Pricing refers to the process of determining the value of a product or service in monetary terms. It is a critical aspect of marketing and business strategy, influencing demand, profitability, and market positioning. Effective pricing considers various factors, including production costs, competition, market demand, and perceived value. Businesses can adopt different pricing strategies, such as cost-plus pricing, value-based pricing, or penetration pricing, to achieve their objectives.

Objectives of Pricing:

One of the primary objectives of pricing is to generate revenue for the business. By setting prices that reflect the value of the product or service, companies can ensure that they are covering costs and making a profit. Pricing strategies should align with revenue goals, whether for short-term gains or long-term sustainability.

Businesses often aim for market penetration through competitive pricing strategies. Lower prices can attract customers and increase market share, especially for new products entering a competitive landscape. This approach helps establish a foothold in the market, encouraging customer loyalty and fostering brand recognition.

Pricing is a critical lever for maximizing profits. By strategically adjusting prices based on demand, cost structure, and competitive landscape, businesses can enhance their profit margins. This may involve premium pricing for high-value products or competitive pricing to drive volume and reduce costs.

Effective pricing can differentiate a product from competitors, positioning it as either a premium offering or a budget-friendly alternative. Understanding competitors’ pricing strategies allows businesses to craft their pricing in a way that highlights unique features or benefits, enhancing their market position.

The price of a product often influences customer perception and brand image. A well-calibrated pricing strategy can convey quality, exclusivity, or affordability. For instance, luxury brands may adopt high pricing to reinforce their premium image, while discount retailers focus on value to attract cost-conscious consumers.

Another objective of pricing is to ensure that all costs associated with a product or service are recovered. This includes fixed costs (like overhead and salaries) and variable costs (like raw materials and production). Businesses must carefully analyze their cost structure to set prices that adequately cover expenses and support financial health.

Pricing strategies can also be used to stabilize markets and reduce price wars. By establishing a consistent pricing approach, companies can help prevent excessive competition that may lead to eroded profits. Collaborative pricing strategies or price signaling can help maintain market stability.

Pricing can be used as a tool to manage demand for a product or service. By implementing dynamic pricing strategies, companies can adjust prices based on real-time demand fluctuations. For example, airline ticket prices often vary based on seasonality and occupancy rates, helping to optimize revenue.

- Promotion and Sales Strategy

Pricing objectives are often tied to promotional activities and sales strategies. Temporary discounts, bundled pricing, or special offers can be employed to stimulate sales during slow periods or to clear inventory. These strategies enhance customer engagement and drive purchases.

Differentiated pricing strategies can be employed to cater to various market segments. Businesses can use price discrimination, charging different prices for the same product based on customer characteristics or buying behavior. This approach allows companies to maximize revenue from each segment by capturing consumer surplus.

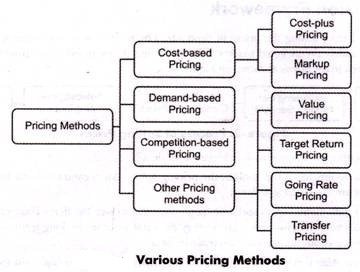

Strategies of Pricing:

1. Cost-Based Pricing

Cost-based pricing involves setting prices based on the costs of producing a product or service, with a markup added for profit. This strategy ensures that a business covers its expenses and achieves a desired level of profitability. It’s straightforward and easy to calculate but may not always consider market conditions or customer demand.

- Example: A manufacturer calculates the production cost of a product and adds a 20% markup to set the retail price.

2. Penetration Pricing

Penetration pricing is used when a company aims to enter a new market or increase its market share quickly. This strategy involves setting low prices initially to attract customers, generate interest, and build brand recognition. After gaining a sufficient market share, the company may gradually raise prices.

- Example: A new streaming service offering a low subscription fee to attract users, with plans to raise the price once customer loyalty is established.

