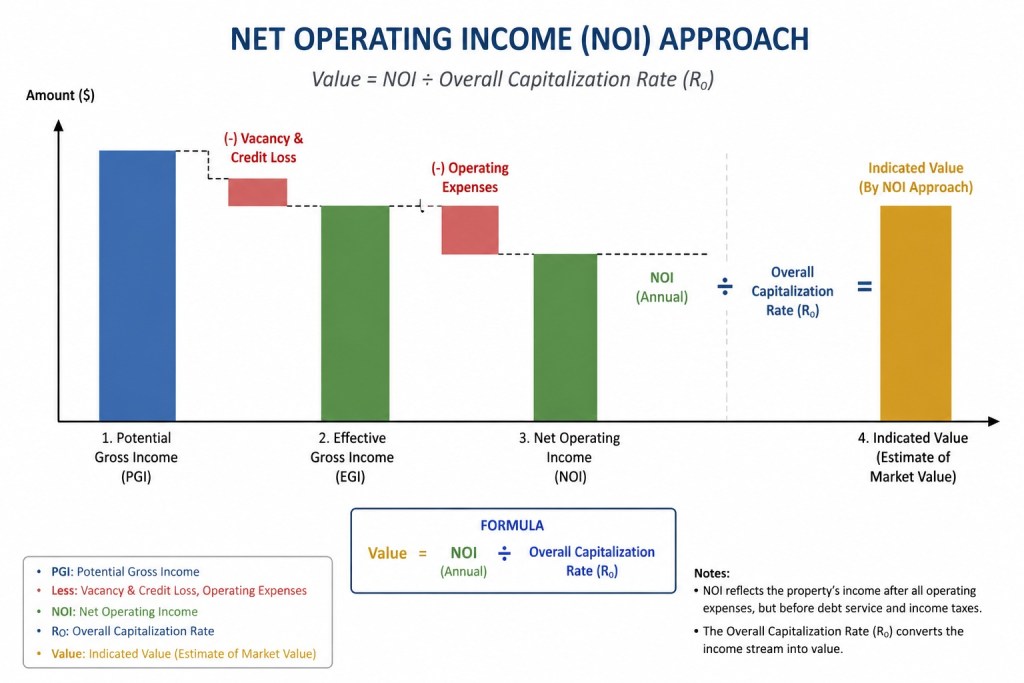

Net Operating Income (NOI) Approach is a traditional theory of capital structure developed by David Durand. This approach argues that the capital structure of a firm is irrelevant and does not affect the overall value of the firm or its weighted average cost of capital (WACC). According to the theory, changes in the proportion of debt and equity financing do not influence the total market value of the company.

The NOI Approach states that although debt is cheaper than equity, any increase in debt financing causes the cost of equity to rise proportionately because shareholders demand higher returns due to increased financial risk. As a result, the overall cost of capital remains constant regardless of the firm’s capital structure.

Definition of Net Operating Income (NOI) Approach

Net Operating Income Approach states that the value of a firm depends on its operating income and business risk, not on its capital structure. Therefore, changes in debt-equity proportions do not affect the firm’s total value or overall cost of capital.

Concept of NOI Approach

According to the NOI Approach:

Value of Firm (V)

V = EBIT / Ko

Where:

- V = Total Value of Firm

- EBIT = Earnings Before Interest and Taxes

- Ko = Overall Cost of Capital

Market Value of Equity (S)

S = V − D

Where:

- S = Market Value of Equity

- V = Total Value of Firm

- D = Market Value of Debt

Cost of Equity (Ke)

Ke = NI / S

Where:

- NI = Net Income Available to Equity Shareholders

- S = Market Value of Equity

Example of NOI Approach

Given

- EBIT = ₹3,00,000

- Debt = ₹5,00,000

- Cost of Debt (Kd) = 10%

- Overall Cost of Capital (Ko) = 12%

Step 1: Calculate Value of Firm

V = EBIT / Ko

V = ₹3,00,000 / 0.12

V = ₹25,00,000

Step 2: Calculate Market Value of Equity

S = V − D

S = ₹25,00,000 − ₹5,00,000

S = ₹20,00,000

Step 3: Calculate Interest

Interest = ₹5,00,000 × 10%

Interest = ₹50,000

Step 4: Calculate Net Income

NI = EBIT − Interest

NI = ₹3,00,000 − ₹50,000

NI = ₹2,50,000

Step 5: Calculate Cost of Equity

Ke = NI / S

Ke = ₹2,50,000 / ₹20,00,000

Ke = 12.5%

Answer

- Value of Firm = ₹25,00,000

- Market Value of Equity = ₹20,00,000

- Cost of Equity = 12.5%

- Overall Cost of Capital = 12% (Constant)

