Marketing may be defined as the collection of activities undertaken by the firm to relate profitability to its market. Marketing in the modem context goes beyond its immediate role as a process through which exchange of goods and services takes place and is viewed as an integral part of the total socioeconomic system which provides the framework within which activities take place.

Marketing may be defined as the collection of activities undertaken by the firm to relate profitability to its market. Marketing in the modem context goes beyond its immediate role as a process through which exchange of goods and services takes place and is viewed as an integral part of the total socioeconomic system which provides the framework within which activities take place. It is, therefore, imperative to understand the total structure of the society in order to gain an insight into the true character of the marketing system.

Marketing involves the performance of operation in a business system. It includes those operations that determine existing and obtained changes in the market. It also includes those operations that influence existing and potential demand. It is concerned with all activities that are concerned with the physical distribution of goods and their exchange in the market place, including channel of selection, transportation, shipping, warehousing, storage, inventory control and so on and so forth.

Thus marketing covers a wide range of interrelated business activities that enlarge the role of a marketer from one of selling, what has been produced, to one of influencing, what is to be produced. The main concern of marketing is to identify and satisfy specific customer needs by means of specific products or services; wherein lies the key to profit.

The term marketing can be broadly described as:

(i) Micro-marketing

Micro-marketing may be described as the process of formulating and implementing certain strategies by a firm that ensures flow of need satisfying goods and services at a profit, Micro-marketing is responsible for effective performance of the strategies of product planning pricing, promoting and distributing.

(ii) Macro-marketing

Macro-marketing is concerned with how effectively a society uses its resources and how fairly it allocates its output of goods and services. Macro-marketing is responsible for effective performance of functions like information function, equalising and distribution function and centralised exchange function.

Marketing environment refers to external factors and forces that affect the company’s ability to develop and maintain successful transactions and relationships with its target consumers.

Role of Marketing

Marketing innovations and technical changes now occur at an ever increasing rate in the field of FMCGs and electronics. Industrial products, however, in the industrial field are often a case of changing technology. The needs of consumers undergo a change.

New competition is coming from all directions—from global competitors eager to grow sales in new markets; from online competitors seeking cost-efficient ways to expand distribution; from private label and store-brands designed to low price alternatives, and brand extensions from strong megabrands leveraging their strengths to move into new categories. The global market pattern is made possible by the development of international transportation and communication system and liberalisation policies adopted by different countries at present.

Modem marketing has much deviated from the past and undergone radical changes in recent years. Marketing is a managerial function, primarily economic, consisting of activities like research into markets, demand forecasting, product planning, pricing, distribution and advertising, organised into a system of interdependencies and directed at yielding profits to the enterprises, providing satisfaction to the consumers and indirectly benefiting society at large.

Marketing has to play an important role. It is the most important multiplier and an effective engine of economic development. It mobilises latent economic energy and thus is the creator of small business. Marketing is the developer of the standard of product and services.

Besides, economic integration is made possible through proper distribution of the product. Distribution is the key area in modem marketing. The importance of distribution will become clearer when it is realised that most of the marketing failures are in fact distribution failures.

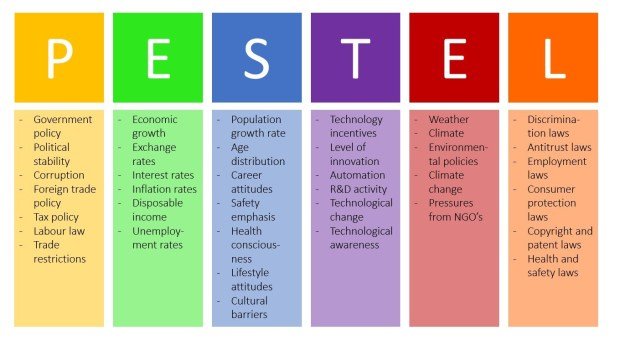

Shortage of raw materials, escalating cost of energy, high level of pollution, changing role of government in environmental protection are some of the dangers that the present world is facing on environmental forces. Advances in technology are an important uncontrollable environment for marketers. Technological progress creates new avenues of opportunity and also poses threat for individual companies.

Certain types of technological developments by competitors may result in loss of markets.