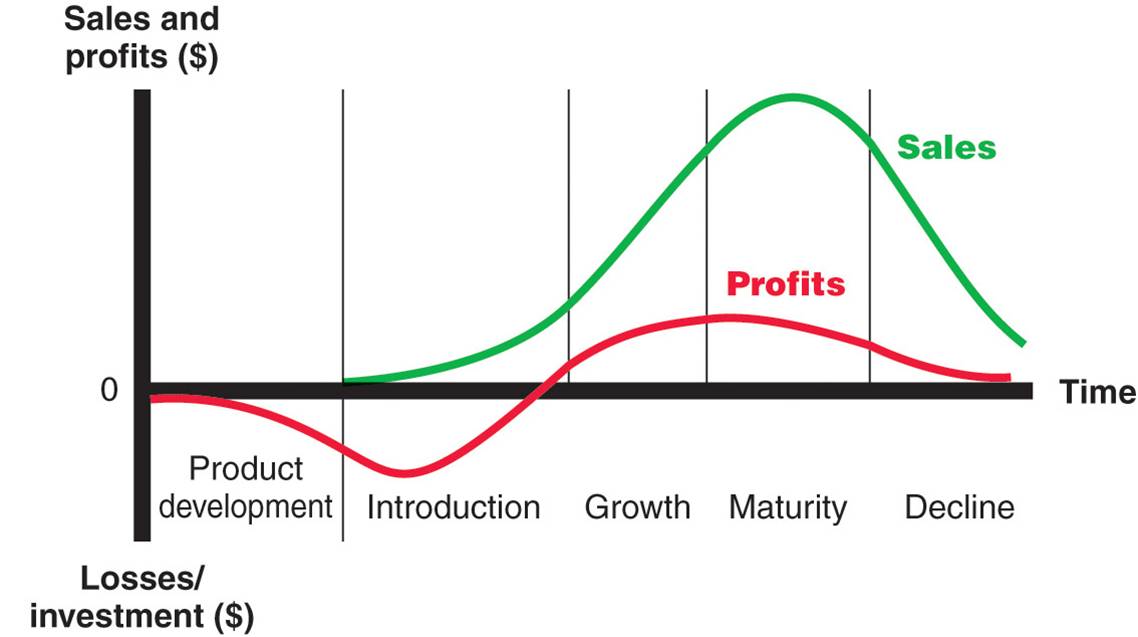

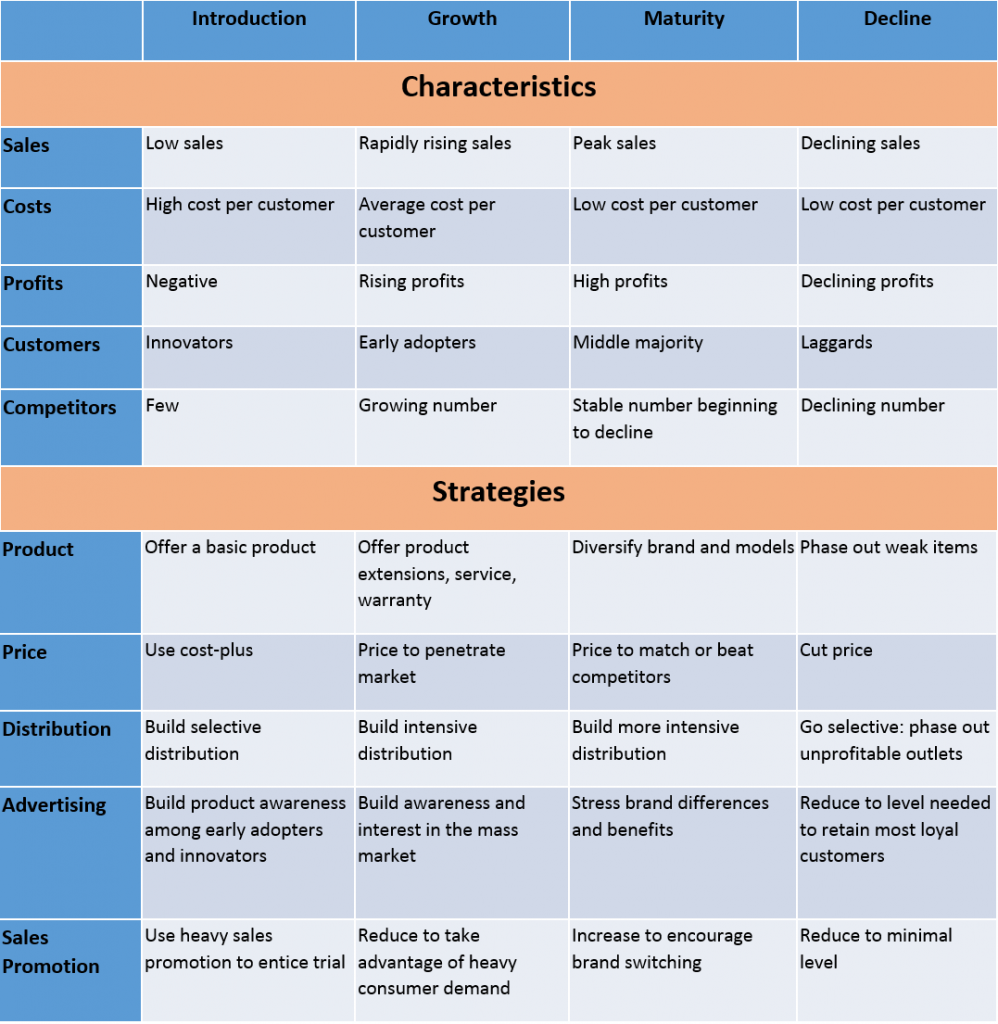

3. Price Skimming

Price skimming is a strategy where businesses set high prices for a new or innovative product, targeting customers willing to pay a premium. Over time, prices are gradually lowered to attract more price-sensitive customers. This approach allows businesses to maximize profit from early adopters before reducing prices to capture a broader market.

- Example: Technology companies like Apple often use skimming pricing for new smartphone launches.

4. Psychological Pricing

Psychological pricing takes advantage of consumer psychology to influence purchasing decisions. This strategy often uses pricing techniques like “charm pricing” (e.g., $9.99 instead of $10) to create the perception of a better deal. It can also involve premium pricing to position a product as high-quality or exclusive.

- Example: A retailer prices items at $19.99 instead of $20 to make the price appear more attractive.

5. Dynamic Pricing

Dynamic pricing involves adjusting prices in real time based on factors like demand, competition, or seasonality. This strategy is commonly used in industries like airlines, hospitality, and ride-sharing services, where prices fluctuate depending on market conditions.

- Example: Uber uses dynamic pricing (surge pricing) to increase fares during peak times or in areas with high demand.

6. Bundle Pricing

Bundle pricing is the strategy of offering multiple products or services together at a lower price than if they were purchased individually. This encourages customers to buy more items while perceiving a better value. It is often used in both consumer goods and services industries.

- Example: Fast food chains offer meal combos, such as a burger, fries, and drink, at a discounted rate when bought together.

7. Value-Based Pricing

