COST CONTROL

Cost control refers to the process of regulating and monitoring costs to ensure that they remain within predetermined limits or standards. It involves setting cost standards or budgets in advance and comparing actual costs with these standards. Any deviations or variances are analyzed, and corrective actions are taken to prevent unnecessary expenditure. Cost control focuses on preventing wastage, improving efficiency, and maintaining costs at an acceptable level. It is a continuous and preventive function aimed at achieving planned cost targets without compromising operational efficiency.

Cost control makes use of techniques such as standard costing, budgetary control, variance analysis, and responsibility accounting. It helps management maintain financial discipline, ensures optimal utilization of resources, and supports smooth functioning of business operations. However, cost control does not aim at reducing costs beyond the established standards; it mainly ensures that costs do not exceed the predetermined limits.

Objectives of Cost Control

- Reduction of Wastage and Inefficiency

One of the primary objectives of cost control is to reduce wastage and inefficiency in the use of materials, labour, and other resources. By setting standards and monitoring actual performance, management can identify losses arising from spoilage, idle time, or poor supervision. Effective cost control ensures optimum utilization of resources and prevents unnecessary expenditure, thereby improving operational efficiency and lowering overall production costs.

- Achievement of Cost Standards

Cost control aims to ensure that actual costs remain within the limits of predetermined cost standards or budgets. Standards act as benchmarks against which actual performance is measured. Any deviation from these standards is promptly analyzed and corrective action is taken. This objective helps organizations maintain financial discipline and ensures that operations are carried out according to planned cost levels.

- Improvement in Profitability

Another important objective of cost control is to improve profitability by keeping costs under check. When costs are controlled effectively, savings are generated without affecting output quality or efficiency. Reduced costs directly contribute to higher profit margins. By controlling expenses at every stage of production and operation, businesses can enhance their financial performance and long-term sustainability.

- Facilitation of Efficient Planning

Cost control supports efficient planning by providing accurate cost data and setting cost targets in advance. Budgets and standards prepared under cost control act as guides for future activities. This objective helps management plan production levels, resource requirements, and expenditure systematically. Proper planning ensures smooth operations and avoids unexpected financial strain due to uncontrolled costs.

- Assistance in Managerial Decision Making

Cost control provides relevant cost information required for effective managerial decision making. Decisions related to pricing, production volume, product mix, and cost-saving measures depend on reliable cost data. By controlling and analyzing costs, management can make informed decisions that align with organizational objectives and ensure optimal use of available resources.

- Promotion of Cost Consciousness

An important objective of cost control is to develop cost consciousness among employees at all levels of management. When cost standards are set and performance is regularly reviewed, employees become aware of the importance of controlling costs. This creates a sense of responsibility and encourages efficient working practices, resulting in reduced wastage and improved overall performance.

- Maintenance of Competitive Pricing

Cost control helps organizations maintain competitive pricing by preventing unnecessary cost escalation. When production and operating costs are kept under control, products can be priced competitively without sacrificing profit margins. This objective is especially important in highly competitive markets where price plays a crucial role in attracting and retaining customers.

- Ensuring Effective Internal Control

Cost control aims to strengthen the internal control system by ensuring proper authorization, recording, and monitoring of costs. Regular comparison of actual costs with standards helps detect errors, inefficiencies, and irregularities at an early stage. This objective improves transparency, accountability, and reliability of cost information, supporting effective management control and organizational efficiency.

Techniques of Cost Control

Budgetary control is an important technique of cost control in which budgets are prepared for various activities and departments in advance. Actual performance is compared with budgeted figures to identify deviations. Variances are analyzed and corrective actions are taken to control excessive expenditure. This technique helps in planning, coordination, and control of costs, ensuring that resources are utilized efficiently and organizational objectives are achieved.

Standard costing involves setting standard costs for materials, labour, and overheads and comparing them with actual costs incurred. Variances between standard and actual costs are calculated and analyzed to identify reasons for inefficiencies. This technique helps management take timely corrective action, improve performance, and maintain cost discipline. Standard costing is widely used as an effective tool for controlling production and operating costs.

Variance analysis is a technique used to analyze the differences between standard costs and actual costs. These variances may relate to material price, material usage, labour efficiency, or overheads. By identifying favorable and unfavorable variances, management can locate problem areas and take corrective measures. Variance analysis provides valuable feedback for improving cost efficiency and operational performance.

- Responsibility Accounting

Responsibility accounting divides the organization into responsibility centers such as cost centers, profit centers, and investment centers. Each center is assigned responsibility for controlling costs under its control. Performance is evaluated by comparing actual costs with targets for each center. This technique promotes accountability, improves managerial efficiency, and ensures effective cost control at various levels of management.

