Cost of Capital

by

by Cost of Capital is the required return necessary to make a capital budgeting project, such as building a new factory, worthwhile. When analysts and investors discuss the cost of capital, they typically mean the weighted average of a firm’s cost of debt and cost of equity blended together.

As it is evident from the name, cost of capital refers to the weighted average cost of various capital components, i.e. sources of finance, employed by the firm such as equity, preference or debt. In finer terms, it is the rate of return, that must be received by the firm on its investment projects, to attract investors for investing capital in the firm and to maintain its market value.

The factors which determine the cost of capital are:

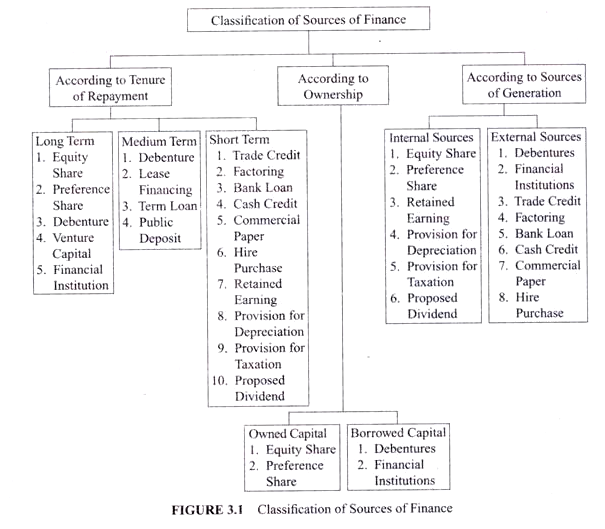

- Source of finance

- Corresponding payment for using finance

On raising funds from the market, from various sources, the firm has to pay some additional amount, apart from the principal itself. The additional amount is nothing but the cost of using the capital, i.e. cost of capital which is either paid in lump sum or at periodic intervals.

The cost of capital metric is used by companies internally to judge whether a capital project is worth the expenditure of resources, and by investors who use it to determine whether an investment is worth the risk compared to the return. The cost of capital depends on the mode of financing used. It refers to the cost of equity if the business is financed solely through equity, or to the cost of debt if it is financed solely through debt.

Many companies use a combination of debt and equity to finance their businesses and, for such companies, the overall cost of capital is derived from the weighted average cost of all capital sources, widely known as the weighted average cost of capital (WACC).

Classification of Cost of Capital

-

Explicit cost of capital

It is the cost of capital in which firm’s cash outflow is oriented towards utilization of capital which is evident, such as payment of dividend to the shareholders, interest to the debenture holders, etc.

-

Implicit cost of capital

It does not involve any cash outflow, but it denotes the opportunity foregone while opting for another alternative opportunity.

To cover the cost of raising funds from the market, cost of capital must be obtained. It helps in assessing firm’s new projects because it is the minimum return expected by the shareholders, lenders and debtholders for supplying capital to the business, as a consideration for their share in the total capital. Hence, it establishes a benchmark, which must be met out by the project.

However, if a firm is incapable of reaping the expected rate of return, the value of shares in the market will tend to decline, which will lead to the reduction in the wealth of the shareholders as a whole.

Importance of Cost of Capital

- It helps in evaluating the investment options, by converting the future cash flows of the investment avenues into present value by discounting it.

- It is helpful in capital budgeting decisions regarding the sources of finance used by the company.

- It is vital in designing the optimal capital structure of the firm, wherein the firm’s value is maximum, and the cost of capital is minimum.

- It can also be used to appraise the performance of specific projects by comparing the performance against the cost of capital.

- It is useful in framing optimum credit policy, i.e. at the time of deciding credit period to be allowed to the customers or debtors, it should be compared with the cost of allowing credit period.

Cost of capital is also termed as cut-off rate, the minimum rate of return, or hurdle rate.

Cost of capital represents a hurdle rate that a company must overcome before it can generate value, and it is used extensively in the capital budgeting process to determine whether a company should proceed with a project.