Value-based pricing is centered around setting prices based on the perceived value to the customer rather than the cost of production. This strategy requires businesses to understand their customers’ needs and how much they are willing to pay for the product’s benefits, features, or unique qualities.

- Example: High-end cosmetics companies use value-based pricing by positioning their products as luxury items with added benefits like superior ingredients or packaging.

8. Competitive Pricing

Competitive pricing involves setting prices in line with competitors in the market. This strategy can either match, beat, or slightly exceed the competition’s prices based on a company’s positioning. It works best in markets with many similar products where price competition is high.

- Example: Retailers often price similar products at competitive rates to ensure they remain attractive to consumers and avoid losing business to cheaper alternatives.

Nature of Pricing:

1. Strategic Tool

Pricing is a strategic tool that plays a pivotal role in a company’s market positioning and overall marketing mix. The price of a product or service affects how customers perceive the quality, value, and brand identity. By adjusting pricing, businesses can influence demand, increase market share, and attract specific customer segments.

- Example: Premium pricing strategies can create a perception of high quality, while competitive pricing might be used to attract price-sensitive customers.

2. Dynamic

Pricing is not static; it is subject to change based on various internal and external factors, including demand, competition, economic conditions, and costs. Businesses often adjust their prices to respond to market fluctuations, consumer behavior, and competitor pricing strategies. Dynamic pricing helps companies remain competitive and optimize profits in a changing environment.

- Example: Airlines often adjust ticket prices based on demand, time of booking, and availability.

