Goodwill, Introductions, Meaning, Definitions, Needs, Origins, Circumstances, Factors, Methods

by

by Goodwill is an intangible asset representing the value of a business’s reputation, brand image, customer loyalty, efficient management, favourable location, and other advantages that enable it to earn higher profits compared to other firms in the same industry.

Unlike tangible assets such as buildings, machinery, or stock, goodwill cannot be physically seen or touched, but it significantly contributes to the earning potential of the business. It reflects the premium value that an acquiring company is willing to pay over and above the fair market value of the net assets of the acquired business.

In accounting terms, goodwill is recognised when a business is purchased for a price higher than the value of its net assets. The difference between the purchase price and the net asset value is recorded as goodwill in the books of the buyer.

Example:

If the net assets of a business are worth ₹50,00,000 and it is purchased for ₹60,00,000, the excess ₹10,00,000 is goodwill.

Goodwill can be:

-

Purchased Goodwill: Arises when paid for during the acquisition.

-

Self-generated Goodwill: Arises due to the firm’s efforts over time but is usually not recorded in the books as per accounting standards.

Need for Valuation of Goodwill

Valuation of goodwill becomes necessary in several business and corporate accounting situations. The major circumstances are explained below, each highlighting why goodwill must be quantified and adjusted.

- Admission of a Partner

When a new partner is admitted into a partnership, the existing partners may be sacrificing a portion of their future profits. Goodwill is valued to compensate the old partners for this sacrifice. The incoming partner pays his share of goodwill in cash or capital, which is distributed among existing partners in their sacrificing ratio. Valuation ensures fairness, prevents disputes, and reflects the firm’s enhanced earning capacity at the time of admission.

- Retirement of a Partner

At the time of retirement, a partner is entitled to his share of goodwill because he helped build the firm’s reputation and profit-earning ability. Goodwill valuation is necessary to determine the retiring partner’s due share. The remaining partners compensate him in cash or adjust capital accounts accordingly. Without proper valuation, the retiring partner may be deprived of the benefits arising from the goodwill generated during his association with the firm.

- Death of a Partner

In case of the death of a partner, goodwill must be valued to calculate the amount payable to the legal representatives of the deceased partner. Since goodwill represents future benefits, the deceased partner’s share up to the date of death must be settled fairly. Valuation helps in arriving at a just settlement, protects the interests of the deceased partner’s family, and ensures continuity of business without financial conflicts.

- Change in Profit-Sharing Ratio

Whenever partners decide to change their profit-sharing ratio, some partners may gain while others may sacrifice their share of future profits. Goodwill valuation becomes essential to compensate the sacrificing partners by the gaining partners. This adjustment maintains equity among partners and reflects the realignment of future earning rights. Valuation avoids misunderstandings and ensures that changes in ownership rights are supported by proper financial adjustments.

- Sale of Business

When a business is sold as a going concern, goodwill valuation is necessary to determine the true sale price. The buyer pays not only for tangible assets but also for the established reputation, customer base, and earning potential of the business. Goodwill valuation ensures that the seller receives fair compensation for the intangible advantages transferred to the buyer and helps in accurate determination of purchase consideration.

- Amalgamation or Absorption of Companies

In cases of amalgamation or absorption, goodwill valuation is required to calculate purchase consideration and to record goodwill or capital reserve in the books of the transferee company. If the purchase price exceeds the fair value of net assets, goodwill arises. Valuation ensures compliance with accounting standards, enables accurate financial reporting, and reflects the true cost of acquiring another company’s business advantages.

- Conversion of Partnership Firm into a Company

When a partnership firm is converted into a company, goodwill must be valued to determine the purchase consideration payable by the company. The company acquires the firm’s reputation and earning capacity along with its assets. Proper valuation ensures that partners receive shares or consideration proportionate to the goodwill contributed by the firm and that the company’s balance sheet reflects a realistic business value.