- Inventory Control Techniques

Inventory control techniques such as EOQ, ABC analysis, and stock level determination help control material costs. Proper inventory management reduces carrying costs, avoids stock shortages, and minimizes wastage or obsolescence. By maintaining optimum stock levels and monitoring material usage, organizations can control material costs effectively and ensure smooth production operations.

- Cost Control through Labour Control

Labour control techniques focus on controlling labour costs by improving productivity and efficiency. Methods such as time keeping, time booking, incentive wage plans, and control of idle time and overtime are used. Efficient labour control ensures optimal utilization of workforce, reduces unnecessary labour costs, and contributes significantly to overall cost control.

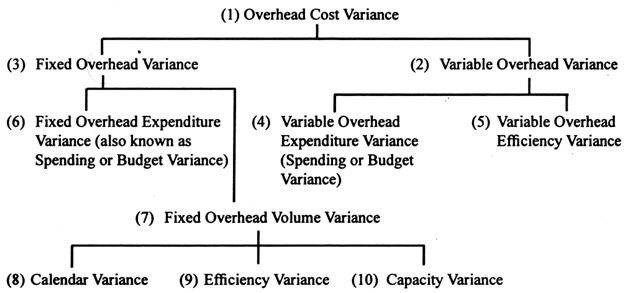

Overhead control involves controlling indirect costs such as factory, office, and selling overheads. This is achieved through proper classification, allocation, apportionment, and absorption of overheads. Budgeting and standard costing help monitor overhead expenses. Effective overhead control prevents cost escalation and ensures accurate product costing and improved profitability.

- Cost Reporting and Review

Regular cost reports and reviews are essential techniques of cost control. Cost reports provide detailed information on costs incurred, variances, and performance trends. Continuous review of these reports enables management to detect inefficiencies, take timely corrective actions, and improve decision making. Effective reporting strengthens internal control and supports efficient cost management.

Steps Involved in Cost Control

Step 1. Establishment of Cost Standards

The first step in cost control is the establishment of cost standards or targets for materials, labour, and overheads. These standards are based on past performance, technical studies, and management policies. Cost standards serve as benchmarks against which actual costs are compared. Properly set standards help management plan operations efficiently and provide a clear basis for controlling costs.

Step 2. Preparation of Budgets

Preparation of budgets is an important step in cost control. Budgets estimate future costs and revenues for different departments and activities. They define the permissible limits of expenditure and guide operational planning. Budgets ensure coordination among departments and help management allocate resources effectively. Budgeted figures also act as control tools for measuring actual performance.

Step 3. Recording of Actual Costs

Accurate recording of actual costs incurred during production or operations is essential for effective cost control. Costs relating to materials, labour, and overheads are collected systematically through cost accounting records. Proper recording ensures reliability of cost data and facilitates meaningful comparison with standards or budgets for identifying deviations.

Step 4. Comparison of Actual Costs with Standards

In this step, actual costs are compared with predetermined standards or budgeted figures. The purpose of this comparison is to identify variances between expected and actual performance. This helps management understand whether costs are under control or exceeding limits. Timely comparison enables early detection of inefficiencies and cost overruns.

Step 5. Analysis of Variances

Variance analysis involves identifying the causes of differences between standard costs and actual costs. Variances may arise due to price changes, inefficient usage of resources, or operational issues. Analyzing variances helps management locate responsibility and understand problem areas. This step provides valuable information for improving efficiency and cost management.

Step 6. Taking Corrective Action

After analyzing variances, management takes corrective actions to eliminate inefficiencies and prevent recurrence of unfavorable variances. Corrective measures may include improving supervision, revising procedures, training employees, or changing suppliers. Prompt corrective action ensures that costs remain under control and organizational performance improves.

Step 7. Continuous Monitoring and Reporting

Cost control is a continuous process that requires regular monitoring and reporting of cost performance. Periodic cost reports provide feedback to management on cost trends and deviations. Continuous monitoring helps maintain cost discipline, supports informed decision making, and ensures long-term control over costs.

Components of Cost Control

Material control is a key component of cost control, focusing on the efficient use and management of raw materials, components, and consumables. It involves proper purchasing, storage, issuing, and accounting of materials. Techniques like inventory control, ABC analysis, and standard pricing help prevent wastage, pilferage, and overstocking, ensuring that material costs are minimized and resources are optimally utilized.

Labour control aims to manage and reduce labour costs while maintaining productivity. It includes timekeeping, time booking, monitoring efficiency, and controlling idle time and overtime. Incentive schemes and proper workforce allocation are also part of labour control. Effective labour control ensures optimal utilization of human resources and contributes significantly to overall cost reduction and operational efficiency.

