Accounting Information Systems (AIS) is a specialized branch of accounting that combines traditional accounting practices with modern information technology to process, manage, and analyze financial data. It refers to a structured framework of people, procedures, and technology designed to collect, record, store, and communicate accounting information for decision-making purposes. An AIS helps organizations ensure accurate financial reporting, effective internal control, and efficient operations.

The system integrates both manual and computerized processes to transform raw financial data into meaningful information. With advancements in technology, most organizations now rely heavily on computerized AIS that involve databases, enterprise resource planning (ERP) systems, and cloud-based solutions. These systems improve the speed, accuracy, and reliability of financial data handling while minimizing human errors.

AIS serves multiple stakeholders such as managers, investors, auditors, regulators, and employees by providing timely and relevant information. It plays a crucial role in strategic planning, budgeting, auditing, and compliance with legal requirements. Moreover, it strengthens internal controls by detecting fraud, ensuring data security, and safeguarding organizational assets.

Meaning of Accounting Information Systems

Accounting Information System (AIS) is a structured framework that combines accounting, management, and information technology to collect, record, process, and report financial and non-financial data for decision-making. It can be defined as a system of people, procedures, controls, databases, and technology designed to manage accounting information and ensure its accuracy, reliability, and relevance.

AIS captures financial transactions from various business activities, processes them into meaningful reports, and communicates this information to internal and external stakeholders such as managers, investors, auditors, and regulators. It integrates traditional accounting practices with advanced technologies like databases, enterprise systems, and cloud computing to enhance efficiency and effectiveness.

Functions of an Accounting Information System:

One of the primary functions of AIS is to collect financial and non-financial data from various business operations. Every transaction, whether sales, purchases, payroll, or expenses, needs to be recorded accurately. AIS ensures that this data is gathered systematically from different sources like invoices, receipts, and ledgers. This organized collection process prevents data loss, duplication, or errors. Accurate data collection forms the foundation for reliable reporting and effective decision-making in an organization.

- Recording of Transactions

After data is collected, AIS records it into appropriate accounting journals and ledgers. This step ensures that all transactions are chronologically documented and classified correctly, following accounting principles. Recording also creates an audit trail, allowing auditors and managers to verify the authenticity of financial data. By automating this process through software, AIS minimizes human errors, improves efficiency, and guarantees the completeness of financial records essential for reporting and compliance purposes.

AIS processes raw data into meaningful financial information by applying accounting rules, classifications, and calculations. This involves posting entries to ledgers, preparing trial balances, and adjusting accounts where necessary. Modern AIS uses computerized systems to automate calculations like depreciation, interest, and payroll. The processing step transforms unorganized raw transactions into structured financial data that can be further analyzed. This makes information more useful for management in planning, monitoring, and evaluating business operations.

A vital function of AIS is the secure storage of accounting information. Data must be maintained in databases or digital systems for easy retrieval, analysis, and reporting. Proper storage ensures that historical financial records are available for audits, comparisons, and future reference. AIS uses technologies like databases, cloud systems, and ERP solutions to organize and protect stored data. Secure storage safeguards sensitive financial information from unauthorized access, loss, or manipulation, thereby ensuring reliability and integrity.

AIS generates reports that provide insights into financial performance and business operations. These reports may include income statements, balance sheets, cash flow statements, budgets, and cost analyses. Reports are customized to meet the needs of different stakeholders, from managers requiring detailed internal reports to investors and regulators requiring summarized financial statements. By delivering timely and accurate reports, AIS supports compliance, enhances decision-making, and communicates essential financial information effectively to users across different levels of the organization.

- Internal Control and Security

Another critical function of AIS is implementing internal controls and security measures to protect financial data. AIS ensures authorization of transactions, segregation of duties, and monitoring of activities to prevent fraud and errors. It also uses passwords, encryption, and access restrictions to safeguard sensitive information. Strong internal control systems built into AIS enhance accuracy, reliability, and accountability in financial reporting. They also ensure compliance with legal requirements, thereby protecting both organizational assets and stakeholder interests.