- Determination of True Value of Business

Goodwill valuation is necessary to ascertain the true value of a business beyond its tangible assets. It reflects factors such as market position, brand image, customer loyalty, and managerial efficiency. This valuation is useful for investors, financial institutions, and management while making investment, merger, or expansion decisions. It provides a realistic picture of the firm’s overall worth and future profit potential.

Origins of Goodwill

Goodwill originates from various internal and external factors that enable a business to earn profits in excess of the normal rate. These sources collectively build the reputation and value of the enterprise over time. The main origins of goodwill are explained below.

- Reputation of the Business

The long-standing reputation of a business is one of the most important sources of goodwill. Firms that have operated successfully for many years build trust among customers, suppliers, and investors. This reputation ensures customer loyalty and repeat sales, even in the presence of competition. A reputed firm can charge premium prices and still retain customers. Such confidence and public image, developed over time, create an intangible advantage that directly contributes to the generation of goodwill.

- Efficient Management

Efficient, experienced, and visionary management plays a crucial role in the creation of goodwill. Capable managers ensure optimum utilization of resources, cost control, innovation, and strategic decision-making. Sound management policies result in higher productivity, better employee relations, and sustained profitability. When a firm consistently earns above-normal profits due to managerial efficiency, it enhances its market value, thereby giving rise to goodwill at the time of valuation or acquisition.

- Location Advantage

A favorable business location significantly contributes to goodwill. Firms located in prime areas, such as commercial hubs or places with easy access to raw materials and markets, enjoy operational and competitive advantages. For example, retail stores in busy marketplaces or factories near ports and transport facilities incur lower costs and attract more customers. Such locational benefits enable higher earnings and long-term stability, resulting in the creation of goodwill.

- Monopoly or Favorable Market Position

Goodwill may arise due to monopoly power or a strong market position. When a firm faces limited or no competition, it can control prices, maintain stable demand, and earn consistent profits. Even without legal monopoly, a dominant market share, brand leadership, or exclusive rights can reduce competitive pressure. These advantages allow the firm to generate excess profits over normal returns, which form the basis for the valuation of goodwill.

- Quality of Products and Services

Superior quality of products or services is a major source of goodwill. Firms that maintain consistent quality standards gain customer satisfaction and brand loyalty. High-quality goods reduce complaints, returns, and marketing costs while improving brand image. Customers often prefer such products even at higher prices. This ability to attract and retain customers through quality leads to sustained earnings, which ultimately results in the creation of goodwill.

- Skilled and Loyal Workforce

A skilled, trained, and loyal workforce contributes significantly to goodwill. Experienced employees improve efficiency, reduce wastage, and enhance innovation. Strong employer–employee relationships also reduce labor turnover and industrial disputes. Such stability ensures smooth operations and continuous productivity. Since human resources are not recorded as assets in the balance sheet, their contribution to future profits appears indirectly in the form of goodwill.

- Favorable Contracts and Legal Rights

Goodwill may also arise from favorable long-term contracts, licenses, patents, trademarks, or exclusive distribution rights. These legal advantages provide income security and competitive protection. For example, patented technology or exclusive supply agreements ensure steady demand and reduced competition. As these benefits enable the firm to earn higher profits over a longer period, they contribute significantly to the valuation of goodwill.

- Marketing Ability and Brand Image

Strong marketing strategies, effective advertising, and a well-established brand image create goodwill. Firms with popular brand names enjoy customer recognition and loyalty, which increases sales volume and market penetration. Brand equity allows businesses to introduce new products easily and withstand competitive pressure. This marketing strength leads to higher future earnings and forms an important origin of goodwill in corporate accounting.

Circumstances When Goodwill is Valued

Valuation of goodwill becomes necessary under several business situations, particularly when ownership or profit-sharing arrangements change. The key circumstances are:

- Sale of Business

When a business is sold as a going concern, the purchase price often includes an amount for goodwill. The buyer is willing to pay for the benefits of an established reputation, customer base, and other advantages that will generate profits in the future. In such cases, goodwill is valued to determine the total consideration.