3. Reflects Costs and Profit Margins

The price of a product or service is often based on the costs involved in its production, distribution, and marketing. Pricing must not only cover these costs but also ensure a profit margin for the company. Understanding fixed and variable costs is essential for setting an appropriate price that ensures profitability.

- Example: A retailer pricing a product will factor in the cost of manufacturing, shipping, and overheads while adding a profit margin.

4. Customer-Oriented

The price must align with the perceived value of the product or service from the customer’s perspective. A customer-oriented pricing strategy considers factors such as the target market’s buying behavior, their willingness to pay, and the product’s perceived benefits. This approach helps in setting a price that customers find fair and reasonable.

- Example: Apple’s pricing of its smartphones is based on consumer perception of innovation and quality.

5. Competitive

Pricing is heavily influenced by competition. Companies need to analyze competitors’ pricing strategies to set a price that is competitive in the market. Pricing too high may drive customers to competitors, while pricing too low could lead to a loss of perceived value. Competitive pricing ensures that businesses maintain market relevance and profitability.

- Example: Supermarkets often adjust their prices based on competitor promotions.

6. Legal and Ethical Considerations

Pricing must adhere to legal regulations and ethical standards. In many countries, laws prevent unfair pricing practices such as price-fixing, price discrimination, and deceptive pricing. Businesses must ensure that their pricing strategies do not exploit consumers or violate antitrust laws.

- Example: The Indian government regulates the maximum retail price (MRP) of essential goods to protect consumers.

Scope of Pricing

1. Cost-Based Pricing

The scope of pricing starts with understanding the costs involved in producing and delivering a product or service. Pricing must cover both fixed and variable costs, while ensuring a reasonable profit margin. Cost-based pricing is often the starting point for setting prices. This approach involves determining the total cost of production and adding a desired profit margin.

- Example: A manufacturer of a gadget may calculate its production cost and add a 20% markup to set the retail price.

2. Market-Based Pricing

Market-based pricing involves setting prices according to market demand, competition, and customer expectations. Businesses must consider external factors, including competitor pricing, market trends, and consumer demand, when setting their prices. By analyzing the market and understanding customer perceptions of value, companies can adjust their pricing strategies accordingly.

- Example: A clothing retailer might adjust prices based on seasonal demand or competitive pricing in the market.

3. Psychological Pricing

The scope of pricing also includes psychological pricing, which uses pricing tactics to influence customer behavior. It involves setting prices that create an emotional impact, such as $9.99 instead of $10, or using prestige pricing to indicate luxury and exclusivity. These strategies are designed to appeal to the customer’s emotions and perception of value.

- Example: A luxury brand may set prices at higher levels to create a perception of quality and exclusivity.

4. Penetration Pricing

In markets where companies aim to gain market share quickly, penetration pricing is used. This strategy involves setting a low price initially to attract customers and build brand awareness. Once the market share increases, the business may gradually raise prices. This approach is especially useful in new market entries or highly competitive industries.

- Example: A new streaming service may offer low subscription prices to attract customers before increasing the rates.

5. Skimming Pricing

Skimming pricing strategy is often used for new, innovative products. Here, businesses set high initial prices, targeting customers who are willing to pay a premium for the latest product or service. Over time, as demand decreases or competition increases, the price is gradually reduced. This helps businesses maximize profits in the early stages of a product’s lifecycle.

- Example: Technology companies often launch new smartphones at a high price before reducing them after a few months.

6. Discount and Promotional Pricing

Discounts and promotions are an integral part of the scope of pricing, especially in retail and e-commerce. Offering discounts, seasonal sales, or limited-time promotions can stimulate demand, clear out inventory, and attract new customers. This strategy helps businesses manage inventory and improve sales volumes during specific periods.

- Example: A retailer offering 30% off during a holiday sale to boost sales.

7. Dynamic Pricing

Dynamic pricing is an advanced pricing strategy that involves adjusting prices in real-time based on demand, supply, or other external factors. This type of pricing is particularly common in industries like airlines, hospitality, and ride-sharing services, where prices fluctuate according to demand and availability.

- Example: Airlines adjust ticket prices based on factors such as the time of booking and available seats.

