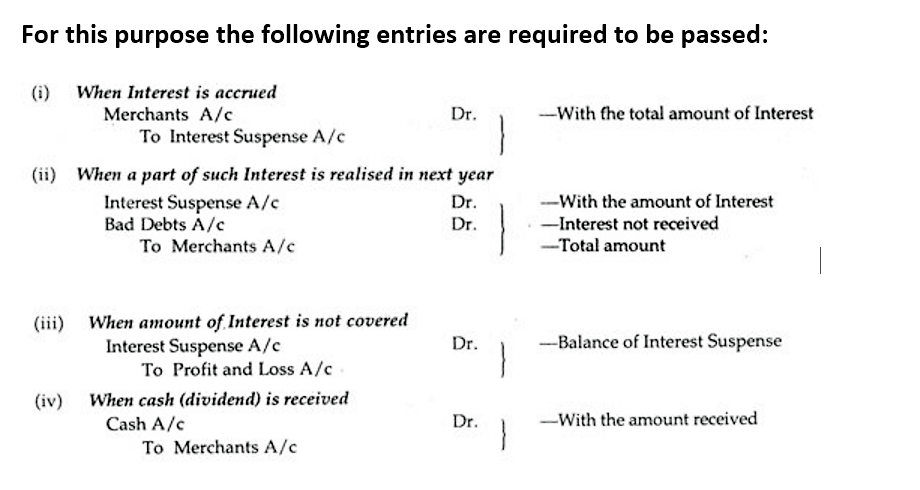

Accounting is the process of recording, classifying, summarizing, and interpreting financial transactions to provide useful information for decision-making. It relies on key principles such as the double-entry system, which ensures that every transaction affects at least two accounts, maintaining balance. Key concepts include accrual accounting, matching revenue with expenses, and the preparation of financial statements like the balance sheet, income statement, and cash flow statement. Accounting aims to provide transparency and accuracy, enabling businesses to track their performance, manage resources, and comply with legal and regulatory requirements.

Definition of Accounting

“Accounting is the art of recording, classifying, and summarizing in a significant manner and in terms of money, transactions, and events which are, in part at least, of a financial character, and interpreting the results thereof.”

“The process of identifying, measuring, and communicating financial information to permit informed judgments and decisions by users of the information.”

“Accounting is the process of identifying, measuring, and communicating economic information to permit informed judgments and decisions by users of the information.”

“Accounting is a systematic recording of business transactions in such a way as to show the outcome of business activities and the financial position of an entity.”

“Accounting is a means of collecting, summarizing, analyzing, and reporting in monetary terms, information about the business for the purpose of decision-making.”

“Accounting is the process of measuring and reporting the economic activities of an organization for decision-making purposes.”

“Accounting is a service activity that provides quantitative financial information about economic entities to be used in making economic decisions.”

“Accounting is the practice of preparing financial statements that are used by the stakeholders of an organization, including shareholders, creditors, employees, and regulators, to make informed financial decisions.”

Scope of Accounting

- Recording of Financial Transactions

The primary scope of accounting is the systematic recording of all financial transactions. Every event involving money, such as sales, purchases, expenses, or income, is entered into books of accounts like journals and ledgers. This ensures that no transaction is missed and provides a complete financial history of the business. Proper recording lays the foundation for further accounting processes like classification, summarization, and reporting, making it an essential function to maintain accuracy, accountability, and transparency in business operations.

- Classification of Transactions

After recording, accounting involves classifying transactions into meaningful categories. Similar items are grouped under respective heads — for example, all sales under the Sales Account, all salaries under the Salary Account, etc. This classification helps in organizing financial data systematically, making it easier to track, analyze, and prepare summaries. Without classification, the raw data would remain unstructured and difficult to interpret, hindering the preparation of financial statements and the extraction of useful insights for decision-making.

- Summarization of Financial Data

Once transactions are recorded and classified, accounting summarizes the data into key reports such as the Trial Balance, Profit and Loss Account, and Balance Sheet. Summarization condenses thousands of transactions into meaningful figures, showing the business’s performance and position. This process transforms detailed records into understandable reports that guide management, investors, and other stakeholders. Without summarization, the massive volume of transactional data would be overwhelming, making it nearly impossible to evaluate the financial health of the business.

