Role of a Financial Manager

by

by The role of a finance manager in India involves financial planning, capital structure management, investment decisions, risk management, and ensuring regulatory compliance. They oversee working capital, optimize resource allocation, and implement financial strategies to enhance profitability. Finance managers also handle mergers, acquisitions, and corporate finance activities to drive business growth. They ensure accurate financial reporting, maintain investor confidence, and align financial goals with business objectives. By managing financial risks and adhering to SEBI, RBI, and taxation regulations, they contribute to a company’s stability and expansion. Their role is critical in ensuring financial sustainability and long-term business success.

Role of a Finance Manager in India:

-

Financial Planning and Strategy

A finance manager in India plays a crucial role in financial planning by setting short-term and long-term financial goals for the organization. They prepare budgets, forecast future financial needs, and align financial strategies with business objectives. By analyzing market trends, economic conditions, and company performance, they ensure optimal resource allocation. Financial planning helps businesses maintain liquidity, achieve growth, and minimize financial risks. Effective financial strategies contribute to organizational success, ensuring sustainable development and maximizing shareholder value in a dynamic economic environment.

-

Capital Structure Management

The finance manager is responsible for deciding the appropriate mix of debt and equity to finance business operations. They evaluate factors like interest rates, risk tolerance, and funding requirements to determine the optimal capital structure. Proper capital management ensures financial stability, reduces the cost of capital, and enhances profitability. In India, where businesses rely on a mix of bank loans, equity funding, and bonds, finance managers must make strategic decisions to balance financial risks and returns, ensuring business expansion and investor confidence.

-

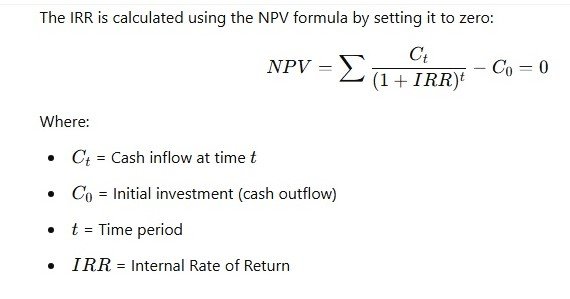

Investment and Capital Budgeting Decisions

Finance managers assess investment opportunities and allocate funds to projects that yield maximum returns. They use capital budgeting techniques like Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to evaluate long-term investments. Investment decisions impact the company’s growth and profitability, requiring careful risk assessment. In India, finance managers play a key role in funding infrastructure projects, business expansions, and technology upgrades. By making sound investment decisions, they ensure efficient capital utilization and long-term financial sustainability.

-

Working Capital Management

Effective working capital management ensures smooth business operations by maintaining an optimal balance between current assets and liabilities. Finance managers oversee cash flow, accounts receivable, inventory, and accounts payable to avoid liquidity crises. In India, businesses often face challenges like delayed payments and credit constraints. Finance managers implement strategies like just-in-time inventory management and credit control policies to optimize working capital. Proper management reduces financial stress, improves operational efficiency, and ensures uninterrupted business activities, contributing to overall organizational success.

-

Risk Management and Compliance

Finance managers in India identify, assess, and mitigate financial risks such as market volatility, credit risks, and regulatory changes. They implement strategies like diversification, hedging, and insurance to protect the company’s financial health. Compliance with financial regulations, including taxation, corporate governance, and SEBI guidelines, is essential. By ensuring adherence to legal and regulatory frameworks, finance managers prevent penalties and reputational risks. Strong risk management practices enhance business stability, investor trust, and long-term financial security in the ever-evolving Indian economic landscape.

-

Profit Allocation and Dividend Policy

Finance managers decide how to allocate profits between reinvestment and dividend distribution to shareholders. In India, companies follow different dividend policies based on profitability, growth prospects, and shareholder expectations. A well-planned dividend strategy enhances investor confidence and maintains stock market stability. Finance managers ensure a balance between rewarding investors and reinvesting in business expansion. Proper profit allocation contributes to financial sustainability, shareholder satisfaction, and the company’s long-term growth, making it a critical function of financial management in India.

-

Financial Reporting and Analysis

Finance managers are responsible for preparing and analyzing financial statements, including balance sheets, income statements, and cash flow statements. They ensure transparency, accuracy, and compliance with accounting standards like the Indian Accounting Standards (Ind AS). Financial analysis techniques such as ratio analysis and trend analysis help in assessing profitability, liquidity, and financial stability. In India, finance managers play a crucial role in presenting financial reports to stakeholders, regulators, and investors. Effective financial reporting enhances decision-making, investor confidence, and corporate governance.

-

Corporate Finance and Mergers & Acquisitions

Finance managers in India oversee corporate finance activities, including mergers, acquisitions, and fundraising. They evaluate potential mergers and acquisitions to enhance business expansion and competitive advantage. Managing financial restructuring, negotiating deals, and assessing the financial viability of partnerships are key responsibilities. With India’s growing startup ecosystem and increasing foreign investments, finance managers play a vital role in securing funding, facilitating corporate restructuring, and ensuring strategic financial growth. Their expertise in corporate finance decisions directly impacts business success and market positioning.