Closed and open economy Models

by

by Closed economy Models

A closed economy is a country that does not import or export. A closed economy sees itself as self-sufficient and claims it does not want to trade internationally. In fact, it believes it does not need to trade.

A closed economy is a type of economy where the import and export of goods and services don’t happen, which implies that the economy is self-sufficient and has no trading activity from outside economics. The sole purpose of such an economy is to meet all the domestic consumers’ needs within the country’s border.

In a completely closed economy, there are no imports or exports. The country claims that it produces everything its citizens need. We also refer to this type economy as isolationist or an autarky.

A closed economy is the opposite of an open economy or a free-market economy. Open economies trade with other nations; they import and export goods and services. Hence, we also call them trading nations.

Maintaining a closed economy is more difficult today than two hundred years ago.

Certain raw materials are vital for the production of many products. For example, without oil, a country would not be able to function today. Many countries, such as Japan, need to import nearly all their raw materials.

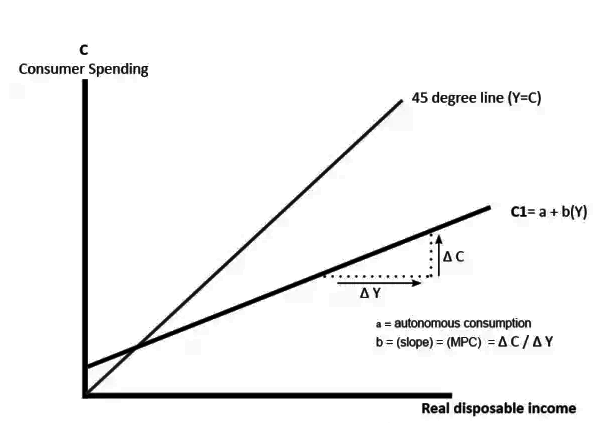

Y = Cd + Id + Gd + X

Were,

Y: National income

Cd: Total domestic consumption

Id: Total investment in domestic goods and services

Gd: Government purchases of domestic goods and services

X: Exports of domestic goods and services

Importance of Closed Economy

With globalization and international trade, it is impossible to establish and maintain a closed economy. The open economy has no restrictions on imports. An open economy carries the risk of depending too much on imports. The domestic players will not be able to compete with international players. To tackle this the governments, use quotas, tariffs, and subsidies.

Resource availability across the globe varies and is never constant. Thus, depending on this availability, an international player will find out the best place to procure a particular resource and come up with the best price. Domestic players who have constraints to globalize will not be able to produce the same product at a price at par or discount compared to an international player. Thus domestic players will not be able to compete with the foreign players and the government uses the above options to provide support to domestic players and also reduce dependency on imports.

Advantages

- It is isolated from neighbors, so there is no fear of coercion or interference.

- Transit costs will be usually very less in the closed economy.

- Taxes on goods and products will be less and controlled by the government, less burden for consumers.

- Domestic players need not compete with the outside players and price competition is less.

- The self-sufficient economy will create proper demand for domestic products and agricultural products and producers will be compensated appropriately.

- Price fluctuations and volatility are easily controllable.

Limitations

- The economy will not grow if they are short of resources like oil, gas, and coal.

- The consumer will not get the best price for commodities compared to global prices.

- In case of emergencies, the economy will be hit severely as most of its production is only domestic.

- They must be able to meet all of its domestic demand internally, which is a difficult task to accomplish.

- They will have restrictions on goods and services to be sold and thus the opportunity for the consumers in such markets is more.

- Isolated economies can be looked down upon by the developing nations and globally such an economy can expect a limited aid when the need comes.

Reasons for Closed Economy

There are a few reasons a country might choose to have a closed economy or other factors that will facilitate the maintenance and building of a closed economy. It is assumed that the economy is self-sufficient and doesn’t require any import outside domestic borders to meet all of its demands from consumers.

- Isolation: An economy might be physically isolated from its trading partners (consider an island or a country surrounded by mountains). The natural boundaries of a country will factor this reason and lead the economy towards a closed one.