Markets are efficient when the price of a good or service attracts exactly as much demand as the market can currently supply. The chief function of the market is to adjust prices to accommodate fluctuations in supply and demand in order to achieve allocative efficiency. An economic system in which goods and services are exchanged by market functions is called a market economy.

Current Concepts in Marketing

(i) Social Marketing

Philip Kotler has defined his social marketing concept as a management orientation aimed at generating customer satisfaction and long-run consumer and public welfare and as the key to satisfying organizational goals and responsibilities. Social marketing is the application of marketing theories and techniques to social situations.

(ii) Over Marketing

It constitutes the striving by a firm to generate increased sales while neglecting quality control, production efficiency and cash flow management.

(iii) Meta Marketing

It is the synthesis of all managerial, traditional, scientific, social and historical foundations of marketing and includes specialization on the inter-relationships of mental and physical processes to supplement the facts and empirical observations of marketing practice.

(iv) De-marketing

It is a situation which may come about as a result of temporary shortages occasioned by short-term excess demand for a company’s products. De-marketing is that aspect of marketing that deals with discouraging customers in general or a certain class of customers in particular on either a temporary or a permanent basis.

(v) Remarketing

It takes the form of finding or creating new uses of users for an existing product. Actually, marketing is a method by which new type of satisfactions are created for old products. But de-marketing is the opposite of the marketing concept, while at the same time remarketing creates new satisfaction for the consumer.

(vi) Relationship Marketing

It is the process of building long-term trusting win-win relationship with customers, distributors, dealers and suppliers. It also promises and delivers high quality efficient services and fair prices to the other party over time. It requires building mutual trust and rapport between the business and its customers.

(vii) Controversial Marketing

Negative demand is common to many products. Controversial marketing is that type of planned marketing which aims at causing demand to rise from negative to positive, and eventually equals the positive supply level. Here the marketer has to take necessary measures to counter it.

(viii) Stimulational Marketing

Stimulational marketing is that type of marketing which transforms a no demand situation into one of positive demand by connecting a product to some existing need through change of environment or spread of knowledge about it.

(ix) Developmental Marketing

Developmental marketing relates to innovation. The marketing has to bring out altogether new useful products or improving existing products so as to have new uses.

Growth of Marketing

In the growth of marketing, the marketing era began virtually after the Second World War. Producers found that consumers in general, particularly in the advanced countries of the west, had their basic needs more or less satisfied. They had become more selective about their purchases. It was a challenging situation.

Marketing came to the rescue by helping to find out what goods were needed the most, who needed them most, in what quantities they were needed and so on. Manufacturing organizations set up separate departments of marketing which provided guidelines to the plants about the right kind of products, right quantities and right prices.

During this period, special importance came to be attached to markets and consumers. At present, marketing starts with assessing the needs of the consumers and then tries to meet them via product planning, pricing and other ways.

Functions of Marketing

- Gathering and Analyzing Market Information

Gathering and analyzing market information is an important function of marketing. Under it, an effort is made to understand the consumer thoroughly in the following ways:

- What do the consumers want?

- In what quantity?

- At what price?

- When do they want (it)?

- What kind of advertisement do they like?

- Where do they want (it)?

What kind of distribution system do they like? All the relevant information about the consumer is collected and analysed. On the basis of this analysis an effort is made to find out as to which product has the best opportunities in the market.

- Marketing Planning

In order to achieve the objectives of an organization with regard to its marketing, the marketeer chalks out his marketing plan. For example, a company has a 25% market share of a particular product.

The company wants to raise it to 40%. In order to achieve this objective the marketer has to prepare a plan in respect of the level of production and promotion efforts. It will also be decided as to who will do what, when and how. To do this is known as marketing planning.

- Product Designing and Development

Product designing plays an important role in product selling. The company whose product is better and attractively designed sells more than the product of a company whose design happens to be weak and unattractive.

In this way, it can be said that the possession of a special design affords a company to a competitive advantage. It is important to remember that it is not sufficient to prepare a design in respect of a product, but it is more important to develop it continuously.

- Standardization and Grading

Standardization refers to determining of standard regarding size, quality, design, weight, colour, raw material to be used, etc., in respect of a particular product. By doing so, it is ascertained that the given product will have some peculiarities.