- Support in Decision–Making

AIS plays a key role in managerial decision-making by providing accurate and timely information. It supports strategic planning, budgeting, forecasting, and performance evaluation by offering insights into costs, revenues, and profitability. Managers rely on AIS-generated data to allocate resources efficiently, identify risks, and assess growth opportunities. By integrating financial and non-financial data, AIS gives a holistic view of business performance. This function enables managers to take informed decisions that drive competitiveness and long-term organizational success.

- Compliance and Audit Support

AIS ensures that financial records and reports comply with statutory requirements, accounting standards, and taxation laws. It simplifies the preparation of documents needed for audits, regulatory reviews, and tax filings. AIS maintains accurate audit trails, making verification easier for auditors. Automated systems reduce the risk of non-compliance by updating regulatory changes. This function enhances transparency, builds trust among stakeholders, and ensures organizations meet legal obligations, thereby avoiding penalties and maintaining credibility in the business environment.

Need of an Accounting Information System:

- Accuracy in Financial Reporting

Organizations require AIS to ensure accuracy in financial reporting. Manual accounting processes often lead to human errors, misclassifications, or data loss. An AIS automates data entry, calculations, and reporting, minimizing mistakes and improving reliability. Accurate financial reports are essential for management decisions, investor confidence, and compliance with accounting standards. By reducing the margin of error, AIS provides precise and trustworthy financial information that reflects the true financial position of the business.

Businesses operate in fast-changing environments, and timely information is crucial for success. AIS provides real-time financial data that helps managers make quick and informed decisions. Whether it is evaluating cash flows, monitoring expenses, or planning investments, timely data supports effective decision-making. Without AIS, organizations may face delays in accessing updated information, leading to missed opportunities or poor strategies. Therefore, AIS is needed to provide up-to-date insights that align decisions with organizational goals.

- Compliance with Regulations

Compliance with accounting standards, taxation laws, and regulatory frameworks is a major need for businesses. AIS ensures that financial transactions are recorded according to Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). It also helps generate tax reports and statutory documents required by regulators. Automated compliance features reduce the risk of penalties, fines, or legal issues. By maintaining transparency and accountability, AIS helps businesses meet legal requirements and build credibility with stakeholders.

- Enhanced Internal Control

AIS is essential for strengthening internal control within organizations. It incorporates security measures such as access restrictions, authorization protocols, and audit trails that safeguard financial data. These controls reduce the chances of fraud, manipulation, or unauthorized transactions. Internal controls also ensure accountability by clearly defining user roles and responsibilities. Without an AIS, detecting irregularities or fraudulent activities becomes difficult. Thus, businesses need AIS to enhance security, maintain ethical practices, and protect organizational assets.

Manual accounting processes are time-consuming and costly, especially in large organizations with complex transactions. AIS reduces paperwork, automates repetitive tasks, and streamlines data management, saving both time and resources. By increasing efficiency, businesses can reallocate resources to other strategic activities. Additionally, quick access to information through AIS reduces the time needed for audits, reporting, and financial analysis. Hence, AIS is needed to improve operational efficiency, minimize costs, and maximize productivity in accounting functions.

- Support for Strategic Planning

AIS provides valuable insights that support long-term strategic planning. It generates reports on revenue trends, cost patterns, and profitability analysis, helping managers forecast future performance. These insights guide decisions regarding budgeting, investments, expansion, and resource allocation. Without AIS, businesses may lack the detailed information necessary for accurate forecasting. By offering comprehensive data analysis, AIS enables organizations to plan effectively, achieve sustainable growth, and remain competitive in an increasingly dynamic business environment.

Auditors require accurate, complete, and verifiable financial records to perform their duties. AIS provides a structured system with detailed audit trails, making verification easier. It maintains chronological records of transactions, user activities, and adjustments, ensuring transparency. By simplifying the audit process, AIS saves time for both auditors and businesses. Moreover, it reduces the risk of audit disputes by providing reliable data. Therefore, AIS is needed to facilitate smooth, efficient, and trustworthy internal and external audits.