-

Admission of a New Partner

When a new partner joins a partnership firm, they get the right to share in the future profits of the business. Since the existing partners have worked to build the firm’s reputation and profit potential, the incoming partner usually compensates them for their share of the goodwill. The valuation ensures fairness in determining the amount payable.

-

Retirement or Death of a Partner

When a partner retires or dies, they are entitled to receive their share of the goodwill, as they helped build the business’s reputation. Valuation ensures the outgoing partner (or their legal heirs) is fairly compensated for their contribution.

-

Amalgamation of Companies

When two companies merge, the valuation of goodwill helps in deciding the share exchange ratio or purchase consideration. This ensures both sets of shareholders are treated fairly based on the relative worth of their companies, including intangible assets like goodwill.

-

Change in Profit-Sharing Ratio

If partners in a firm decide to change their existing profit-sharing arrangement, the partner gaining a higher share compensates the partner losing a share of profits. Goodwill valuation helps determine this compensation amount.

-

Conversion of a Partnership into a Company

When a partnership is converted into a company, goodwill is valued to determine the consideration payable to the partners, especially when the business is transferred as a going concern.

-

Court Cases or Tax Purposes

In legal disputes, divorce settlements, inheritance cases, or tax assessments, goodwill valuation may be required to determine the fair market value of a business.

- Liquidation

Even during liquidation, goodwill may have a residual value if the brand name, customer contracts, or other intangible advantages can be sold separately.

Factors Affecting the Valuation of Goodwill:

The value of goodwill is not fixed—it varies depending on several qualitative and quantitative factors. These include:

-

Nature of Business

The type of business has a major influence on goodwill. A business with stable demand, essential products, and a long-term customer base (e.g., FMCG, healthcare) will generally have higher goodwill compared to one operating in a volatile or seasonal market.

-

Location of Business

A business located in a prime area with high footfall (e.g., near markets, busy streets, or transportation hubs) can attract more customers without significant advertising. Such businesses have higher goodwill because their location provides a competitive advantage.

-

Reputation of the Business

A well-established reputation for quality, service, and reliability increases customer trust and loyalty, resulting in repeat business and higher goodwill. Negative publicity or poor customer service can reduce goodwill.

-

Efficiency of Management

A capable and experienced management team improves productivity, reduces costs, and maintains consistent quality—factors that enhance profitability and goodwill. Poor management decisions, on the other hand, can damage goodwill quickly.

-

Quality of Products or Services

High-quality products and services ensure customer satisfaction and retention, leading to strong word-of-mouth promotion and higher goodwill. Businesses known for substandard products may have low or even negative goodwill.

-

Market Conditions

Favourable industry trends, low competition, and economic stability enhance goodwill, while recession, intense competition, or market saturation can reduce it.

-

Access to Resources

Easy access to skilled labour, raw materials, finance, and advanced technology can increase a firm’s efficiency and profitability, thereby boosting goodwill.

-

Risk Involved

Businesses with lower business risk (e.g., stable cash flows, diversified products) command higher goodwill. High-risk ventures (e.g., speculative trading) have lower goodwill valuations.

-

Long-Term Contracts and Relationships

Securing long-term contracts with key customers or suppliers provides revenue stability and increases goodwill.

-

Brand Value and Intellectual Property

Well-known trademarks, patents, and copyrights add to goodwill because they provide a unique competitive advantage.

-

Monopoly or Favourable Agreements

Legal monopolies or government concessions can significantly enhance goodwill since they reduce competition and guarantee revenue streams.

-

Synergy Benefits in Mergers

In the case of amalgamation or acquisition, expected cost savings, market expansion, or combined operational efficiency can increase the goodwill valuation.

Importance of Valuation of Goodwill:

The process of valuing goodwill is essential for:

-

Ensuring fairness in partner compensation.

-

Determining the correct purchase consideration in mergers/acquisitions.