Features of Net Operating Income (NOI) Approach

- Capital Structure is Irrelevant

A key feature of the Net Operating Income (NOI) Approach is that capital structure does not affect the value of the firm. According to this theory, whether a company finances its operations through debt, equity, or a combination of both, the total value of the firm remains unchanged. Investors focus on the firm’s earning capacity and business risk rather than its financing pattern. Therefore, changes in leverage do not create additional value. This feature forms the foundation of the NOI Approach and distinguishes it from theories that consider capital structure relevant to firm valuation.

- Value of the Firm Depends on Operating Income

The NOI Approach states that the value of a firm is determined by its operating income, particularly Earnings Before Interest and Taxes (EBIT). The firm’s earning power and business performance are considered the primary factors influencing its market value. Financing decisions do not alter the company’s operating income; therefore, they do not affect firm value. A company with higher and stable operating income will generally have a higher valuation. This feature emphasizes that operational efficiency and profitability are more important than financing choices in determining the overall worth of a business.

- Overall Cost of Capital Remains Constant

According to the NOI Approach, the overall cost of capital (Ko) remains constant regardless of changes in the debt-equity ratio. Even if a company increases its use of debt financing, the weighted average cost of capital does not decline. This occurs because any benefit obtained from cheaper debt is exactly offset by an increase in the cost of equity. As a result, the firm’s overall capitalization rate remains unchanged. This feature supports the idea that leverage does not influence firm value and that financing decisions have no effect on the company’s total cost of capital.

- Cost of Equity Increases with Leverage

The NOI Approach recognizes that higher debt financing increases financial risk for equity shareholders. As leverage rises, shareholders face greater uncertainty because debt holders have a prior claim on earnings. To compensate for this additional risk, equity investors demand a higher rate of return. Therefore, the cost of equity increases proportionately with leverage. This increase offsets the advantage of lower-cost debt financing. This feature reflects the relationship between financial risk and shareholder expectations and explains why the overall cost of capital remains constant despite changes in capital structure.

- Cost of Debt Remains Constant

Another important feature of the NOI Approach is the assumption that the cost of debt remains constant at all levels of leverage. Lenders are assumed to charge the same interest rate regardless of the amount of debt used by the company. Although this assumption may not be realistic in practice, it simplifies the analysis of capital structure. Since the cost of debt remains unchanged, the entire adjustment to increased leverage occurs through a rise in the cost of equity. This feature helps explain the mechanism through which the overall cost of capital remains constant.

- No Optimum Capital Structure Exists

Under the NOI Approach, there is no optimum capital structure because changes in debt and equity proportions do not affect firm value or overall cost of capital. Since leverage neither increases nor decreases the total value of the firm, no particular financing mix is considered superior. Managers cannot create additional value simply by altering the debt-equity ratio. This feature contrasts sharply with the Net Income Approach, which suggests that an optimum capital structure exists. The NOI theory therefore supports the view that financing decisions are irrelevant to maximizing firm value.

- Focuses on Business Risk Rather Than Financial Risk

The NOI Approach emphasizes business risk as the primary determinant of firm value. Business risk arises from the nature of the company’s operations, industry conditions, competition, and economic environment. While financial risk increases with leverage, the theory assumes that investors adjust their required returns accordingly. As a result, firm value continues to depend mainly on operating performance rather than financing decisions. This feature highlights the importance of managerial efficiency, profitability, and operational stability in determining market value, reinforcing the theory’s focus on the earning power of the firm.

- Supports Capital Structure Irrelevance Theory

A significant feature of the NOI Approach is its support for the concept of capital structure irrelevance. The theory argues that investors cannot gain additional wealth merely because a firm changes its financing pattern. Since the overall cost of capital remains constant and firm value is unaffected by leverage, capital structure decisions do not influence shareholder wealth. This idea later influenced modern financial theories, particularly the Modigliani-Miller propositions. As a result, the NOI Approach occupies an important place in financial management by providing a theoretical foundation for understanding the relationship between leverage and firm value.

