National Securities Clearing Corporation Limited (NSCCL) is a wholly-owned subsidiary of the National Stock Exchange (NSE) of India. It was established to ensure smooth clearing and settlement of trades executed on the NSE. NSCCL acts as a central counterparty (CCP), guaranteeing settlement and reducing counterparty risk by novating trades. It manages margins, monitors risks, and ensures timely transfer of funds and securities, maintaining integrity in the capital markets.

Objectives of NSCCL:

NSCCL’s primary objective is to ensure the guaranteed settlement of all trades executed on the National Stock Exchange. It acts as a counterparty to both buyers and sellers, reducing counterparty risk and enhancing market confidence. By providing this guarantee, NSCCL ensures that trade failures due to non-performance by either party are avoided, thereby maintaining the integrity of the clearing and settlement system.

A core objective of NSCCL is the implementation of a robust risk management framework to protect the capital markets. This includes real-time monitoring of trading limits, maintenance of margins, and stringent position limits to prevent market manipulation or defaults. NSCCL ensures that financial risks are minimized and systemic risks are avoided, ensuring that market disruptions do not spread across participants.

NSCCL seeks to enhance operational efficiency in clearing and settlement processes by adopting automated, transparent, and timely systems. Its objective is to reduce the time lag between trade execution and settlement, reduce manual intervention, and facilitate paperless, straight-through processing. This efficiency reduces cost and increases the speed of transactions for all market participants.

Promoting transparency is an essential objective of NSCCL. It maintains a centralized clearing system where the details of trades, margins, and obligations are accessible to clearing members. This openness helps participants understand their settlement responsibilities, monitor their risks, and stay compliant, which enhances trust in the financial markets.

Another key objective is to maintain financial stability in the capital market ecosystem. By acting as a central counterparty and managing default risk, NSCCL ensures that trade failures do not have a cascading effect on other trades. This contributes to investor confidence and market sustainability during periods of volatility.

NSCCL aims to integrate India’s clearing and settlement systems with international best practices. By aligning with global standards, such as those prescribed by IOSCO and BIS, it ensures competitiveness and builds investor confidence, especially among global institutional investors. This integration makes Indian markets more accessible and trustworthy to the global financial community.

NSCCL’s objective extends beyond clearing; it also focuses on developing the Indian financial markets. By introducing innovative clearing systems, derivatives clearing, and risk control measures, it supports the growth of various market segments. It actively participates in policy advocacy and technological upgrades that promote an efficient and modern securities infrastructure.

Functions of NSCCL:

NSCCL acts as a central counterparty to trades executed on the NSE by novating each transaction. This means it becomes the legal counterparty to both sides of a trade — buyer to every seller and seller to every buyer. Novation ensures the anonymity of trading participants and reduces the risk of counterparty default, making trade settlement more secure and reliable.

One of the core functions of NSCCL is the efficient clearing and settlement of securities and funds. It determines settlement obligations, coordinates the exchange of cash and securities, and ensures that both are transferred to respective parties within the stipulated time frame. This process is crucial for maintaining the liquidity and orderliness of the market.

To safeguard against defaults, NSCCL collects margins such as Initial Margin, Mark-to-Market Margin, and Exposure Margin from trading members. These margins are computed on real-time positions and monitored continuously. By holding these margins, NSCCL ensures that members have sufficient collateral to meet their obligations, thereby reducing credit and settlement risks.

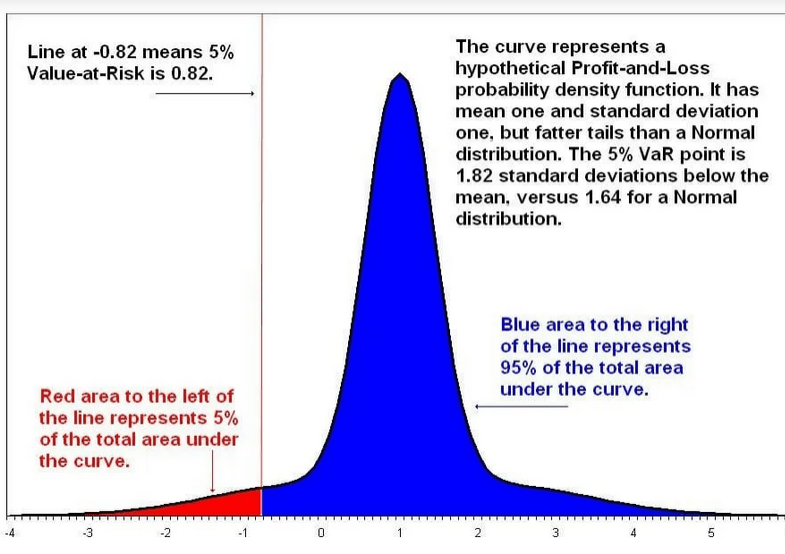

NSCCL continuously monitors the exposure and creditworthiness of its clearing members through a risk management system. It uses sophisticated tools to measure and control risks, including Value at Risk (VaR) models, position limits, and stress testing. This ongoing surveillance enables timely intervention to mitigate potential defaults and systemic risk.

In case a member defaults on settlement obligations, NSCCL has well-defined default procedures. It can invoke the default fund, liquidate collateral, and ensure that the trades are settled without disrupting the market. This function is critical in maintaining trust in the market and preventing contagion effects.

NSCCL maintains detailed records of all transactions, margins, settlement obligations, and member compliance. It provides regular reports and audit trails to regulators, members, and other stakeholders. This documentation ensures transparency, regulatory compliance, and enables audits, dispute resolution, and financial analysis.

NSCCL constantly updates its systems to incorporate technological innovations such as algorithmic trading interfaces, real-time data feeds, and API-based systems. It promotes automated trading, clearing, and reporting mechanisms to streamline operations. This function enhances market accessibility, speed, and accuracy, benefiting all participants in the capital markets.

by

by