- Analysis and Interpretation

Accounting goes beyond reporting figures; it involves analyzing and interpreting the summarized financial data. Analysis helps identify trends, relationships, and variances, such as profit margins, cost patterns, or liquidity positions. Interpretation explains what the numbers mean for the business, guiding managers and stakeholders in understanding strengths, weaknesses, and opportunities. This analytical scope turns raw numbers into actionable insights, supporting strategic decisions, improving performance, and ensuring that the business remains competitive in its environment.

- Communication of Financial Information

One of the crucial scopes of accounting is communicating financial information to internal and external stakeholders. Financial statements, audit reports, and management summaries serve as formal channels for conveying the company’s financial health. Investors assess returns, creditors evaluate solvency, and management plans strategies based on this communicated data. Transparent communication builds trust, enhances credibility, and fulfills statutory disclosure requirements. Without accounting, businesses would lack an organized way to share essential financial details with relevant parties.

- Compliance with Legal and Tax Requirements

Accounting ensures that businesses comply with legal obligations such as tax filings, statutory audits, and regulatory reporting. It calculates tax liabilities, prepares statutory returns, and maintains records as required by law. By providing timely and accurate financial data, accounting enables businesses to meet government regulations, avoid penalties, and maintain a good legal standing. This legal and tax compliance aspect broadens the scope of accounting beyond just internal operations, linking it directly to external regulatory frameworks.

- Assisting in Planning and Forecasting

Accounting plays a vital role in business planning and forecasting. By analyzing past financial data, businesses can predict future performance, estimate revenues, set budgets, and plan investments. It provides the foundation for creating financial models that guide decisions on expansion, diversification, cost control, or financing. Effective planning supported by accurate accounting ensures that resources are allocated efficiently, risks are managed proactively, and long-term organizational goals are achieved. Without accounting, financial planning would be speculative and unreliable.

- Facilitating Management Control

Accounting supports management in exercising control over business activities. Through cost accounting, budgetary control, and variance analysis, it provides tools to monitor operations, evaluate efficiency, and control wastage. Managers can track performance against targets, investigate deviations, and implement corrective actions. This controlling scope of accounting helps optimize resources, improve productivity, and enhance profitability. Without accounting, management would struggle to keep operations aligned with strategic objectives, potentially leading to inefficiency, overspending, or underperformance.

- Assisting in Decision-Making

Accounting provides essential data that aids managerial decision-making across various areas, including pricing, production, investments, and financing. By offering cost analyses, profitability reports, and cash flow statements, accounting helps managers evaluate different alternatives and choose the best course of action. Decision-making based on reliable accounting data reduces uncertainty, minimizes risks, and increases the likelihood of achieving desired outcomes. Without accounting, decisions would lack a solid financial foundation, increasing the chance of errors or poor choices.

- Providing Evidence and Accountability

Accounting records serve as official evidence in legal matters, tax audits, or regulatory inspections. They prove ownership of assets, existence of liabilities, validity of transactions, and fulfillment of obligations. Well-maintained accounting ensures businesses can defend themselves in disputes, claim rightful benefits, or comply with investigations. This accountability scope promotes transparency and integrity within the organization, deterring fraud and mismanagement. Without reliable accounting records, businesses expose themselves to legal vulnerabilities, reputational damage, and operational risks.

Objectives of Accounting

- Maintaining Systematic Records

The primary objective of accounting is to systematically record all financial transactions in the books of accounts. By documenting every sale, purchase, expense, income, or investment, businesses ensure no transaction is forgotten or omitted. Proper recordkeeping helps track the financial history and enables businesses to retrieve past information easily when needed. Without systematic records, it would be nearly impossible to monitor thousands of daily transactions accurately, making it hard to assess business performance or prepare reliable financial statements.

- Determining Profit or Loss

Another key objective is to ascertain the net profit or loss of a business over a specific accounting period. By matching revenues with related expenses, accounting reveals whether the business has earned a surplus or incurred a deficit. This calculation is typically done through the preparation of a Profit and Loss Account. Determining profitability is crucial for business owners, investors, and management as it guides decision-making, helps assess performance, and allows planning for improvements in future business operations.