In today’s competitive business environment, AIS provides organizations with a significant edge. By offering timely, accurate, and reliable financial data, AIS enables managers to respond faster to market changes and customer needs. It enhances decision-making, improves efficiency, and ensures compliance, all of which strengthen competitiveness. Businesses that adopt advanced AIS gain agility and transparency compared to those relying on manual systems. Thus, AIS is needed as a strategic tool for achieving long-term sustainability and market leadership.

Scope of an Accounting Information System:

- Financial Data Management

The scope of AIS includes systematic management of financial data, from collection to reporting. It captures all transactions like sales, purchases, payroll, and expenses, ensuring they are accurately recorded and organized. This makes it easier to prepare financial statements and comply with accounting standards. AIS manages both current and historical data, providing a reliable foundation for analysis. Thus, its scope covers the entire cycle of financial data handling essential for effective business operations.

- Integration with Technology

AIS extends to integrating accounting practices with modern technology such as databases, ERP systems, and cloud platforms. This integration enables automation of tasks, improved data accessibility, and enhanced processing speed. By combining technology with accounting, AIS expands its role from simple bookkeeping to strategic decision support. Its scope also includes adapting to emerging tools like artificial intelligence and data analytics. Therefore, AIS is not limited to accounting but also encompasses technological advancements that drive efficiency.

- Internal Control and Security

The scope of AIS involves ensuring strong internal controls and data security. It defines authorization levels, establishes audit trails, and applies protective measures such as encryption and firewalls. These features safeguard financial information from unauthorized access, manipulation, or fraud. By strengthening accountability and compliance, AIS supports ethical and transparent operations. Its role in maintaining the security of sensitive data makes it indispensable in protecting organizational assets and building stakeholder trust, extending its scope beyond accounting.

- Compliance and Legal Reporting

AIS has a wide scope in ensuring compliance with legal requirements and statutory reporting. It assists in preparing financial reports according to GAAP, IFRS, and local regulations. It also generates tax-related documents and helps organizations meet deadlines for filing returns. By automating compliance functions, AIS reduces the risk of penalties and enhances organizational credibility. Thus, its scope extends to meeting legal obligations, supporting auditors, and ensuring that businesses operate within the framework of regulatory standards.

AIS plays a significant role in managerial decision-making by providing timely and relevant financial information. It offers detailed analyses of revenues, expenses, profits, and costs, enabling managers to make informed choices. Its scope also includes preparing budgets, forecasts, and performance evaluations that guide future planning. By presenting real-time insights, AIS empowers businesses to respond effectively to changes in the market. Hence, its scope extends beyond record-keeping to becoming a vital tool for strategic management decisions.

- Auditing and Verification

The scope of AIS covers auditing and verification of financial records. It provides detailed documentation and audit trails that facilitate easy checking of transactions. Both internal and external auditors rely on AIS to ensure data accuracy and detect irregularities. Automated systems simplify the audit process by maintaining systematic records, reducing the possibility of disputes. This enhances transparency and accountability in reporting. Thus, AIS contributes significantly to auditing, making it an integral part of financial governance.

- Support for Strategic Planning

AIS contributes to long-term strategic planning by offering insights into financial performance and resource utilization. It generates analytical reports that highlight trends, variances, and future opportunities. This information helps organizations allocate resources effectively, set realistic goals, and pursue growth strategies. Its scope includes guiding decisions on expansion, investments, and risk management. By transforming raw data into actionable knowledge, AIS extends its role to shaping the overall strategic direction of the organization for sustainable success.

- Global and Multidimensional Application

The scope of AIS is not restricted to local operations; it also supports multinational businesses. Modern AIS systems handle multiple currencies, languages, and regulatory frameworks, making them useful for global enterprises. Their application extends across industries like manufacturing, services, banking, and retail. AIS also incorporates non-financial information, such as customer data or sustainability metrics, to provide holistic insights. Hence, its scope is multidimensional, covering diverse functions, industries, and geographies in today’s interconnected business environment.

