Strategic Evaluation and Control

by

by Strategic Evaluation & control is as important as strategy formulation. It sheds light on the efficiency and effectiveness of the comprehensive plans in achieving the desired results.

Role of organizational systems in strategic evaluation & control: Strategic evaluation operates in the context of various organizational systems. An organization develops various systems which help in integrating various parts of the organization. The major organizational systems are: information system, planning system, motivation system, appraisal system and development system. All these organizational systems play their role in strategic evaluation and control. Some of these systems are closely and directly related and some are indirectly related to evaluation and control. In connection with the role of organizational systems in strategic evaluation & control, the following systems may be important.

-

Information System

Evaluation and control action is guided by adequate information from the beginning to the end. Management information and management control systems are closely interrelated which the information system is designed on the basis of control system. Every manager in the organization must have adequate information about his performance, standards and how he is contributing to the achievement of organizational objectives. There must be a system of information tailored to the specific management needs at every level, both in terms of adequacy and timeliness.

-

Planning System

Planning is the basis for control in the sense that it provides the entire spectrum on which control function is based. In fact, these two terms are often used together in the designation of the department which carries production planning, scheduling and routing. It emphasizes that there is a plan which directs the behavior and activities in the organization. Control measures these behavior and activities and suggests measures to remove deviation. Thus, there is a reciprocal relationship between planning and control.

-

Motivation System

Motivation system is not only related to evaluation and control system but to the entire organizational processes. Lack of motivation on the part of managers is a significant barrier in the process of evaluation and control. Since the basic objective of evaluation and control is to ensure that organizational objectives are achieved. Motivation plays a central role in this process. It energizes managers and other employees in the organization to perform better which is the key for organizational success.

-

Appraisal System

Appraisal or performance appraisal system involves systematic evaluation of the individual with regard to his performance on the job and his potential for development. While evaluating an individual, not only his performance is taken into consideration but also his abilities and potential for better performance. Thus, appraisal system provides feedback for control system about how individuals are performing.

-

Development System

Development system is concerned with developing personnel to perform better in their present positions and likely future positions that they are expected to occupy. Thus, development system aims at increasing organizational capability through people to achieve better results. These results become the basic for evaluation and control. Role of organizational systems in strategic evaluation should not be undermined.

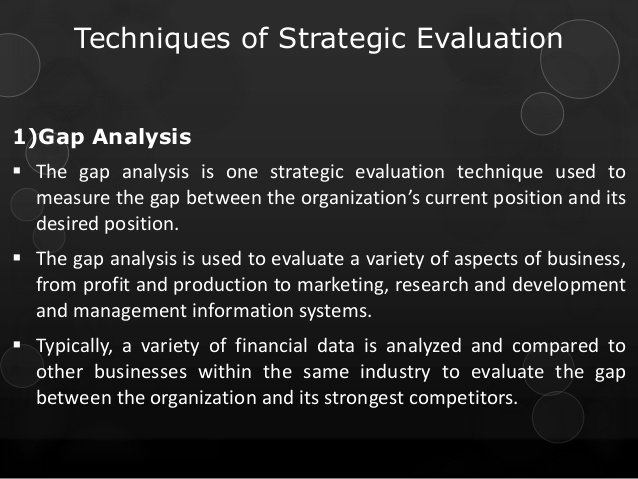

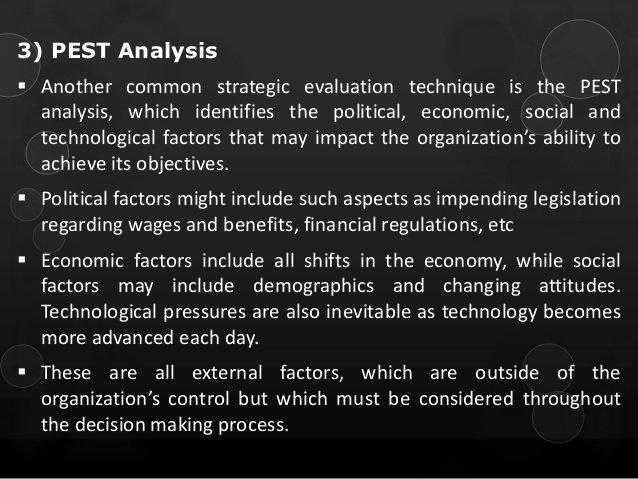

Techniques of strategic evaluation & control

Strategy evaluation and control is the sixth step in the strategic management process. As we have read that well executed strategy definitely ensures successful achievement of organizational goals and objectives. But changes internal and external environment of an organization may not allow the firm to achieve desired goals and objective. The environment changes may takes place at any stage of strategy implementation. Strategy evaluation and control done after measuring results shall not help in taking corrective action. It should be done in the early stage of strategy execution, to see whether the strategy is successfully implemented or not and to carryout mid-course corrections whenever necessary. Therefore strategists should systematically review, evaluate, and control the process of strategy implementation.