Overhead control involves managing indirect costs such as factory, administrative, and selling overheads. It includes proper classification, allocation, apportionment, and absorption of overheads. Monitoring actual overheads against standards or budgets helps identify inefficiencies and prevent unnecessary expenditure. Effective overhead control ensures accurate costing of products and supports profitability improvement.

Budgetary control is a systematic approach to planning and controlling costs by setting budgets for various departments and activities. Actual performance is compared with budgeted figures to identify variances. This component ensures that resources are allocated efficiently, expenditures are kept within limits, and financial discipline is maintained across the organization.

- Standard Costing and Variance Analysis

Standard costing and variance analysis form an important component of cost control. Cost standards are predetermined for materials, labour, and overheads, and actual costs are compared against them. Variances are analyzed to identify reasons for deviations and corrective actions are taken. This helps maintain cost efficiency, prevent wastage, and achieve operational targets.

Performance measurement involves assessing the efficiency of materials, labour, and overhead utilization. Key performance indicators, efficiency ratios, and cost reports help management evaluate departmental and individual performance. Identifying underperformance allows corrective action, motivating employees, improving productivity, and ensuring that cost control objectives are achieved.

Regular reporting and continuous monitoring of cost performance are essential for effective cost control. Detailed cost reports provide insights into material consumption, labour efficiency, and overhead expenditure. Continuous monitoring helps management detect deviations early, take corrective action promptly, and maintain overall control over costs.

- Responsibility Accounting

Responsibility accounting assigns cost control accountability to different departments, cost centers, or managers. Each responsible person is evaluated based on their ability to control costs within their area. This component ensures accountability, promotes cost-conscious behavior, and supports overall organizational cost control objectives.

COST REDUCTION

Cost reduction is a systematic and continuous process of lowering the unit cost of production or operation without affecting the quality, performance, or usefulness of the product or service. Unlike cost control, which focuses on maintaining costs within set limits, cost reduction aims at permanently reducing costs. It involves identifying and eliminating unnecessary or avoidable expenses through improved methods, better utilization of resources, and adoption of new techniques.

Cost reduction uses tools such as value analysis, work study, process improvement, and standardization. It encourages innovation, efficiency, and cost consciousness at all levels of management. The objective of cost reduction is to achieve long-term savings, enhance competitiveness, and improve profitability by making operations more efficient and economical.

Objectives of Cost Reduction

- Minimize Production Costs

The primary objective of cost reduction is to minimize production costs without affecting the quality of products or services. By analyzing the cost structure, management identifies areas of inefficiency, wastage, and unnecessary expenditure. Implementing improved methods, optimizing resources, and controlling unnecessary overheads helps in reducing unit costs. Lower production costs increase profitability, enhance competitiveness, and allow the organization to allocate resources more efficiently across various operations.

- Improve Operational Efficiency

Cost reduction aims to improve operational efficiency by streamlining production processes and eliminating unnecessary activities. This involves optimizing material usage, labour productivity, and machine utilization. By reducing idle time, minimizing defects, and improving workflow, organizations can achieve higher output with the same or fewer resources. Enhanced operational efficiency contributes to cost savings, better resource utilization, and overall performance improvement, making the organization more competitive in the market.

A key objective of cost reduction is to enhance profitability by decreasing overall expenses. Reduced production and operational costs directly increase profit margins. By controlling material wastage, labour inefficiencies, and overhead expenditures, businesses can retain more revenue as profit. Consistent cost reduction efforts help organizations maintain sustainable growth, fund expansion projects, and improve financial stability, thereby ensuring long-term success and shareholder value.

- Encourage Resource Optimization

Cost reduction promotes optimum utilization of available resources, including materials, manpower, and machinery. It encourages management to use resources efficiently, reduce wastage, and avoid overproduction. By allocating resources judiciously, organizations can produce more output at lower costs, conserve valuable inputs, and maintain production sustainability. Effective resource optimization reduces unnecessary expenditure and contributes to better financial and operational performance.

Cost reduction seeks to lower costs without compromising product quality. Techniques such as value analysis, process improvement, and standardization aim to eliminate waste while maintaining or improving product standards. By controlling costs intelligently, organizations can ensure customer satisfaction, build brand reputation, and remain competitive. Maintaining quality alongside cost efficiency ensures long-term market success and customer loyalty.

- Promote Continuous Improvement

Cost reduction encourages continuous improvement in processes, methods, and resource management. Organizations regularly review operations to identify areas where costs can be minimized. This objective instills a culture of efficiency and innovation within the organization. Continuous cost reduction efforts lead to better productivity, reduced wastage, and streamlined operations, contributing to sustained competitiveness and financial health.

