EBIT less than this level will result in negative EPS. Therefore EPS is zero at this level of EBIT. Thus financial breakeven point refers to the level of EBIT at which financial profit is nil.

Financial Break Even Point (FBEP) is expressed as ratio with the following equation: