by

by Debenture is a long-term debt instrument issued by companies or governments to raise funds from the public or institutional investors. It is essentially a loan agreement where the issuer agrees to pay interest (called the coupon) at a fixed or floating rate and repay the principal amount at maturity. Unlike shares, debentures do not confer ownership rights; instead, they represent a creditor relationship between the holder and the issuer.

Debentures can be secured or unsecured. Secured debentures are backed by specific assets or collateral, providing more safety to investors. Unsecured debentures, also known as naked debentures, rely solely on the creditworthiness of the issuer. They are typically issued by well-established companies with a strong financial reputation.

Debentures can also vary in terms of convertibility. Convertible debentures can be converted into equity shares after a specified period, offering potential upside if the company performs well. Non-convertible debentures (NCDs) remain purely debt instruments until maturity.

Debentures play a crucial role in corporate financing by allowing companies to raise large amounts without diluting ownership. For investors, they offer a balance between safety and return, especially when issued by reputable companies or backed by assets.

Feature of Debentures

- Fixed Interest Rate

One of the primary features of debentures is that they carry a fixed rate of interest, known as the coupon rate, which is paid to debenture holders at regular intervals, usually semi-annually or annually. This fixed income feature makes debentures attractive to conservative investors seeking predictable returns. Unlike dividends on shares, which depend on profits, the interest on debentures is an obligation and must be paid even if the company faces losses, thus providing a sense of security to the investor.

- Maturity Period

Debentures are issued for a specific period, which is known as the maturity period, and at the end of this period, the principal amount must be repaid to the debenture holders. The maturity period can range from a few years to several decades, depending on the type and purpose of the issue. This fixed tenure gives both the company and the investor a clear timeline, with the company knowing when the repayment is due and the investor knowing when they will receive back their invested capital.

- No Ownership Rights

Debenture holders are considered creditors of the company, not owners. This means they do not have any voting rights or control over company decisions. While equity shareholders have a say in the company’s management and policies through voting, debenture holders have no such influence. Their relationship with the company is purely financial, limited to the repayment of interest and principal. This feature appeals to investors who are not interested in management control but seek assured returns from their investments.

- Priority over Equity Holders

In the event of liquidation or winding up of the company, debenture holders have a higher claim on the company’s assets than equity shareholders. This means that the company must first repay its debts, including debentures, before distributing any remaining assets to shareholders. This feature makes debentures a relatively safer investment compared to shares, as debenture holders have a better chance of recovering their money if the company faces financial distress or bankruptcy.

- Security Backing (in Secured Debentures)

Many debentures are secured by the company’s fixed or floating assets, meaning specific assets are pledged as collateral for the loan. If the company defaults on payment, the debenture holders can claim the secured assets to recover their dues. This security feature enhances the safety of investment for holders of secured debentures. Unsecured debentures, on the other hand, carry more risk but are usually issued by companies with strong reputations and high creditworthiness to compensate for the lack of collateral.

- Convertibility Option

Certain debentures come with the option to convert them into equity shares after a specified period, known as convertible debentures. This feature allows investors to benefit from the company’s growth by becoming shareholders if the company performs well. Convertible debentures usually carry a lower interest rate compared to non-convertible debentures because they offer the added benefit of potential equity participation. Non-convertible debentures (NCDs), however, remain purely debt instruments throughout their life, providing only fixed income without equity conversion.

- Tradability and Transferability

Debentures are typically listed on stock exchanges, making them easily tradable and transferable among investors. This liquidity feature is important because it allows investors to sell their debentures in the secondary market before maturity if they need cash or want to adjust their investment portfolios. The ability to transfer ownership without involving the issuing company enhances flexibility and marketability, making debentures an attractive instrument for both institutional and retail investors seeking investment mobility.

- Tax Implications

The interest earned on debentures is considered taxable income in the hands of the investor. From the company’s perspective, however, the interest paid on debentures is treated as a tax-deductible expense, reducing the company’s taxable profits. This tax benefit makes debentures a cost-effective financing tool for companies, especially compared to dividends, which are not tax-deductible. For investors, understanding the tax treatment of debenture income is important when evaluating the overall return on investment.