Assumptions of the NOI Approach

1. Overall Capitalization Rate Remains Constant

The NOI Approach assumes that the overall capitalization rate, also known as the overall cost of capital or Ko, remains constant regardless of the degree of leverage employed by the firm. This means that no matter how the company structures its financing between debt and equity, the market always values the firm by capitalizing its net operating income at the same fixed rate. This constant capitalization rate implies that the total market value of the firm is determined solely by its earning power and operating income, not by its financing decisions, making capital structure completely irrelevant to overall firm valuation under this theoretical framework.

2. Cost of Equity Rises with Increasing Leverage

Unlike the NI Approach, the NOI Approach explicitly recognizes that equity shareholders are rational investors who perceive and respond to increasing financial risk as leverage rises. As the proportion of debt in the capital structure increases, the fixed interest obligations create greater earnings volatility and higher financial risk for equity holders. Consequently, shareholders demand a progressively higher rate of return to compensate for this increased risk, causing the cost of equity to rise proportionally with leverage. This rise in equity cost precisely offsets the benefit of using cheaper debt, ensuring that the overall weighted average cost of capital remains unchanged regardless of the debt-equity mix.

3. Cost of Debt Remains Constant

The NOI Approach assumes that the cost of debt remains constant at all levels of leverage, reflecting the idea that debt holders maintain a prior claim on the firm’s assets and earnings, shielding them from the financial risk of moderate leverage levels. Since debt holders enjoy priority in repayment and their returns are fixed through contractual interest obligations, they do not demand higher returns as the company takes on additional debt within reasonable limits. This constant cost of debt, combined with the rising cost of equity, ensures that the overall capitalization rate remains stable as the firm shifts its financing mix between debt and equity.

4. No Corporate Taxes

Similar to the NI Approach, the basic NOI Approach assumes a taxation-free environment, meaning that corporate income taxes do not exist and therefore the tax-deductibility benefit of interest payments on debt is not considered. In a world without taxes, debt loses its additional advantage of generating a tax shield, making the theoretical argument for capital structure irrelevance more straightforward and internally consistent. This assumption eliminates a significant real-world advantage of debt financing, allowing the model to demonstrate that the only cost benefit of debt, its lower rate, is entirely offset by the rise in equity cost, leaving total firm value and overall cost of capital unaffected by leverage.

5. The Market Values the Firm as a Whole

A fundamental assumption of the NOI Approach is that investors and the market value the firm as a total entity based on its overall earning power and net operating income stream, rather than separately valuing the individual components of its capital structure. This holistic valuation perspective means that the split of total firm value between debt and equity is considered inconsequential, as the market focuses on the overall cash generating ability of the business rather than how those cash flows are divided among different capital providers. Consequently, any restructuring of the financing mix merely redistributes the existing total value between debt holders and shareholders without changing the aggregate firm value.

6. Investors Have Homogeneous Expectations

The NOI Approach assumes that all investors share identical expectations regarding the firm’s future net operating income, overall risk profile, and growth prospects. This homogeneity of expectations ensures that all market participants agree on the appropriate overall capitalization rate to apply when valuing the firm’s earnings stream. Without this assumption, different investors might assign different values to the same firm based on varying perceptions of risk arising from leverage, potentially disrupting the clean theoretical conclusion that capital structure is irrelevant. Homogeneous expectations simplify the model by ensuring consistent market-wide agreement on firm valuation, regardless of the debt-equity composition chosen by management.

Capital Structure under the NOI Approach:

1. Capital Structure is Irrelevant to Firm Value

The most fundamental proposition of the NOI Approach regarding capital structure is that the total market value of a firm is completely independent of its financing mix, making capital structure decisions entirely irrelevant to overall firm valuation. According to this approach, the market values the firm solely based on its net operating income and the overall capitalization rate, both of which remain unaffected by how the firm chooses to divide its financing between debt and equity. Whether a firm uses no debt or substantial leverage, its total market value remains unchanged. Any attempt to increase firm value by substituting equity with cheaper debt is self-defeating, as the resulting rise in equity cost exactly neutralizes the apparent benefit of cheaper debt financing.

