Retail internationalization is the transfer of retail operations outside the home market. It involves the international transfer of retail concepts, management skills, technology and even the buying function.

International trade and commerce has existed for centuries and played a very important part in the World History. However International Retailing has been in existence and has gained ground in the past two to three decades. The economic boom in several countries, coupled with globalization have given way to Organizations looking at setting up retailing across borders. The advent of internet and multimedia has further changed the dimensions as far as International Retailing is concerned.

The international perspective in retail business involves understanding and navigating the complexities of operating in diverse global markets. Retailers expanding internationally must consider cultural nuances, regulatory environments, consumer behaviors, and economic conditions unique to each country.

The international perspective in retail business involves a nuanced understanding of diverse markets and the ability to adapt strategies to local conditions. Successful global retailers prioritize cultural sensitivity, comply with local regulations, and leverage technology to navigate the complexities of operating on a global scale. By combining a deep understanding of local markets with a strategic and flexible approach, retailers can establish a strong international presence and capitalize on global opportunities.

Factors involved in International Retailing

A careful examination of the definition for international retailing reveals certain concepts which are key to the process of international retailing. These include operations, concepts, management expertise, technology and buying.

- Operations

Retail internationalization is the expansion of a retailer’s operations into a foreign market. The store format may or may not be similar to that in the home market. Identical operations may well trade under a different brand than that operated in the domestic market. This decision is largely dependent upon the method of market entry. On the acquisition of a foreign retail operation, the new owner may retain the original brand if it is a respected brand.

For example, in 1999 Wal-Mart (the retail giant) bought UK grocery chain ASDA and retained the original ASDA brand. When a retailer enters a new market by franchise, it may transfer an established domestic brand. Sometimes, a new foreign brand is perceived as more fashionable than its competitors.

- Concepts

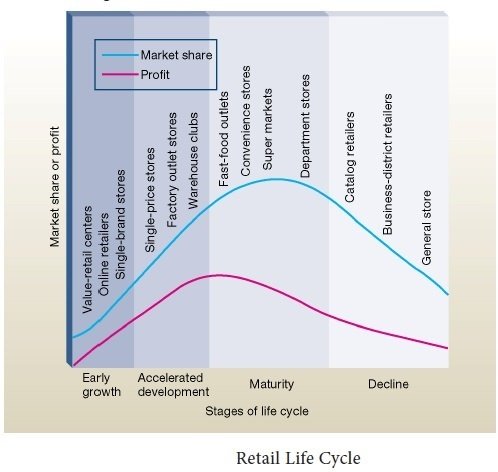

Retail concepts lay emphasis on innovations in the industry. The self service concept first emerged in California in 1912. Later, the concept was followed in a number of international markets in the next two decades. Similarly, the convenience store format which originated in USA in 1920s was taken up in Europe in the 1970s. Now, the focus in on globalization. The retail concept currently by operated by retailers may also become successful in a foreign market.

The internationalization of “the body shops” popularized the idea of environmentally sensitive products. The success of such concepts have been adopted by competitors spawning of similar retail offers in natural toiletries and cosmetics.

- Management expertise

The transfer of concepts is linked with the internationalization of management expertise. This encompassed the internationalization of skills and techniques used in the management of the business. Formation of alliances is an important means of transferring management functions. Retail alliances are prompted by operational synergies, buying economies of scale, increased retailer power over manufacturer, the development of retailer own labels and joint defense building against the market entry of foreign competitors.

International retail alliances are the direct outcome of growing globalization. Successful alliance management rests on close cooperation, communication, synergistic performance measures and an agreement to common objectives.

- Technology

Retailers who operate internationally require the use of technology advances. Use IT in central management of retail operations has improved its decision making in areas such as finance, personnel and logistics. Technologies such as EPOS (Electronic Point of Sale) are also used at operational levels of retail stores.

Generally, internationalization will employ relatively advanced technology. It is preferable for retailers to move into a market where they have a technological advantage. Technological advantage in turn, would confer a competitive advantage over indigenous retailers.

- Buying

The proportion of consumer expenditure on retail is considerably important. As the population becomes more wealthy a greater proportion of income is spent on non-essentials. Only a small percentage of total spend goes on food and clothing. A higher share of spending power is directed towards non-essentials such as holidays and leisure activities. In retail operations the function of buying is indeed sourcing. Sourcing has had the greatest impact in terms of internationalization.

Alliances are formed to attain efficiency and leverage in sourcing. International retailers use their collective influence with suppliers to reduce prices and improve quality. For example, the European alliance EMD has stated exerting the combined purchasing power of its members as its primary objective.