The cost of capital concept is also widely used in economics and accounting. Another way to describe the cost of capital is the opportunity cost of making an investment in a business. Wise company management will only invest in initiatives and projects that will provide returns that exceed the cost of their capital.

Cost of capital, from the perspective on an investor, is the return expected by whoever is providing the capital for a business. In other words, it is an assessment of the risk of a company’s equity. In doing this an investor may look at the volatility (beta) of a company’s financial results to determine whether a certain stock is too risky or would make a good investment.

- Cost of capital represents the return a company needs in order to take on a capital project, such as purchasing new equipment or constructing a new building.

- Cost of capital typically encompasses the cost of both equity and debt, weighted according to the company’s preferred or existing capital structure, known as the weighted-average cost of capital (WACC).

- A company’s investment decisions for new projects should always generate a return that exceeds the firm’s cost of the capital used to finance the project—otherwise, the project will not generate a return for investors.

Significance of Cost of Capital

-

Capital Allocation and Project Evaluation:

The cost of capital is paramount in capital allocation decisions. Companies must decide where to invest their limited resources, and the cost of capital serves as a benchmark for evaluating potential projects. By comparing the expected returns of a project with the cost of capital, firms can make informed investment decisions that align with shareholder value maximization.

-

Financial Performance Measurement:

It serves as a yardstick for assessing financial performance. A company’s ability to generate returns above its cost of capital indicates operational efficiency and effective resource utilization. Shareholders and investors often scrutinize this metric as it reflects the company’s capacity to create value and generate sustainable profits.

-

Cost of Debt and Equity Balancing:

The cost of capital guides the balance between debt and equity in a firm’s capital structure. As companies strive to minimize their overall cost of capital, they navigate the trade-off between the lower cost of debt and the potential risks associated with increased leverage. Striking the right balance ensures an optimal capital structure that minimizes costs while maintaining financial flexibility.

-

Investor Expectations and Market Perception:

It influences investor expectations and market perception. A company’s cost of capital is indicative of the returns investors require for providing funds. If a company consistently exceeds or falls short of this benchmark, it can impact investor confidence and influence stock prices. Managing and meeting these expectations are crucial for maintaining a positive market perception.

-

Risk Management:

The cost of capital integrates risk considerations. The cost of equity, for instance, incorporates the risk premium investors demand for investing in a particular stock. Understanding these risk components aids in strategic decision-making and risk management. Companies can adjust their capital structure and investment strategies to mitigate risk and align with their cost of capital.

-

Capital Structure Optimization:

It facilitates capital structure optimization. Achieving the right mix of debt and equity is essential for minimizing the cost of capital. Firms aim to find the optimal capital structure that maximizes shareholder value. This involves assessing the impact of various financing options on the overall cost of capital and choosing the combination that minimizes this metric.

-

Market Competitiveness:

The cost of capital impacts a company’s competitiveness. In industries where access to capital is a critical factor, having a lower cost of capital can provide a competitive advantage. This advantage enables companies to undertake projects and investments that might be financially unfeasible for competitors with higher capital costs.

- Dividend Policy and Shareholder Returns:

It guides dividend policy. Companies consider the cost of capital when determining whether to distribute profits as dividends or reinvest in the business. This decision affects shareholder returns and influences the overall attractiveness of the company’s stock to investors.

- Economic Value Added (EVA) and Shareholder Wealth:

The cost of capital is integral to Economic Value Added (EVA), a measure of a company’s ability to generate wealth for shareholders. By deducting the cost of capital from the Net Operating Profit After Taxes (NOPAT), EVA provides a clear picture of whether a company is creating or eroding shareholder value.

- Strategic Planning and Long-Term Viability:

It informs strategic planning and ensures long-term viability. By aligning investment decisions with the cost of capital, companies can focus on projects that contribute most significantly to shareholder value over the long term. This strategic alignment is crucial for sustainable growth and maintaining a competitive edge in the dynamic business environment.