Determinants of Demand

by

by The demand of a product is influenced by a number of factors. An organization should properly understand the relationship between the demand and its each determinant to analyze and estimate the individual and market demand of a product.

The demand for a product is influenced by various factors, such as price, consumer’s income, and growth of population.

For example, the demand for apparel changes with change in fashion and tastes and preferences of consumers. The extent to which these factors influence demand depends on the nature of a product.

An organization, while analyzing the effect of one particular determinant on demand, needs to assume other determinants to be constant. This is due to the fact that if all the determinants are allowed to differ simultaneously, then it would be difficult to estimate the extent of change in demand.

Determinants of demand are the various factors that influence a consumer’s desire and ability to purchase a product or service at a given price and time. While price is a significant factor, demand is not solely dependent on it. In real-world markets, demand is shaped by a range of non-price elements that affect consumer behavior and purchasing decisions. These determinants help explain why the demand for a good might increase or decrease, even if its price remains unchanged.

Key determinants include consumer preferences, income levels, prices of related goods (substitutes and complements), expectations about future prices and income, and the number of buyers in the market. For instance, if consumer incomes rise, demand for normal goods typically increases. Similarly, a change in the price of a complementary good (like petrol for cars) can affect the demand for a related product.

Other important factors influencing demand include advertising, weather conditions, government policies, and demographic changes. For example, a successful marketing campaign can boost consumer interest in a product, while a shift in population demographics may lead to rising demand in specific sectors like housing or healthcare.

Understanding the determinants of demand is essential for businesses, marketers, and policymakers to anticipate market trends, adjust strategies, and make informed decisions about pricing, production, and resource allocation. These determinants form the foundation for demand forecasting and economic analysis.

Determinants of demand:

1. Consumer Preferences

Consumer preferences are among the most critical non-price determinants of demand. These preferences are shaped by various factors such as lifestyle, tastes, social trends, advertising, peer influence, cultural values, product image, and consumer perception of quality.

For instance, if consumers begin preferring plant-based diets due to health or environmental concerns, the demand for meat substitutes and organic vegetables will rise. Advertising plays a major role in shaping consumer tastes and establishing brand loyalty, which directly affects demand. A well-positioned marketing campaign can shift consumer preferences and increase demand for a product even without altering its price.

Moreover, factors like occupation, personality, age, and social status also influence individual preferences. A young professional may prefer a smartphone with advanced features, while an elderly person may prioritize ease of use.

2. Prices of Related Products

The demand for a product is also influenced by the prices of related goods, which are broadly categorized into:

- Substitute Goods: Substitutes are products that can be used in place of each other. If the price of one increases, the demand for its substitute usually increases as well. Example: If the price of coffee rises significantly, consumers may switch to tea, increasing the demand for tea.

- Complementary Goods: These are products that are used together, and the demand for one is linked to the price of the other. If the price of a complement rises, the demand for the associated product tends to fall. Example: A rise in the price of petrol may reduce the demand for cars, especially if the cars are not fuel-efficient.

Understanding how goods are related helps businesses determine pricing strategies. For example, reducing the price of razors may increase the demand for razor blades due to their complementary relationship.

3. Consumer Income

Income level is a fundamental determinant of demand. The ability to purchase goods and services increases with income, assuming other factors remain unchanged. The effect of income on demand depends on the type of good:

- Normal Goods: For these goods, demand rises with an increase in income. For example, as income increases, consumers may purchase more branded clothing or dine out more often.

- Inferior Goods: For these goods, demand decreases when income rises, as consumers switch to superior alternatives. For instance, people may stop buying budget instant noodles and shift to healthier or gourmet options when their income improves.

Thus, a firm must understand whether its product is a normal or inferior good to forecast demand appropriately based on economic conditions.

4. Consumer Expectations

Expectations regarding future income, prices, and product availability can affect current demand. Consumers tend to make anticipatory decisions:

- If they expect prices to rise in the future, they may purchase more now, thereby increasing current demand.

- If they expect a fall in income due to a recession or job loss, they may reduce present consumption and postpone non-essential purchases.

Example: Before the launch of a new iPhone model, people may delay purchasing the current model, anticipating new features or price drops, which affects the demand for the existing version.

Businesses use insights into consumer expectations to time their promotions, discount cycles, and inventory stocking.

5. Number of Buyers in the Market

The size and composition of the population directly impact the total market demand. An increase in the number of consumers raises the quantity demanded, even if individual demand remains constant.

Example: A growing urban population increases demand for housing, transportation, and utility services. Similarly, a rise in the number of school-aged children boosts demand for school supplies and uniforms.

Businesses consider demographic trends—such as aging populations, rising birth rates, or increased urban migration—to develop products that meet the evolving needs of a growing or changing customer base

6. Weather and Seasonal Factors

Weather conditions and seasonal variations often have a direct influence on the demand for specific products. Certain goods experience high demand only during specific times of the year.

Examples:

- Winter increases demand for heaters, woolen clothing, and hot beverages.

- Summer leads to a rise in the consumption of ice cream, air conditioners, and cold beverages.

Weather also affects agricultural demand and production. A drought may reduce the demand for lawn care services, while heavy rains can spike umbrella and raincoat sales. Businesses use seasonal demand patterns to manage inventory, plan promotions, and optimize logistics.

7. Government Policies and Regulations

Government decisions significantly affect demand through taxes, subsidies, trade regulations, or public service announcements.

Examples:

- Subsidy on electric vehicles can increase their demand by lowering effective consumer prices.

- Ban or tax on sugary drinks may reduce their demand and shift consumption to healthier alternatives.