Challenges of Pricing:

Market conditions, including competition, consumer demand, and economic fluctuations, can change rapidly. Businesses must continually assess these dynamics to set appropriate prices, making it challenging to maintain consistent pricing strategies. Unexpected shifts, such as economic downturns or new entrants in the market, can disrupt established pricing models.

Prices must reflect the costs associated with producing and delivering a product or service. However, fluctuating costs of raw materials, labor, and logistics can complicate pricing strategies. Businesses must frequently adjust their pricing to maintain profitability without alienating customers who may be sensitive to price increases.

Understanding how consumers perceive value is crucial for effective pricing. If prices are set too high, customers may perceive the product as overpriced; if too low, it may be viewed as low-quality. Striking the right balance between perceived value and price is a persistent challenge.

Competitive pricing is essential to attract and retain customers, but it can lead to price wars, eroding profit margins. Businesses must carefully analyze competitors’ pricing strategies and find ways to differentiate their offerings without engaging in destructive price competition.

Different market segments exhibit varying levels of price sensitivity. Determining how sensitive customers are to price changes can be complex, especially in diverse markets. Businesses need to use segmentation strategies to tailor pricing to different consumer groups effectively.

Pricing can be influenced by government regulations and industry standards, especially in highly regulated sectors like pharmaceuticals, utilities, and telecommunications. Businesses must navigate these constraints while ensuring compliance and maintaining competitive pricing.

Consumer psychology plays a significant role in pricing. Strategies like charm pricing (e.g., setting prices at $9.99 instead of $10) can influence purchasing decisions, but businesses must understand the psychological impact of pricing and how it relates to brand positioning.

- Global Pricing Strategies

For companies operating in multiple countries, establishing a global pricing strategy can be particularly challenging. Factors like currency fluctuations, local market conditions, and cultural differences affect pricing decisions and require a nuanced approach.

- Technology and Data Analytics

While technology provides tools for data-driven pricing strategies, it also introduces complexity. Businesses must effectively leverage analytics to monitor pricing performance and make informed decisions, requiring investment in technology and expertise.

Factors Influencing Pricing

The fundamental factor influencing pricing is the cost incurred in producing goods or services. This includes direct costs (materials, labor) and indirect costs (overheads). Businesses typically set prices to cover these costs while ensuring a profit margin. Understanding the total cost structure helps in determining the minimum price point necessary for sustainability.

The level of consumer demand for a product or service significantly influences pricing. When demand is high, businesses may set higher prices due to increased willingness to pay. Conversely, when demand is low, prices may need to be reduced to stimulate sales. Market research helps identify demand elasticity and assists in forecasting how changes in price can affect sales volume.

The pricing strategies of competitors play a critical role in determining a company’s pricing. Businesses must analyze competitor pricing to ensure their offerings are competitively positioned. This may involve setting prices lower to attract price-sensitive customers or higher if offering superior value or differentiation.

- Customer Perception and Value

Customer perception of value is pivotal in pricing decisions. Pricing should reflect the perceived value of the product or service in the eyes of consumers. Factors influencing this perception include brand reputation, product quality, and the benefits offered. Effective communication of value can justify higher prices and enhance consumer willingness to pay.

Broader economic factors, such as inflation, interest rates, and economic growth, impact pricing decisions. In an inflationary environment, businesses may need to raise prices to maintain profit margins. Economic downturns may necessitate price reductions to retain customers facing tighter budgets.

- Regulatory and Legal Factors

Government regulations, industry standards, and legal considerations can influence pricing. Certain industries may have pricing regulations to protect consumers, prevent price gouging, or maintain fair competition. Companies must stay compliant with these regulations while formulating their pricing strategies.

The choice of distribution channels affects pricing due to varying costs associated with each channel. Direct sales may allow for lower prices, while intermediaries (wholesalers, retailers) can add markup to prices. Understanding the entire distribution strategy helps in setting appropriate end-user prices.

The overall marketing strategy and objectives of a business also influence pricing. For example, a company aiming to penetrate the market may adopt penetration pricing, setting low prices to attract customers quickly. Alternatively, a company focusing on premium positioning may implement skimming pricing to maximize revenue from early adopters.

Like this:

Like Loading...

by

by