Steps to Implement an Accounting Information System:

Step 1. Identifying Organizational Needs

The first step in implementing an AIS is to clearly identify the needs of the organization. Management must analyze business processes, accounting requirements, and decision-making needs. This includes understanding transaction volume, reporting requirements, and compliance obligations. By defining objectives, the system can be tailored to address gaps in the current accounting processes. Identifying organizational needs ensures that the AIS aligns with business goals, enhances efficiency, and provides accurate financial information for internal and external stakeholders.

Step 2. Setting Clear Objectives

Once organizational needs are identified, it is essential to set clear objectives for the AIS. Objectives may include improving reporting accuracy, strengthening internal controls, enhancing data security, or automating routine tasks. These goals serve as benchmarks to evaluate system effectiveness after implementation. Setting objectives also helps in prioritizing resources and choosing features that provide maximum value. With clearly defined objectives, the organization can ensure that the AIS is purpose-driven and aligned with both financial and strategic priorities.

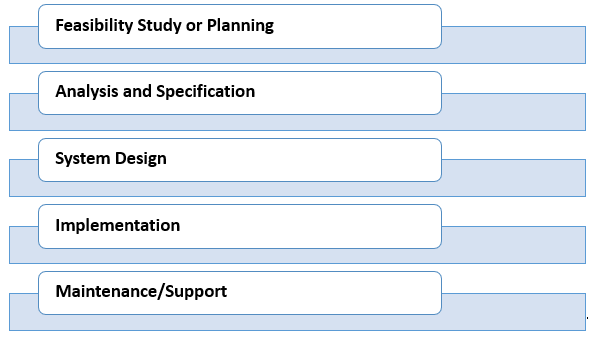

Step 3. Feasibility Study and Planning

Before implementation, a detailed feasibility study is conducted to evaluate technical, financial, and operational viability. This includes assessing the costs, potential benefits, risks, and available resources. A proper plan is then developed, outlining timelines, responsibilities, and milestones. Feasibility studies also examine whether the staff has the required technical expertise or training needs. Planning provides a roadmap for execution, minimizing unexpected challenges and ensuring that the AIS implementation is realistic, achievable, and sustainable for long-term organizational success.

Step 4. Selection of Appropriate Software

Choosing the right accounting software is critical for successful AIS implementation. Organizations must compare different options based on features, scalability, cost, integration capability, and user-friendliness. Popular solutions include ERP systems, customized accounting software, or cloud-based platforms. The chosen software should support organizational objectives, comply with regulations, and handle transaction volumes efficiently. Selection should also consider vendor reputation, customer support, and future upgrade options. A well-chosen software system ensures smooth operations, better control, and reliable financial data management.

Step 5. Designing the System Framework

The system design stage focuses on creating a framework for the AIS, including process workflows, reporting formats, and internal controls. It specifies how data will be collected, processed, stored, and communicated. This step also defines user roles, access levels, and security features. Designing ensures that the AIS aligns with business operations and accounting standards. A properly designed framework guarantees efficiency, prevents duplication, and minimizes errors, ensuring that the system is functional, secure, and adaptable to organizational needs.

Step 6. Hardware and Infrastructure Setup

AIS implementation requires suitable hardware and infrastructure to support the chosen software. This includes computers, servers, networking devices, storage systems, and backup facilities. Depending on the system type, organizations may also use cloud services for scalability. Hardware should be reliable, secure, and capable of handling high transaction loads without failure. Infrastructure also includes internet connectivity, firewalls, and antivirus tools for data protection. Proper setup of hardware and infrastructure ensures smooth operation, speed, and reliability of the accounting system.

Step 7. Data Migration and Testing

Data migration is the process of transferring existing accounting records into the new AIS. This involves cleansing, validating, and converting data from legacy systems to ensure accuracy. Once migrated, the system undergoes rigorous testing to identify errors, check functionality, and validate internal controls. Testing includes trial transactions, report generation, and reconciliation with old records. This step ensures that the AIS works as intended before going live. Effective data migration and testing prevent disruptions and ensure continuity in operations.