- Mandatory health regulations (like banning plastic) may boost the demand for eco-friendly alternatives.

Such policies can either expand or restrict consumer choice and purchasing ability, and companies must adapt their product offerings in response.

8. Technological Changes

Technological innovation influences demand by introducing new products, improving existing ones, or making older products obsolete.

Example: The introduction of smartphones drastically reduced the demand for MP3 players and digital cameras. Similarly, rapid internet connectivity increased demand for streaming services over traditional cable TV.

Technological developments also impact production and distribution, enabling better customization, lower costs, and faster delivery—further shaping consumer demand.

The Determinants of demand for a product:

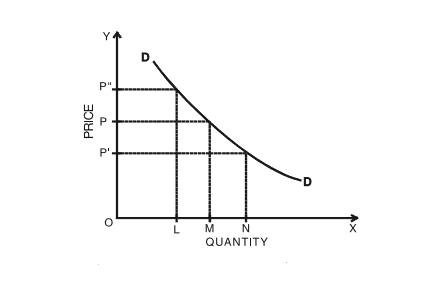

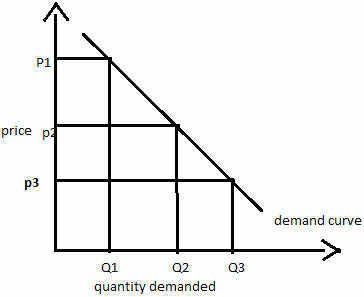

1. Price of a Product or Service

Affects the demand of a product to a large extent. There is an inverse relationship between the price of a product and quantity demanded. The demand for a product decreases with increase in its price, while other factors are constant, and vice versa.

For example, consumers prefer to purchase a product in a large quantity when the price of the product is less. The price-demand relationship marks a significant contribution in oligopolistic market where the success of an organization depends on the result of price war between the organization and its competitors.

2. Income

Constitutes one of the important determinants of demand. The income of a consumer affects his/her purchasing power, which, in turn, influences the demand for a product. Increase in the income of a consumer would automatically increase the demand for products by him/her, while other factors are at constant, and vice versa.

For example, if the salary of Mr. X increases, then he may increase the pocket money of his children and buy luxury items for his family. This would increase the demand of different products from a single family. The income-demand relationship can be analyzed by grouping goods into four categories, namely, essential consumer goods, inferior goods, normal goods, and luxury goods.

3. Tastes and Preferences of Consumers

Play a major role in influencing the individual and market demand of a product. The tastes and preferences of consumers are affected due to various factors, such as life styles, customs, common habits, and change in fashion, standard of living, religious values, age, and sex.

A change in any of these factors leads to change in the tastes and preferences of consumers. Consequently, consumers reduce the consumption of old products and add new products for their consumption. For example, if there is change in fashion, consumers would prefer new and advanced products over old- fashioned products, provided differences in prices are proportionate to their income.

Apart from this, demand is also influenced by the habits of consumers. For instance, most of the South Indians are non-vegetarian; therefore, the demand for non- vegetarian products is higher in Southern India. In addition, sex ratio has a relative impact on the demand for many products.

For instance, if females are large in number as compared to males in a particular area, then the demand for feminine products, such as make-up kits and cosmetics, would be high in that area.

4. Price of Related Goods

Refer to the fact that the demand for a specific product is influenced by the price of related goods to a greater extent.

Related goods can be of two types, namely, substitutes and complementary goods, which are explained as follows:

- Substitutes: Refer to goods that satisfy the same need of consumers but at a different price. For example, tea and coffee, jowar and bajra, and groundnut oil and sunflower oil are substitute to each other. The increase in the price of a good results in increase in the demand of its substitute with low price. Therefore, consumers usually prefer to purchase a substitute, if the price of a particular good gets increased.

- Complementary Goods: Refer to goods that are consumed simultaneously or in combination. In other words, complementary goods are consumed together. For example, pen and ink, car and petrol, and tea and sugar are used together. Therefore, the demand for complementary goods changes simultaneously. The complementary goods are inversely related to each other. For example, increase in the prices of petrol would decrease the demand of cars.

5. Expectations of Consumers

Imply that expectations of consumers about future changes in the price of a product affect the demand for that product in the short run. For example, if consumers expect that the prices of petrol would rise in the next week, then the demand of petrol would increase in the present.

On the other hand, consumers would delay the purchase of products whose prices are expected to be decreased in future, especially in case of non-essential products. Apart from this, if consumers anticipate an increase in their income, this would result in increase in demand for certain products. Moreover, the scarcity of specific products in future would also lead to increase in their demand in present.

6. Effect of Advertisements

Refers to one of the important factors of determining the demand for a product. Effective advertisements are helpful in many ways, such as catching the attention of consumers, informing them about the availability of a product, demonstrating the features of the product to potential consumers, and persuading them to purchase the product. Consumers are highly sensitive about advertisements as sometimes they get attached to advertisements endorsed by their favorite celebrities. This results in the increase demand for a product.

7. Distribution of Income in the Society

Influences the demand for a product in the market to a large extent. If income is equally distributed among people in the society, the demand for products would be higher than in case of unequal distribution of income. However, the distribution of income in the society varies widely.

This leads to the high or low consumption of a product by different segments of the society. For example, the high income segment of the society would prefer luxury goods, while the low income segment would prefer necessary goods. In such a scenario, demand for luxury goods would increase in the high income segment, whereas demand for necessity goods would increase in the low income segment.

8. Growth of Population

Acts as a crucial factor that affect the market demand of a product. If the number of consumers increases in the market, the consumption capacity of consumers would also increase. Therefore, high growth of population would result in the increase in the demand for different products.