2. No Optimal Capital Structure Exists

Unlike the NI Approach, which identifies maximum leverage as the optimal point, the NOI Approach concludes that no single optimal capital structure exists for any firm. Since the overall cost of capital remains constant at every possible debt-equity ratio, there is no particular financing mix that minimizes WACC or maximizes firm value. Every capital structure is equally good or equally bad from a valuation perspective, as changing the proportion of debt and equity merely redistributes value between debt holders and shareholders without altering total firm value. This conclusion challenges the traditional notion that finance managers can enhance firm value through careful capital structure engineering, suggesting that managerial effort is better focused on improving operating performance rather than financing decisions.

3. Cost of Equity Adjusts to Keep WACC Constant

A central mechanism underlying the NOI Approach’s capital structure conclusion is that the cost of equity automatically adjusts upward as leverage increases, precisely offsetting the benefit of incorporating cheaper debt into the capital structure. As the firm takes on more debt, equity shareholders perceive greater financial risk arising from fixed interest obligations and the increased probability of earnings volatility. Rational investors respond by demanding a higher required rate of return on their equity investment to compensate for this additional risk. This systematic rise in equity cost ensures that the weighted average of debt and equity costs, that is WACC, remains constant at all leverage levels, preventing any capital structure change from altering the firm’s overall cost of capital.

4. Market Value of the Firm is Determined by NOI

Under the NOI Approach, the total market value of the firm is determined exclusively by capitalizing the firm’s net operating income at the constant overall capitalization rate, completely independent of the capital structure chosen. The formula used is Total Market Value of Firm = Net Operating Income divided by Overall Capitalization Rate. Since both net operating income and the capitalization rate are unaffected by leverage decisions, the resulting total firm value remains fixed regardless of the debt-equity mix employed. The individual values of debt and equity components may change as the financing mix changes, but their combined total always remains the same, confirming the irrelevance of capital structure to aggregate firm valuation under this approach.

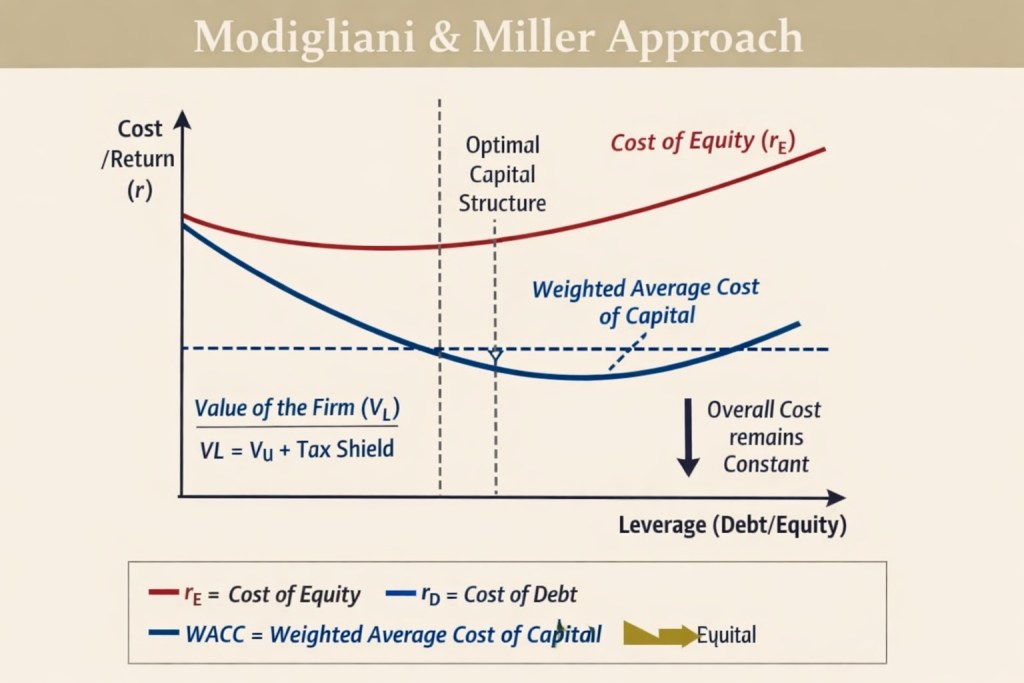

5. Graphical Representation of Capital Structure Irrelevance

When the NOI Approach is represented graphically with the degree of leverage on the horizontal axis, the overall cost of capital curve appears as a perfectly horizontal straight line at a constant level, indicating that WACC does not change regardless of how much debt the firm uses. Simultaneously, the cost of equity curve slopes upward as leverage increases, reflecting the rising financial risk premium demanded by shareholders, while the cost of debt curve remains flat. The horizontal WACC line powerfully illustrates the core conclusion of the NOI Approach, that no capital structure decision can move the overall cost of capital up or down, reinforcing the irrelevance proposition through clear visual representation.