- Strengthen Competitive Advantage

Reducing costs enables organizations to price products more competitively while maintaining profitability. Cost reduction helps businesses respond effectively to market competition, attract more customers, and increase market share. By lowering costs strategically, companies can offer better value without sacrificing margins, strengthening their position in the market and ensuring long-term sustainability.

- Facilitate Strategic Decision-Making

Cost reduction provides management with detailed insights into areas of excessive expenditure and inefficiency. This information supports strategic decision-making regarding process improvement, resource allocation, production planning, and investment. By understanding cost drivers, management can make informed decisions that reduce expenses, enhance profitability, and align operations with organizational goals. Cost reduction ensures that decisions are financially sound and operationally efficient.

Techniques of Cost Reduction

Value analysis is a technique used to reduce costs by examining products and processes to eliminate unnecessary expenses while maintaining quality and functionality. It involves analyzing each component of a product or service to determine its value contribution. By removing or modifying non-essential elements, organizations can lower production costs, improve efficiency, and offer competitive pricing without compromising customer satisfaction.

Process improvement focuses on enhancing production or operational processes to reduce waste, defects, and inefficiencies. Techniques such as workflow optimization, automation, and lean management help streamline operations. By improving processes, organizations can achieve higher output with fewer resources, minimize delays, and reduce labour and material costs. This technique ensures sustainable cost savings and increased operational efficiency.

Standardization involves setting uniform specifications for materials, components, and processes to minimize variations and inefficiencies. By using standard sizes, methods, and procedures, organizations can reduce material wastage, simplify production, and lower procurement costs. Standardization ensures consistency, reduces errors, and enhances productivity, contributing significantly to overall cost reduction.

Budgetary control is a technique where budgets are prepared for departments, activities, or projects to limit expenses. Actual costs are compared with budgeted figures, and deviations are analyzed. This helps identify areas of excessive expenditure and take corrective measures. Budgetary control ensures that costs are kept within planned limits and resources are allocated efficiently, supporting long-term cost reduction objectives.

- Efficient Material Management

Efficient material management techniques such as inventory control, ABC analysis, and Economic Order Quantity (EOQ) help reduce material costs. Proper purchasing, storage, and issue practices prevent overstocking, stockouts, and wastage. By controlling material usage and maintaining optimal inventory levels, organizations can significantly reduce costs associated with storage, spoilage, and obsolescence.

- Labour Productivity Improvement

Labour productivity improvement techniques aim to enhance workforce efficiency and reduce labour costs. Methods include training, incentive schemes, performance monitoring, and proper workforce allocation. By improving labour output per unit of input and minimizing idle time or overtime, organizations can reduce overall labour expenditure while maintaining high-quality output.

- Technological Upgradation

Adopting new technologies and modern equipment can reduce production costs in the long run. Automation, mechanization, and advanced machinery improve efficiency, reduce manual errors, and optimize resource usage. Though initial investment may be high, technological upgradation leads to substantial cost savings through higher productivity, reduced wastage, and lower labour costs.

- Outsourcing and Make-or-Buy Decisions

Outsourcing non-core activities or making strategic make-or-buy decisions can reduce costs. By sourcing goods or services from specialized vendors at lower costs, organizations can save on labour, overheads, and capital expenditure. Cost-effective outsourcing ensures that resources are focused on core activities while minimizing operational expenses.

Waste minimization involves reducing scrap, defects, and unnecessary consumption of resources in production or operations. Techniques such as lean manufacturing, Kaizen, and continuous improvement help identify and eliminate waste. Minimizing waste lowers material, labour, and overhead costs, contributing directly to cost reduction and improved profitability.

Steps in Cost Reduction

Step 1. Identify Cost Centers

The first step in cost reduction is to identify the cost centers or departments where costs are incurred. These centers may include production, administration, sales, or services. By pinpointing areas where significant expenses occur, management can focus efforts on analyzing and reducing costs effectively. Identifying cost centers ensures that cost reduction measures are applied systematically to the most impactful areas.

Step 2. Analyze Cost Components

Once cost centers are identified, the next step is to analyze various cost components such as materials, labour, and overheads. Detailed examination helps detect areas of wastage, inefficiency, and unnecessary expenditure. By understanding the contribution of each component to total cost, management can prioritize areas that offer maximum potential for cost reduction.

Step 3. Set Cost Reduction Targets

After analyzing costs, specific cost reduction targets are set for each department or cost component. These targets serve as benchmarks for performance evaluation. Clear objectives guide employees and managers in adopting measures to achieve savings. Setting realistic and measurable targets ensures accountability and helps monitor the progress of cost reduction initiatives.