- Transit Cost: Due to physical isolation the transportation cost of goods will be highest leading to high transit costs. It doesn’t make sense in trade if the price of goods is increased due to the high overheads of transport and thus the economy tends to close in such cases.

- Government Decree: Governments might close down borders for taxes, regulations purposes. Thus, they will decree the trade with other economies. Violations will be punished. The government will try to support its domestic producers and tax international players to generate revenue.

- Cultural Preferences: Citizens might prefer to contact and trade only with citizens, this will lead to another barrier and facilitate a closed economy. For example, when McDonald’s came to India, people opposed the outlets claiming they use beef in their dishes and it was against culture.

Open economy Models

An open economy is a type of economy where not only domestic actors but also entities in other countries engage in trade of products (goods and services). Trade can take the form of managerial exchange, technology transfers, and all kinds of goods and services. (However, certain exceptions exist that cannot be exchanged; the railway services of a country, for example, cannot be traded with another country to avail the service.)

It contrasts with a closed economy in which international trade and finance cannot take place.

The act of selling goods or services to a foreign country is called exporting. The act of buying goods or services from a foreign country is called importing. Exporting and importing are collectively called international trade.

There are a number of economic advantages for citizens of a country with an open economy. A primary advantage is that the citizen consumers have a much larger variety of goods and services from which to choose. Additionally, consumers have an opportunity to invest their savings outside the country. There are also economic disadvantages of an open economy. Open economies are interdependent on others and this exposes them to certain unavoidable risks.

If a country has an open economy, that country’s spending in any given year need not equal its output of goods and services. A country can spend more money than it produces by borrowing from abroad, or it can spend less than it produces and lend the difference to foreigners. As of 2014 there is no totally-closed economy.

he basic model

In a closed economy, all output is sold domestically, and expenditure is divided into three components: consumption, investment, and government purchases.

Y = C + I + G

where Y is the national income, C is the total consumption, I is the total investment and G is the total government expenditure. In an open economy, some output is sold domestically and some is exported to be sold abroad. We can divide expenditure on an open economy’s output Y into four components: Cd, consumption of domestic goods and services, Id, investment in domestic goods and services, Gd, government purchases of domestic goods and services, X, exports of domestic goods and services. The division of expenditure into these components is expressed in the identity

Y = Cd + Id + Gd + X.

The sum of the first three terms, Cd + I d + Gd, is domestic spending on domestic goods and services. The fourth term, X, is foreign spending on domestic goods and services (the value of exports).

Advantages

Lower Costs

Open economies are able to get cheaper imports and can sell exports at higher prices. In other words, both importers and exporters of open countries [and therefore, their consumers] benefit from price differentials.

Economic Growth

It is claimed that an open economy, with given productive resources, can have a higher GDP. Alternatively, for producing a given GDP, it spends a smaller quantity of productive resources.

This happens due to its enhanced access to improved and better technology which provides an upward thrust to economic development.

Global Prosperity and Flow of Productive Resources

Traditional economic thinking dealing with international economic transactions assumed that there was near absence of mobility (flow) of capital and other factors of production between countries.

Over time, however, the realities of international trade have belied this theory. Currently, enormous volumes of a variety of capital funds are circulating between world economies.

In addition, international flows of other inputs (raw materials and intermediate products, technology, institutional set ups, work ethos and, to some extent, even labour) have increased in varying degrees.

Some models of entrepreneurial and institutional set ups have gained the status of international standardisation. All this has also added to the overall global prosperity, as countries increasingly yearn, learn and earn together.

Superiority of Trade over Isolation

Some countries have been able to experience a rapid export-led economic growth. In contrast, it is difficult to find instances of widespread successful import substitution. Successful import substitution has been possible only in respect of a few specified industries.

Improved Availability of Goods and Services

International trade in goods and services enables each country to concentrate on the production of those goods in which it has a comparative cost advantage, and import those in which it has a comparative cost disadvantage. That way, it can add to the volume, variety and quality of goods and services that go into determining its GDP.

Impetus to Innovation

Open economies provide an incentive for research and adoption of innovations. This is because open economies have ‘lie benefit of a wider scope for their profitable application over bigger markets and recovery of huge research costs. However, being an open economy also has its drawbacks.