- Determining Financial Position

Accounting helps determine the financial position of a business at the end of a period by preparing the Balance Sheet. The balance sheet lists assets, liabilities, and capital, giving a snapshot of what the business owns and owes. It helps stakeholders assess whether the business is financially strong or weak. Knowing the financial position is critical for making investment decisions, borrowing funds, or expanding operations. Without proper accounting, businesses cannot accurately measure their worth or understand their obligations.

- Providing Information to Stakeholders

Accounting serves as a communication tool by providing relevant financial information to various stakeholders. Owners, investors, creditors, employees, government agencies, and managers all rely on accounting reports to make informed decisions. For example, investors use accounting data to assess profitability, creditors to evaluate creditworthiness, and management to plan strategies. Transparent and reliable accounting helps build trust with external parties, enhances reputation, and ensures that decisions are based on accurate, up-to-date financial data.

- Assisting in Decision-Making

Accounting provides valuable data that supports managerial decision-making. Managers use financial statements, cost reports, and budget analyses to determine pricing strategies, cost controls, investment opportunities, or expansion plans. Without accurate accounting information, decision-making becomes guesswork, increasing the risk of losses. Well-maintained accounts help identify profitable products, control unnecessary expenses, and allocate resources efficiently. Accounting thus acts as a powerful tool for steering the business in the right direction and achieving long-term organizational goals.

- Compliance with Legal Requirements

Businesses are legally required to maintain proper books of accounts and prepare financial reports to comply with taxation laws, corporate regulations, and other statutory requirements. Accounting ensures businesses meet these obligations by systematically documenting transactions, calculating taxes accurately, and filing statutory returns on time. Non-compliance can lead to penalties, legal action, or damage to reputation. Therefore, accounting not only helps in managing internal operations but also ensures businesses operate within the legal framework set by authorities.

- Facilitating Audit and Verification

Accounting records provide the basis for internal and external audits, which verify the accuracy and fairness of financial statements. Auditors examine the books to ensure that transactions are properly recorded and financial reports present a true picture of the business. This verification enhances credibility and assures stakeholders of the reliability of the data. Without proper accounting, audits would be impossible, leading to mistrust, potential fraud, and mismanagement. Accounting thus plays a critical role in ensuring accountability.

- Providing Comparative Analysis

One important objective of accounting is to enable comparisons between different periods, departments, or businesses. By maintaining uniform records over time, businesses can analyze trends in revenues, expenses, and profits. This comparative analysis helps identify strengths, weaknesses, growth patterns, and areas requiring attention. For example, a business can compare this year’s sales to last year’s to evaluate growth. Consistent accounting allows management to set benchmarks, measure performance, and adjust strategies accordingly to stay competitive.

- Assisting in Budgeting and Forecasting

Accounting provides the necessary data for preparing budgets and forecasts. By analyzing past performance, businesses can estimate future revenues, expenses, and cash flows. Budgets serve as a financial roadmap, guiding organizations on how to allocate resources effectively. Forecasting helps anticipate future challenges and opportunities, allowing proactive adjustments. Without accounting data, budgeting becomes guesswork, making it hard to set realistic goals. Thus, accounting plays a central role in strategic planning, helping businesses stay financially prepared and agile.

- Providing Evidence in Legal Matters

Accounting records act as evidence in case of legal disputes, insurance claims, or tax assessments. Courts, tax authorities, and regulatory bodies often rely on a business’s books of accounts to resolve conflicts. Well-maintained records can prove the validity of transactions, ownership of assets, or fulfillment of obligations. Without proper documentation, businesses may struggle to defend themselves or claim rightful benefits. Therefore, accounting not only serves internal needs but also protects businesses legally by maintaining credible proof.

Functions of Accounting

- Recording Financial Transactions

The fundamental function of accounting is recording all business transactions systematically. Every financial event, whether it’s a sale, purchase, payment, or receipt, is documented in the books of accounts. This ensures no transaction is missed or forgotten. Proper recording creates a reliable financial history, making it easier to trace details when needed. Without this function, businesses would face disorganized data, errors, and incomplete records, leading to faulty decisions and unreliable financial statements. This forms the backbone of the entire accounting process.