6. Practical Implications of the NOI Approach

Although the NOI Approach concludes that capital structure is theoretically irrelevant, it carries important practical implications for financial managers. It suggests that firms should not waste resources or management attention attempting to find a mythical optimal debt-equity ratio, as no such ratio genuinely exists under this framework. Instead, management should focus on decisions that directly improve operating performance, revenue generation, cost efficiency, and investment returns, since these are the true drivers of firm value. The approach also highlights the importance of investor rationality and market efficiency, reminding managers that sophisticated investors will see through superficial capital restructuring exercises and price the firm based on its fundamental earning power rather than its financing arrangement.

Advantages of the NOI Approach

- Simplicity and Practical Applicability

The NOI Approach offers remarkable conceptual simplicity, making it highly practical for financial managers. It posits that the overall cost of capital (WACC) and firm value remain constant regardless of the debt-equity mix, assuming no taxes and perfect markets. This straightforward framework allows managers to focus on operational efficiency rather than getting entangled in complex capital structure optimization calculations. Unlike the Net Income Approach, which requires intricate computations of changing equity costs, the NOI model provides a clean, easy-to-understand baseline. Practitioners can use this as a starting point for strategic decisions without excessive mathematical modeling, saving both time and analytical resources.

- Emphasis on Operating Efficiency Over Financing

A fundamental advantage of the NOI Approach is its strategic shift in management focus toward operational excellence rather than financial engineering. Since the theory asserts that firm value depends solely on net operating income and business risk—not on how that income is financed—it encourages managers to concentrate on improving production, sales, marketing, and cost control. This operational orientation fosters sustainable competitive advantages through better products, efficient processes, and market expansion. By de-emphasizing the debt-equity mix, the approach prevents management from wasting energy on fruitless arbitrage between debt and equity, redirecting attention toward genuine value-creating activities.

- Recognition of Market Imperfections (Arbitrage Process)

The NOI Approach uniquely validates the existence of investor-level arbitrage as a equilibrating mechanism in financial markets. According to this theory, if two identical firms with different capital structures trade at different valuations, rational investors will engage in homemade leverage—borrowing personally to purchase equity of the unlevered firm and selling the levered firm’s shares. This arbitrage activity quickly corrects any mispricing, ensuring that market values converge. This built-in self-correction mechanism gives the approach strong intuitive appeal, as it acknowledges that sophisticated investors will not pay a premium for what they can replicate personally, thereby maintaining market efficiency.

- Logical Treatment of Equity Capitalization Rate

The NOI Approach provides a logical, intuitive explanation for the behavior of the equity capitalization rate (Ke). As a firm increases its debt proportion, the financial risk borne by equity shareholders rises proportionately. Consequently, the required rate of return on equity (Ke) increases linearly to exactly offset the benefits of cheaper debt. This elegant inverse relationship ensures that the weighted average cost of capital (WACC) remains perfectly unchanged. This treatment recognizes shareholder psychology realistically—investors rationally demand higher compensation for bearing greater residual risk, and this natural market reaction neutralizes any apparent advantage from substituting debt for equity.

- Foundation for Modern Capital Structure Theories

Despite its restrictive assumptions, the NOI Approach serves as the intellectual bedrock for contemporary capital structure theories, most notably Modigliani-Miller (M-M) Proposition I. By establishing that leverage does not affect firm value in a no-tax world, it paved the way for further research incorporating taxes, bankruptcy costs, and asymmetric information. Students and practitioners who master the NOI framework gain a critical conceptual lens for understanding trade-off theory, pecking order theory, and signaling models. Without this foundational understanding, modern financial management becomes disjointed; the NOI Approach offers the essential starting point for all advanced capital structure deliberations.

- Encourages Rational Capital Budgeting Decisions

Since the NOI Approach asserts a constant WACC irrespective of leverage, it allows financial managers to evaluate investment projects using a stable, unchanging discount rate. This consistency eliminates the complex, iterative calculations required to adjust hurdle rates for varying debt proportions across different projects. Managers can therefore focus purely on the project’s operating cash flows and risk characteristics rather than worrying about how the project will be financed. This separation of investment and financing decisions (the famous “separation theorem”) streamlines capital budgeting, reduces computational errors, and ensures that projects are evaluated on their fundamental economic merits alone.