Step 8. Training of Personnel

Employees and accountants must be trained to use the AIS effectively. Training programs cover data entry, report generation, system navigation, and troubleshooting. This ensures that staff can fully utilize the system’s capabilities while minimizing errors. Training also emphasizes the importance of security protocols, internal controls, and compliance requirements. Continuous support and refresher training may be provided to adapt to system upgrades. Well-trained personnel are critical for successful AIS implementation since the system’s efficiency depends on user competence.

Step 9. Implementation and Monitoring

After successful testing and training, the AIS is officially implemented in the organization. This involves switching to the new system for recording transactions and generating reports. Implementation should be monitored closely to identify issues, technical glitches, or user errors. Regular supervision ensures timely corrective measures and smooth adoption. Monitoring also helps evaluate whether the system is meeting set objectives. Continuous observation during the initial phase ensures that the AIS delivers accurate results and enhances operational efficiency.

Step 10. Evaluation and Continuous Improvement

The final step is evaluating system performance and ensuring continuous improvement. Regular audits, feedback, and performance reviews help identify strengths and weaknesses of the AIS. Updates, patches, and upgrades are applied to keep the system secure and efficient. Organizations may also enhance reporting features, add automation, or integrate with other systems. Continuous improvement ensures that the AIS adapts to changing business needs, regulatory requirements, and technological advancements, making it a long-term asset for financial management.

Types of Accounting Information Systems:

1. Manual Accounting Information System

This is the most traditional type where accounting data is processed manually using paper-based journals, ledgers, and registers. Transactions are recorded by hand and financial statements are prepared without computer assistance. Though inexpensive, manual AIS is time-consuming and prone to human errors. It is usually found in very small businesses with limited transactions. Today, it is less common but still relevant in rural areas or organizations with minimal technological infrastructure.

2. Computerized Accounting Information System

A computerized AIS uses software and digital tools to record, process, and report financial data. Examples include Tally, QuickBooks, and MYOB. These systems automate calculations, maintain digital records, and generate reports efficiently. They provide greater accuracy, speed, and reliability compared to manual systems. Computerized AIS also integrates internal controls, enhances data security, and allows easy data storage and retrieval. Most medium and large organizations adopt computerized systems for effective financial management and compliance.

3. Enterprise Resource Planning (ERP) Systems

ERP-based AIS integrates accounting with other business functions like human resources, supply chain, production, and sales. Examples include SAP, Oracle NetSuite, and Microsoft Dynamics. These systems provide a centralized database, allowing departments to access consistent financial and operational data. ERP-based AIS ensures better coordination, strategic planning, and real-time reporting. Although costly to implement, ERP systems are highly effective for large organizations with complex operations, offering a holistic view of both financial and non-financial performance.

4. Cloud-Based Accounting Information System

This type of AIS uses cloud technology, enabling businesses to access financial data anytime and anywhere through the internet. Examples include Zoho Books, Xero, and FreshBooks. Cloud AIS offers scalability, data backup, remote access, and lower infrastructure costs. It also allows collaboration among accountants, managers, and auditors across different locations. However, it requires strong cybersecurity measures to safeguard sensitive data. Small to medium-sized businesses increasingly prefer cloud-based systems for their flexibility and cost efficiency.

5. Transaction Processing Systems (TPS)

TPS are specialized AIS designed to handle high volumes of routine transactions such as sales, purchases, payroll, and inventory. They ensure accuracy, speed, and reliability in day-to-day operations. For example, a retail billing system automatically records sales transactions and updates inventory. These systems provide the foundation for other AIS functions like reporting and auditing. TPS are essential for organizations dealing with thousands of transactions daily, such as banks, supermarkets, and large manufacturing firms.