Once transactions are recorded, accounting classifies them into categories based on their nature. For example, salaries go under expenses, while sales go under income. This classification is done using ledgers and ensures similar items are grouped together for better understanding. It helps businesses analyze specific areas like costs, incomes, or assets without confusion. Classification transforms raw entries into an organized structure, making it easier to summarize and interpret financial information later on. Without it, the accounts would remain chaotic and unusable.

- Summarizing Financial Data

Accounting summarizes the classified data to present it in a concise, understandable form. This is done through financial statements such as the profit and loss account, balance sheet, and cash flow statement. Summarization condenses thousands of detailed transactions into key figures that reflect business performance and position. It gives stakeholders a clear snapshot of how the business is doing, helping guide decisions. Without summarization, financial data would be overwhelming and inaccessible, making it difficult to grasp the business’s overall health.

- Analyzing Financial Information

Beyond summarizing, accounting analyzes financial data to uncover patterns, relationships, and trends. For example, businesses analyze profit margins, cost trends, or return on investment. This function helps management understand how efficiently resources are used, where costs can be controlled, and how performance compares with targets or industry standards. Financial analysis turns static numbers into meaningful insights that guide improvement. Without this, businesses would miss opportunities to optimize operations or might overlook warning signs indicating financial trouble.

Accounting not only analyzes numbers but also interprets what those numbers mean for the business. Interpretation explains the significance of financial data — for example, whether a profit is sufficient, why expenses have risen, or how cash flow affects expansion plans. This function transforms technical figures into actionable knowledge that managers and stakeholders can understand and use. Without interpretation, financial reports would remain complex and inaccessible, especially for non-experts, making it hard to apply findings to real-world decisions.

- Communicating Financial Information

Accounting functions as a communication system, sharing financial information with various users — including owners, investors, creditors, government bodies, and employees. This is done through reports, statements, and disclosures that convey the business’s financial health and activities. Effective communication builds trust, ensures transparency, and supports informed decision-making. Without proper financial communication, stakeholders would lack critical insights, leading to uncertainty, poor decisions, or even legal non-compliance. Accounting thus plays a key role in keeping everyone informed and aligned.

- Ensuring Compliance and Control

Accounting ensures businesses comply with tax laws, corporate regulations, and other legal requirements. It also provides tools for internal control, helping management monitor expenses, prevent fraud, and maintain accountability. Through regular recording and reporting, accounting creates a check-and-balance system that safeguards company assets and operations. Without this function, businesses risk fines, penalties, or operational inefficiencies. Accounting thus goes beyond numbers, acting as a governance tool that reinforces discipline, integrity, and adherence to both internal policies and external rules.

- Assisting in Planning and Forecasting

Accounting supports strategic planning and forecasting by providing historical data and trend analyses. Managers use accounting reports to create budgets, predict future costs, plan investments, and set realistic financial goals. This function ensures that decisions are grounded in actual data rather than assumptions. It helps anticipate challenges and identify opportunities, enhancing the business’s agility and preparedness. Without accounting’s contribution, planning efforts would be speculative and less effective, increasing the risk of misallocation of resources or financial shortfalls.

- Facilitating Decision-Making

Accurate and timely accounting data empowers management to make informed decisions across various areas — including pricing, resource allocation, cost control, and investment. For example, knowing the cost structure helps decide whether to cut expenses or increase prices. Financial insights also guide whether to expand, contract, or modify operations. Without accounting, decision-making would rely on guesswork, increasing the likelihood of mistakes. This function ensures that choices are data-driven, aligned with the business’s capabilities, and positioned for success.

- Providing Legal Evidence and Accountability

Accounting records serve as legal evidence in disputes, audits, and inspections. Well-maintained books prove the legitimacy of transactions, ownership of assets, and fulfillment of obligations. They also establish accountability within the organization by tracking who authorized or executed financial activities. In case of legal claims, insurance settlements, or regulatory reviews, accounting records become crucial. Without this function, businesses expose themselves to legal risks, challenges in defending claims, and potential losses due to lack of documented proof.