Reason for Internationalization of retailing

- Inadvertent internationalization

Inadvertent internationalization is due to political instability. Sometimes, changes in the demarcation of national borders take place. This may mean a retail company is operating in a different market although its stores have not physically moved. Changes in Eastern Europe are the examples of this kind. The US retailer KMart entered Czechoslovakia. Within a year it found itself operating in two district markets, the Czech and Slovak republics.

- Non-commercial reasons

Non-commercial reasons of political, personal, ethical or social responsibility have motivated retailers to move into foreign markets. For example, retailers foray into markets for reasons of social and environmental responsibility. Notably, the Body Shop’s “trade not aid” sourcing policy helped develop infrastructures in order to stabilize economics.

- Commercial objectives

It include entering the market which gives retailers competitive edge. Gaining important market knowledge before moving in on a larger scale learning about innovations may be other commercial objectives of retail internationalization.

- Government regulations

Government regulations influence the choice of market by retailers. It is not a prerequisite to internationalization. Retailers prefer the markets with fewer restrictions on their growth. Severe regulations at home push retailers into the international arena. Loi Royer in France severely restricted the development of large out of town stores. As a result the French hypermarkets turned to less restrictive markets to continue their expansion.

- Growth potential

Retailers seek the best growth potential possible. If they perceive profitable opportunities in overseas markets, they are likely to capitalize on them.

International Perspective in Retail Business

-

Globalization and Market Expansion:

Retailers may choose from various entry strategies, including franchising, joint ventures, acquisitions, or establishing wholly-owned subsidiaries, depending on the level of control desired and the nature of the market.

Managing global supply chains is crucial, involving coordination of sourcing, production, and distribution across different countries. Retailers often optimize supply chain efficiency to reduce costs and enhance flexibility.

-

Cultural Sensitivity and Localization:

- Understanding Cultural Differences:

Cultural factors significantly impact consumer preferences, shopping habits, and communication styles. Successful retailers adapt their strategies to align with local cultural norms and values.

- Localization of Products and Services:

Retailers often tailor their product offerings and services to meet local tastes and preferences. This may involve adapting packaging, marketing messages, and even the assortment of products.

-

Regulatory and Legal Considerations:

- Compliance with Local Regulations:

International retailers must navigate diverse regulatory landscapes, including tax laws, employment regulations, and trade restrictions. Understanding and complying with local laws are critical for sustained success.

- Trade Barriers and Tariffs:

Retailers need to be aware of trade barriers, tariffs, and import/export regulations that may impact the cost and availability of goods.

-

Economic Conditions:

Global retailers face exposure to currency fluctuations, which can impact pricing, profitability, and financial performance. Hedging strategies may be employed to manage currency risk.

Economic conditions in different countries influence consumer purchasing power and spending behavior. Retailers must be adaptable to economic fluctuations and tailor strategies accordingly.

-

Technology and E-commerce:

- E-commerce and Digital Platforms:

The growth of e-commerce enables retailers to reach international consumers without significant physical infrastructure. Online platforms provide opportunities for market entry and global reach.

The adoption of technology varies globally. Retailers need to assess the digital maturity of each market and adapt their technology strategies accordingly.

-

Competitive Landscape:

- Local and Global Competition:

Retailers face competition from both local players and other international brands. Understanding the competitive landscape is crucial for market positioning and differentiation.

- Partnerships and Collaborations:

Forming strategic partnerships with local businesses or entering collaborations with established players can facilitate market entry and enhance competitiveness.

-

Consumer Behavior and Trends:

- Diverse Consumer Behaviors:

Consumer preferences and behaviors differ across countries. Retailers must conduct thorough market research to understand local trends, shopping habits, and preferences.

Some consumer trends, such as sustainability and ethical consumption, have global resonance. Retailers can leverage such trends for consistent messaging across international markets.

-

Social and Environmental Responsibility:

Social and environmental responsibility are increasingly important globally. Retailers are expected to demonstrate commitment to sustainable and ethical practices, aligning with global expectations.

-

Logistics and Distribution:

- Efficient Distribution Networks:

Establishing efficient logistics and distribution networks is critical for timely and cost-effective delivery of products. Retailers often optimize distribution strategies based on the geography and infrastructure of each market.

Last-mile delivery challenges can vary significantly, and retailers must address them to provide a seamless customer experience.

-

Adaptability and Agility:

International retailers need to adopt agile business models to respond to changing market conditions, consumer preferences, and competitive landscapes.

Effective crisis management is essential for navigating unexpected challenges, such as geopolitical events, economic downturns, or public health crises.

Like this:

Like Loading...

by

by