6. Management Information Systems (MIS)

MIS-based AIS focuses on providing summarized financial and operational data for middle and top management. It generates reports such as budgets, performance analysis, and variance reports to support decision-making. MIS transforms raw accounting data into meaningful information that helps managers plan, monitor, and control organizational activities. Unlike TPS, which focuses on recording, MIS emphasizes analysis and reporting. Its role in decision support makes MIS an essential type of AIS in modern business environments.

7. Decision Support Systems (DSS) in Accounting

DSS-based AIS provides advanced analytical tools and models to support strategic financial decisions. It uses accounting data along with predictive analysis, simulations, and forecasting to guide decisions such as investment planning, cost control, and expansion strategies. DSS goes beyond routine reporting by offering “what-if” scenarios and financial modeling. This system is especially useful for large corporations where management must evaluate alternatives and make complex strategic decisions based on reliable accounting and non-financial data.

Advantages of an Accounting Information System:

One of the biggest advantages of AIS is enhanced accuracy in financial data management. Manual accounting is prone to human errors, such as miscalculations and misclassifications. AIS automates data entry, posting, and report generation, minimizing mistakes. By ensuring precise and reliable information, it supports compliance with accounting standards and reduces costly errors. Accurate records also enhance the credibility of financial statements, which is vital for decision-making, audits, and building stakeholder trust in the organization.

AIS saves considerable time and reduces costs by automating repetitive accounting tasks. Activities like posting entries, preparing ledgers, generating invoices, and producing reports are completed quickly with minimal effort. This efficiency enables accountants and managers to focus on analysis rather than routine work. Additionally, reducing paperwork and storage costs further contributes to financial savings. For businesses handling large transaction volumes, AIS significantly improves productivity, minimizes delays, and helps organizations operate in a cost-effective manner.

AIS provides timely and relevant financial information, which supports better decision-making. Managers can access real-time data regarding revenues, expenses, and cash flows, helping them analyze performance and plan effectively. Detailed reports and forecasts guide strategic choices such as investments, budgeting, and expansion. By integrating financial and non-financial data, AIS presents a holistic view of the organization’s operations. This advantage allows management to make informed, evidence-based decisions that contribute to competitiveness and long-term business growth.

AIS enhances internal control by establishing systematic checks and balances. It incorporates authorization protocols, segregation of duties, and automated audit trails, which reduce fraud and manipulation. Access restrictions ensure that only authorized personnel can perform specific accounting tasks, safeguarding sensitive information. By monitoring transactions and activities, AIS helps detect irregularities early and ensures accountability. Strong internal control strengthens transparency, builds stakeholder confidence, and ensures compliance with laws and regulations, making AIS vital for responsible governance.

- Better Data Storage and Security

AIS provides secure storage of accounting records using databases, servers, or cloud systems. Unlike manual files, which can be lost or damaged, digital systems ensure reliable backups and recovery options. Advanced security measures like encryption, passwords, and firewalls protect data from unauthorized access or cyber threats. Additionally, stored data can be retrieved easily for audits, analysis, or compliance purposes. This advantage of AIS ensures the confidentiality, integrity, and availability of financial information for business use.

- Support for Compliance and Auditing

AIS simplifies compliance with accounting standards, tax regulations, and legal requirements. It automatically generates statutory reports and maintains accurate records required by authorities. For auditors, AIS offers detailed audit trails, ensuring easy verification of transactions. Automated compliance reduces the risk of penalties, errors, or legal disputes. Furthermore, AIS provides transparency by maintaining accurate documentation. This advantage ensures organizations meet their legal obligations while building trust with regulators, investors, and other stakeholders through accountable practices.

- Scalability and Flexibility

AIS can adapt to the growth and changing needs of businesses. As organizations expand, transaction volumes and reporting requirements increase. AIS can scale up by handling larger data volumes and integrating new features without disrupting operations. Flexible systems such as ERP or cloud-based AIS allow customization to fit industry-specific needs. This adaptability ensures that businesses continue to operate efficiently while maintaining accurate financial records. Thus, scalability and flexibility make AIS a long-term investment for organizations.