Purpose of Accounting

The primary purpose of accounting is to record all financial transactions systematically. Businesses engage in numerous transactions daily, such as sales, purchases, and payments. Accounting ensures that these transactions are documented in a structured way, which serves as the foundation for preparing financial reports and tracking financial performance. Accurate records also help in auditing and reviewing financial activities.

Accounting plays a critical role in maintaining financial control over business operations. By tracking revenue, expenses, assets, and liabilities, accounting ensures that businesses can monitor their financial resources effectively. This helps in controlling costs, managing budgets, and identifying any discrepancies or inefficiencies in resource allocation, allowing management to take corrective actions when necessary.

One of the key purposes of accounting is to measure the financial performance of a business over a given period. By preparing income statements and other financial reports, accounting helps businesses assess how well they are performing. These reports provide insights into profitability, revenue growth, and expense management, enabling stakeholders to evaluate whether the business is meeting its financial objectives.

Accounting provides relevant financial information that aids in decision-making for management and other stakeholders. It allows businesses to analyze past performance, forecast future trends, and make informed decisions regarding expansion, investments, and cost control. This financial data helps in setting realistic goals and improving overall business strategy.

One of the primary purposes of accounting is to ensure that businesses comply with legal and regulatory requirements. Businesses are required to follow accounting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), and comply with tax laws and financial reporting regulations. Accounting ensures that financial records are maintained accurately to meet these obligations.

Accounting serves as a means of communicating financial information to stakeholders such as investors, creditors, regulators, and employees. Stakeholders rely on accurate financial statements to assess the viability and performance of a business. Accounting ensures that financial data is presented transparently, enabling stakeholders to make informed decisions about their involvement with the company.

Accounting aids in planning and budgeting by providing historical financial data that helps businesses forecast future financial outcomes. Accurate accounting records allow businesses to create budgets, set financial targets, and allocate resources efficiently. Effective planning based on solid accounting data helps businesses prepare for future challenges and opportunities, ensuring long-term financial stability.

Importance Accounting

- Accurate Financial Records

Accounting ensures the maintenance of accurate and systematic records of all financial transactions. These records are essential for tracking the business’s performance, assets, liabilities, income, and expenses. Without proper accounting, businesses would struggle to monitor their financial health, making it difficult to assess profitability or identify financial risks. Accurate records are also required for audits, reviews, and evaluations by management and external parties.

Accounting provides vital financial data that supports effective decision-making. Business owners, managers, and investors rely on accounting information to evaluate past performance, forecast future trends, and make strategic decisions about resource allocation, investments, and cost management. It helps businesses assess whether they should expand, cut costs, or adjust their operations. Good accounting enables businesses to base their decisions on data, reducing the risk of poor judgment.

One of the key importance of accounting is ensuring compliance with legal and regulatory obligations. Governments and regulatory bodies require businesses to maintain proper financial records and submit periodic financial statements. These statements help in calculating taxes, ensuring regulatory compliance, and adhering to accounting standards like Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Non-compliance can result in legal penalties, fines, or damage to the company’s reputation.

Accounting helps in evaluating a company’s performance over a specific period. By comparing financial results (like profit margins, expenses, or revenue growth) with past records or industry standards, businesses can measure their efficiency and financial success. This performance evaluation enables businesses to understand how well they are achieving their goals and where improvements are needed, aiding in setting realistic financial targets for future growth.

A business’s ability to access external financing depends heavily on its accounting practices. Investors, banks, and other financial institutions require clear and transparent financial statements to assess a company’s creditworthiness and profitability before granting loans or investments. Proper accounting ensures that financial statements accurately reflect the business’s financial status, boosting its credibility with potential lenders or investors.

- Fraud Detection and Prevention

Effective accounting systems play a crucial role in detecting and preventing fraud. By maintaining proper internal controls and regularly reconciling accounts, businesses can identify discrepancies or suspicious activities that may indicate fraud or theft. Regular audits, supported by good accounting practices, help safeguard a company’s financial resources and maintain its integrity.

Like this:

Like Loading...

by

by