- Neutralizes Unproductive Tax Arbitrage Arguments

In its pure form (assuming no corporate taxes), the NOI Approach effectively neutralizes the temptation for firms to engage in unproductive tax-driven arbitrage through excessive leverage. By demonstrating that the value of the firm remains invariant to the debt-equity mix, it discourages management from taking on dangerous debt levels simply to exploit interest tax shields. This conservative implication protects firms from over-leveraging, which in the real world leads to financial distress, agency conflicts, and bankruptcy. Thus, the approach implicitly advocates for prudent, moderate leverage policies rather than aggressive, high-risk financial structures that could destabilize the enterprise during economic downturns.

Limitations of the NOI Approach

- Assumes Constant Overall Cost of Capital

The NOI approach assumes that the overall cost of capital remains constant regardless of changes in the capital structure. In reality, increasing debt raises the financial risk of the company, causing both the cost of debt and the cost of equity to change. Investors demand higher returns as risk increases. Therefore, the assumption of a constant overall cost of capital is unrealistic and does not reflect actual market conditions. This limitation reduces the practical applicability of the NOI approach in making financing decisions for modern business organizations.

The NOI approach assumes that increasing debt does not affect the firm’s financial risk. However, excessive borrowing increases fixed interest obligations and the possibility of financial distress. As debt rises, shareholders face greater risk because earnings become more uncertain. Consequently, investors demand higher returns on equity. By ignoring the impact of financial risk, the NOI approach fails to represent the real relationship between leverage and the cost of capital. This makes the approach less suitable for practical financial management and capital structure planning.

- Unrealistic Assumption of Perfect Capital Market

The NOI approach is based on the assumption of a perfect capital market where there are no taxes, transaction costs, or information differences among investors. In practice, capital markets are imperfect due to taxes, brokerage charges, government regulations, and unequal access to information. These market imperfections influence financing decisions and affect the cost of capital. Since the assumptions of the NOI approach rarely exist in the real business environment, its conclusions may not accurately represent actual corporate financing situations.

- Ignores Tax Benefits of Debt

The NOI approach assumes that debt financing does not provide any tax advantage. In reality, interest paid on debt is generally tax deductible, reducing the company’s taxable income and lowering the effective cost of debt. This tax shield makes debt financing more attractive than equity in many situations. By ignoring the tax benefits associated with borrowing, the NOI approach underestimates the value of debt financing and provides an incomplete explanation of capital structure decisions in modern financial management.

- Assumes Cost of Debt Remains Constant

According to the NOI approach, the cost of debt remains unchanged regardless of the amount of borrowing. In practice, lenders charge higher interest rates when a company’s debt level increases because the risk of default becomes greater. As financial leverage rises, the cost of debt usually increases rather than remaining constant. This unrealistic assumption weakens the practical usefulness of the NOI approach and limits its ability to explain the actual behaviour of borrowing costs in competitive financial markets.

- Difficult to Apply in Practice

The assumptions of the NOI approach are highly theoretical and difficult to apply in real business situations. Market conditions, investor expectations, interest rates, taxes, and business risks continuously change over time. As a result, the cost of debt, cost of equity, and overall cost of capital rarely remain constant. Finance managers must consider these changing factors while making capital structure decisions. Therefore, the NOI approach provides only a simplified theoretical framework and has limited practical application in financial management.

- Overlooks Investor Behaviour

The NOI approach assumes that investors are rational and react uniformly to changes in the company’s capital structure. However, investor decisions are influenced by factors such as market sentiment, expectations, risk perception, and economic conditions. Different investors may value the same company differently based on their individual preferences and investment objectives. By overlooking these behavioural factors, the NOI approach fails to explain how investor attitudes can influence the market value of the firm and its financing decisions.

- Limited Practical Acceptance

The NOI approach has limited acceptance in modern financial management because its assumptions do not match real business conditions. Financial decisions today are influenced by taxes, bankruptcy costs, agency costs, market imperfections, and changing investor expectations. Modern capital structure theories provide more realistic explanations by considering these practical factors. Although the NOI approach is important for understanding the theoretical relationship between capital structure and firm value, it is mainly useful for academic study rather than practical financial decision making.

by

by