-

Presenting an accurate financial position in legal cases.

-

Facilitating negotiations during business sale.

-

Ensuring compliance with accounting standards (AS 26 in India, IFRS 3 globally).

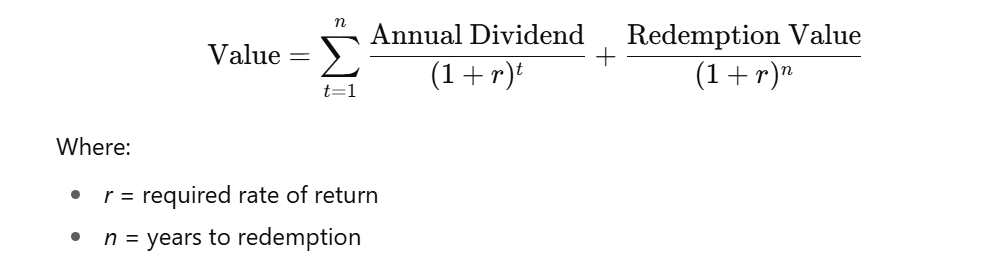

Methods of Valuation of Goodwill:

The value of goodwill can be determined using various methods, depending on the nature of the business, purpose of valuation, and availability of data. The main methods are:

1. Average Profit Method

Goodwill is valued by multiplying the average maintainable profits by a certain number of years’ purchase.

-

Formula:

Goodwill = Average Profit × Number of Years’ Purchase

-

Steps:

-

Determine past profits.

-

Adjust for abnormal items.

-

Calculate average profit.

-

Multiply by agreed years’ purchase (e.g., 3, 4, or 5 years).

-

-

Types:

-

Simple Average Profit Method – Uses arithmetic average.

-

Weighted Average Profit Method – Gives higher weight to recent profits to reflect current earning capacity.

-

2. Super Profit Method

Goodwill is calculated based on the “super profits” — the excess of average profit over the normal profit (which is based on the normal rate of return).

-

Formula:

Goodwill = Super Profit × Number of Years’ Purchase

Where:

Super Profit = Average Profit − Normal Profit

Normal Profit = Capital Employed × Normal Rate of Return (NRR)

-

Features:

-

Highlights the business’s earning capacity above industry standards.

-

Suitable when profits are higher than normal industry returns.

-

3. Capitalization Method

This method converts maintainable profits into total capital value, then deducts the actual capital employed to get goodwill.

a) Capitalization of Average Profits

-

Formula:

Goodwill = [Average Profit × 100 / NRR] − Capital Employed

-

Indicates how much more the business is worth compared to its actual capital invested.

b) Capitalization of Super Profits

-

Formula:

Goodwill = [Super Profit × 100] / NRR

-

Focuses purely on capitalizing the extra profit above the normal level.

4. Annuity Method

Super profits are treated as an annuity receivable for a certain period, and goodwill is calculated as the present value of that annuity.

-

Formula:

Goodwill = Super Profit × Present Value of ₹1 for n years at i%

-

Use: Reflects the time value of money, making it suitable when super profits are expected only for a limited period.

5. Market Value Method

Used for companies whose shares are actively traded in the stock market. Goodwill is indirectly reflected in the market value of shares above their book value.

-

Formula:

Goodwill = (Market Value per Share − Net Asset Value per Share) × Number of Shares

-

Use: Common for valuing goodwill in publicly listed companies.

6. Purchase Consideration Method (Residual Method)

Goodwill is the difference between the purchase consideration paid for acquiring a business and the net assets acquired.

-

Formula:

Goodwill = Purchase Consideration − Net Assets Acquired

-

Use: Applicable in mergers, acquisitions, and business takeovers.

7. Rule of Thumb Method

Goodwill is valued as a fixed proportion (e.g., 1 year’s purchase) of turnover, gross profit, or some other financial measure.

-

Use: Quick, but not precise; often used in small business sales (e.g., retail shops).