Step 4. Explore Cost Reduction Methods

Management identifies suitable methods and techniques for reducing costs. This may include value analysis, process improvement, standardization, automation, and outsourcing. Selecting the right approach depends on the nature of operations and the type of costs involved. Properly chosen methods ensure effective and sustainable cost reduction without compromising quality or efficiency.

Step 5. Implement Cost Reduction Measures

The next step is the practical implementation of the selected cost reduction methods. This involves reorganizing processes, improving workflow, introducing new technology, or adopting better resource management practices. Successful implementation requires cooperation from all departments and active participation of employees to achieve the desired cost savings.

Step 6. Monitor and Measure Results

After implementation, continuous monitoring of cost performance is essential. Actual costs are compared with targets to assess the effectiveness of cost reduction measures. Regular reporting and performance analysis help management identify areas needing further improvement and ensure that cost reduction objectives are met consistently.

Step 7. Take Corrective Action

If cost reduction targets are not achieved, management must take corrective action. This may involve modifying processes, retraining staff, adjusting resource allocation, or adopting alternative techniques. Timely corrective measures ensure that cost reduction efforts remain on track and desired savings are realized without affecting operational efficiency.

Step 8. Encourage Continuous Improvement

Cost reduction is a continuous process. Organizations must foster a culture of cost consciousness and continuous improvement. Regular review of processes, adoption of best practices, and employee involvement help sustain cost reduction over time. Continuous improvement ensures long-term efficiency, competitiveness, and profitability.

Components of Cost Reduction

Material cost reduction focuses on minimizing expenses related to raw materials, components, and consumables. Techniques include bulk purchasing, standardization of materials, improved inventory management, and reducing wastage or spoilage. Proper material handling and supplier negotiation also help lower costs. Efficient material cost management ensures that production expenses are reduced without compromising the quality of the final product.

Labour cost reduction aims to optimize the use of human resources while minimizing wage and overhead expenditures. Methods include improving workforce productivity, training, performance-based incentives, reducing idle time, and avoiding unnecessary overtime. Efficient labour management ensures higher output at lower costs, contributing directly to overall cost reduction.

Overhead cost reduction involves controlling indirect expenses such as rent, utilities, depreciation, administrative expenses, and factory overheads. Techniques include energy conservation, better allocation of resources, automation, and outsourcing non-core activities. Proper management of overheads ensures that fixed and variable costs are minimized, improving profitability.

- Process and Operational Improvement

Improving production and operational processes is a key component of cost reduction. Streamlining workflows, eliminating inefficiencies, and adopting lean practices help reduce waste and optimize resource utilization. Continuous process improvement leads to lower production costs, better quality, and higher operational efficiency.

- Technological Upgradation

Investing in modern machinery, automation, and advanced production technologies helps reduce long-term costs. Although the initial investment may be significant, technological upgradation minimizes labour, time, and material wastage, resulting in higher efficiency and sustainable cost savings.

Standardization reduces costs by using uniform materials, components, and methods in production. It minimizes variations, simplifies procurement, and reduces wastage. Standardized processes also help in achieving consistent quality while lowering costs associated with errors and rework.

Minimizing waste in materials, labour, and processes is an essential component of cost reduction. Techniques like lean manufacturing, Kaizen, and process optimization help identify and eliminate unnecessary consumption, scrap, and defects. Reducing waste directly decreases production costs and enhances profitability.

- Outsourcing and Make-or-Buy Decisions

Outsourcing non-core functions or making strategic make-or-buy decisions helps reduce costs by leveraging external expertise and economies of scale. It allows organizations to focus on core activities while reducing expenditure on less critical operations. Efficient outsourcing contributes to lower operational costs and improved overall efficiency.

Key differences between Cost Control and Cost Reduction

| Aspect |

Cost Control |

Cost Reduction |

| Focus |

Limits |

Minimization |

| Objective |

Maintain |

Lower |

| Approach |

Preventive |

Corrective |

| Timing |

Continuous |

Periodic |

| Effect on Standard |

Within limits |

Below limits |

| Scope |

Narrow |

Broad |

| Quality Impact |

Neutral |

Considered |

| Methodology |

Standardization |

Innovation |

| Measurement |

Variances |

Cost savings |

| Resource Focus |

Efficiency |

Optimization |

| Management Role |

Supervisory |

Strategic |

| Long-Term Benefit |

Stability |

Profitability |

| Tools |

Budgets, Standards |

Process improvement |

| Dependency |

Standards |

Analysis |

| Nature |

Routine |

Improvement |

by

by