In today’s dynamic business environment, AIS provides a strong competitive edge. It enables faster decision-making, efficient resource allocation, and real-time financial monitoring. By ensuring accuracy, efficiency, and compliance, AIS allows businesses to outperform competitors relying on manual or outdated systems. Cloud-based AIS also supports remote access and collaboration, improving organizational agility. This advantage empowers companies to respond quickly to market changes and customer demands, positioning them ahead of competitors and supporting sustainable business success.

Limitations of an Accounting Information System:

One of the major limitations of AIS is its high cost of implementation. Purchasing licensed software, upgrading hardware, hiring consultants, and training staff require significant investment. For small and medium-sized enterprises, these expenses can be burdensome. In addition, maintenance and system upgrades involve ongoing costs. While AIS improves efficiency, the initial financial burden may outweigh short-term benefits for smaller organizations, making it difficult for them to adopt advanced systems compared to larger companies.

AIS is often complex and requires specialized technical knowledge for installation, operation, and maintenance. Employees without proper training may face difficulties in using the system effectively, leading to errors or inefficiencies. Integrating AIS with existing systems can also be challenging, especially in large organizations with multiple departments. Technical glitches, software bugs, and compatibility issues add to this complexity. Without skilled IT professionals, businesses may struggle to maximize the benefits of AIS, limiting its effectiveness.

- Risk of Data Security Breaches

Although AIS incorporates security features, it remains vulnerable to cyberattacks, hacking, and data breaches. Sensitive financial data stored in digital systems can be exploited if security measures fail. Businesses relying on cloud-based AIS face risks of unauthorized access and data theft. Even internal misuse by employees can compromise data integrity. Protecting against such risks requires constant monitoring, advanced cybersecurity tools, and strict protocols, which may not always be feasible, especially for smaller organizations.

AIS heavily depends on technology for functioning. Any disruption in hardware, software, or internet connectivity can halt operations and delay reporting. Power outages, system crashes, or technical failures may result in temporary loss of access to critical financial information. Overdependence on technology also creates challenges in regions with limited infrastructure or unstable connectivity. This limitation makes AIS vulnerable to external factors beyond the organization’s control, affecting continuity in accounting and decision-making processes.

- Risk of Errors During Data Migration

When shifting from manual systems or older software to new AIS platforms, data migration is necessary. This process is prone to errors such as incomplete transfers, incorrect formatting, or data loss. If historical records are not migrated accurately, it may create inconsistencies in financial reporting. Data migration requires skilled professionals, careful planning, and significant time. Errors at this stage can compromise the reliability of the AIS and diminish its effectiveness in generating accurate financial reports.

- Resistance to Change by Employees

Another limitation is employee resistance to adopting AIS. Workers accustomed to manual systems may find it difficult to adapt to computerized processes. Fear of job loss, lack of technical skills, or reluctance to learn new systems can hinder successful implementation. Without proper training and motivation, employees may underutilize AIS features, reducing its benefits. Overcoming this resistance requires change management strategies, continuous support, and effective communication, which can be time-consuming and costly for organizations.

- Continuous Upgradation Requirement

AIS needs regular upgrades to keep up with technological advancements, regulatory changes, and growing business needs. These upgrades often involve additional costs, disruptions in workflow, and retraining employees. If organizations fail to update their systems, AIS may become outdated, exposing them to compliance risks and inefficiencies. For small businesses, frequent upgrades can be financially and operationally challenging. This limitation makes it difficult to maintain the system’s effectiveness over the long term without significant ongoing investment.

- Possibility of System Failure

Despite its advantages, AIS is not foolproof and may experience failures. Technical breakdowns, software crashes, malware attacks, or hardware damage can lead to system downtime. In such cases, businesses may face disruptions in accounting processes, delayed reporting, or even data loss. Restoring the system requires technical expertise and backup measures, which are not always available instantly. This limitation highlights the risk of overreliance on AIS without adequate contingency plans or alternative arrangements for emergencies.

Like this:

Like Loading...

by

by