This way, sale is made possible on the basis of samples. Mostly, it is the practice that the traders look at the samples and place purchase order for a large quantity of the product concerned. The basis of it is that goods supplied conform to the same standard as shown in the sample.

Products having the same characteristics (or standard) are placed in a given category or grade. This placing is called grading. For example, a company produces commodity – X, having three grades, namely A’. ‘B’ and ‘C’, representing three levels of quality; best, medium and ordinary respectively.

Customers who want best quality will be shown ‘A’ grade product. This way, the customer will have no doubt in his mind that a low grade product has been palmed off to him. Grading, therefore, makes sale-purchase easy. Grading process is mostly used in case of agricultural products like food grains, cotton, tobacco, apples, mangoes, etc.

- Packaging and Labelling

Packaging aims at avoiding breakage, damage, destruction, etc., of the goods during transit and storage. Packaging facilitates handling, lifting, conveying of the goods. Many a time, customers demand goods in different quantities. It necessitates special packaging. Packing material includes bottles, canister, plastic bags, tin or wooden boxes, jute bags etc.

Label is a slip which is found on the product itself or on the package providing all the information regarding the product and its producer. This can either be in the form of a cover or a seal.

For example, the name of the medicine on its bottle along with the manufacturer’s name, the formula used for making the medicine, date of manufacturing, expiry date, batch no., price etc., are printed on the slip thereby giving all the information regarding the medicine to the consumer. The slip carrying all these is details called Label and the process of preparing it as Labelling.

- Branding

Every producer/seller wants that his product should have special identity in the market. In order to realise his wish he has to give a name to his product which has to be distinct from other competitors.

Giving of distinct name to one’s product is called branding. Thus, the objective of branding is to show that the products of a given company are different from that of the competitors, so that it has its own identity.

For instance, if a company wants to popularise its commodity – X under the name of “777” (triple seven) then its brand will be called “777”. It is possible that another company is selling a similar commodity under AAA (Triple ‘A’) brand name.

Under these circumstances, both the companies will succeed in establishing a distinct identity of their products in the market. When a brand is not registered under the trade Mark Act, 1999, it becomes a Trade Mark.

- Customer Support Service

Customer is the king of market. Therefore, it is one of the chief functions of marketer to offer every possible help to the customers. A marketer offers primarily the following services to the customers:

- After-sales-services

- Handling customers’ complaints

- Technical services

- Credit facilities

- Maintenance services

Helping the customer in this way offers him satisfaction and in today’s competitive age customer’s satisfaction happens to be the top-most priority. This encourages a customer’s attachment to a particular product and he starts buying that product time and again.

- Pricing of Products

It is the most important function of a marketing manager to fix price of a product. The price of a product is affected by its cost, rate of profit, price of competing product, policy of the government, etc. The price of a product should be fixed in a manner that it should not appear to be too high and at the same time it should earn enough profit for the organization.

- Promotion

Promotion means informing the consumers about the products of the company and encouraging them to buy these products. There are four methods of promotion:

- Advertising

- Personal selling

- Sales promotion

- Publicity

Every decision taken by the marketer in this respect affects the sales. These decisions are taken keeping in view the budget of the company.

- Physical Distribution

Under this function of marketing the decision about carrying things from the place of production to the place of consumption is taken into account. To accomplish this task, decision about four factors are taken. They are:

- Transportation

- Inventory

- Warehousing

- Order Processing

Physical distribution, by taking things, at the right place and at the right time creates time and place utility.

- Transportation

Production, sale and consumption-all the three activities need not be at one place. Had it been so, transportation of goods for physical distribution would have become irrelevant. But generally it is not possible. Production is carried out at one place, sale at another place and consumption at yet another place.

Transport facility is needed for the produced goods to reach the hands of consumers. So the enterprise must have an easy access to means of transportation.

Mostly we see on the road side’s private vehicles belonging to Pepsi, Coca Cola, LML, Britannia, etc. These private carriers are the living examples of transportation function of marketing. Place utility is thus created by transportation activity.

- Storage or Warehousing

There is a time-lag between the purchase or production of goods and their sale. It is very essential to store the goods at a safe place during this time-interval. Godowns are used for this purpose. Keeping of goods in godowns till the same are sold is called storage.

For the marketing manager storage is an important function. Any negligence on his part may damage the entire stock. Time utility is thus created by storage activity.

by

by