Disadvantages

- Footloose Funds:

Currently, large amounts of “footloose” (that is, short term and/or speculative type) funds are moving around the world in search of places where they can be “parked” (that is, invested temporarily) within acceptable levels of safety and return.

Therefore, any change in one or both of these determining factors can lead to a large scale international movement of these funds.

- Risk Exposure:

Open economies are interdependent. And this exposes them to certain unavoidable risks. Disturbances like trade cycles, and fluctuations in income, prices and employment etc., originating in one economy, spread to other economies also.

These disturbances may even gather strength in the process of dispersal. Consequently, all open economies, including the one from where a disturbance originates, are likely to suffer in varying degrees. Expectedly, the damage inflicted on the interdependent open economies is influenced by the following factors.

Size of the Economy:

More precisely, it is the proportion contributed by the originating economy in international economic transactions and the nature of these transactions.

By way of examples of this phenomenon, we can consider countries which have a large share in short-term capital flows or in energy sources like petroleum products, etc. and countries whose currencies are used as foreign exchange reserves, such as the US and the UK.

Intensity of the Initial Disturbance:

Other things being equal, a disturbance of higher initial intensity is likely to cause a correspondingly greater damage to the interconnected open economies.

Degree of Integration:

This factor is self-explanatory. Economies with greater restrictions on international economic transactions tend to suffer less when a disturbance originates in some other country.

When a number of South East Asian economies suffered heavily on account of a severe financial crisis in 1997-98, India could escape this disaster.

This was because Indian rupee was not freely convertible on capital account and short term capital funds could not leave the country on a large scale.

- Indebtedness:

Large scale increase in international capital flows has resulted in problems like heavy indebtedness of certain countries and their inability to repay their debts. Starting with 1970s banks and other financial institutions, in search for better returns extended huge loans to some countries.

Their borrowers, however, could not use these loans for increasing their export earnings out of which to service them. Some of them could not “absorb” these loans productively for promoting their economic growth. This resulted in frequent bankruptcies of the borrowing governments and associated financial crises.

- Import Dependence:

Certain varieties of imports can expose a country to undue political, economic and cultural risk. Examples are imports necessary for defence, health care, energy needs, food needs, and the like.

- Growth Bringing Poverty:

There are instances where an expansion in international trade of a country has resulted in what is termed “immiserising growth”.

It happens when international trade adds to the productive capacity of a country, but its terms of trade deteriorate so much that there is a net decline in its economic welfare.

In addition, it is also possible that while there is an overall increase in economic welfare of the country, some sections happen to be net losers.

- Constraints on Resource Use:

It is possible that a country is forced to adopt certain production technologies which do not let it make an optimum use of its factor-endowment.

Alternatively, it may have to face restrictions on its exports. Such a state of affairs may be thrust upon a country which has a weak bargaining strength or which is facing balance of payments difficulties.

For example, the USA and several other industrially advanced countries (with abundant capital resources) are interested in weakening competition from imported goods from labour-surplus countries like India.

They are insisting that imports should be totally banned (or at least severely restricted) if they are produced by “exploited” or “sweat” labour (that is, by labour which is paid at rates lower than those in rich countries like the USA) or by child labour.

The flaws in this logic are quite easy to see. Wage rates are expected to be lower in a labour-surplus economy. And it is this fact which makes its labour-intensive products competitive.

Similarly, it is a fact that child labour is extensively used in India in the manufacture of carpets and other handicrafts.

It is also admitted that it would be better if these children, instead of working, were attending schools. But that happy situation can be attained only if our economy grows and income levels of the parents rise. Till then, if these children are prevented from taking up jobs, their families would become still poorer.

- Problems of Foreign Exchange:

These days, currencies are on “paper standard”.’ And historically, some leading currencies of the world (the most prominent being the US dollar) are being held as “foreign exchange reserves” by countries of the world for financing their trade and other international economic transactions.

Moreover, a rapid expansion in these transactions has added to the need for ever-increasing volumes of foreign exchange reserves.