- Covenants and Terms

Debentures are often governed by detailed terms and conditions specified in the debenture trust deed. This includes covenants that impose certain restrictions or obligations on the issuing company, such as maintaining specific financial ratios, limiting further borrowings, or restricting asset sales. These covenants are designed to protect the interests of debenture holders and ensure that the company remains financially healthy enough to meet its repayment obligations. Compliance with these terms is monitored by a trustee on behalf of the debenture holders.

- Redeemability

Debentures can be classified as redeemable or irredeemable (perpetual). Redeemable debentures are repaid by the company on or before a specified maturity date, either as a lump sum or through periodic installments. Irredeemable debentures, on the other hand, do not have a fixed maturity date and continue indefinitely, with interest payments made until the company decides to redeem them voluntarily or is wound up. Redeemability offers clarity and assurance to investors about the timeline of their capital recovery.

Types of Debentures

1. Registered Debentures

Registered debentures are recorded in the company’s register with details like the holder’s name, address, and holding amount. Transfer of ownership requires proper registration and documentation, ensuring safety and preventing unauthorized transfers. These debentures are ideal for investors who prefer formal ownership records and are less concerned about liquidity. Since only the registered person can claim interest or repayment, they offer an extra layer of security. However, trading registered debentures can be slower due to the administrative steps required to update ownership records upon transfer.

2. Bearer Debentures

Bearer debentures are not registered in the company’s records and are transferable by mere delivery, making them highly liquid. The holder of the physical certificate is considered the owner and can claim interest and repayment. These debentures typically carry coupons attached, which the holder presents to receive interest payments. Bearer debentures are attractive for investors seeking anonymity and easy transferability. However, they also pose higher risks, such as loss or theft, since possession determines ownership. Their ease of transfer makes them popular in secondary markets, but they are less common today due to regulatory controls.

3. Secured (Mortgage) Debentures

Secured debentures are backed by specific assets or a general charge over the company’s assets, providing security to investors. If the company defaults on repayment, holders of secured debentures can claim the pledged assets to recover their dues. They are also called mortgage debentures when secured by immovable property. This security feature reduces the investment risk, making them attractive to conservative investors. Companies offering secured debentures often pay slightly lower interest rates compared to unsecured ones, as the collateral reduces the lender’s risk exposure.

4. Unsecured (Naked) Debentures

Unsecured debentures, also known as naked debentures, are not backed by any specific assets or security. Holders rely solely on the issuer’s creditworthiness for repayment. These debentures carry higher risk compared to secured ones and generally offer higher interest rates as compensation. Companies with strong financial standing and good reputations can issue unsecured debentures successfully. Investors in unsecured debentures are considered general creditors during liquidation and have a lower priority compared to secured creditors. Despite the higher risk, they are favored by some investors for their potential returns.

5. Convertible Debentures

Convertible debentures come with an option to convert them into equity shares of the company after a specified period. This gives investors the potential for capital appreciation if the company performs well, in addition to earning fixed interest until conversion. Convertible debentures typically offer lower interest rates compared to non-convertible ones because of the added equity conversion benefit. They appeal to investors looking for a balance between safety and growth opportunities. However, once converted, they lose their debt characteristics and become subject to the risks and rewards of equity ownership.

6. Non-Convertible Debentures (NCDs)

Non-convertible debentures remain purely debt instruments throughout their tenure and cannot be converted into shares. These debentures offer fixed interest income and are usually issued with a specified maturity period, at the end of which the principal is repaid. NCDs can be either secured or unsecured, depending on the terms of issuance. Investors seeking predictable returns and no exposure to equity risk often prefer NCDs. Companies may issue NCDs when they want to raise long-term funds without diluting ownership or offering potential equity upside to investors.

7. Redeemable Debentures

Redeemable debentures are issued with a clear repayment or redemption date, either as a lump sum or through scheduled installments. The company has a legal obligation to repay the principal on or before the specified maturity date. These debentures provide certainty to investors regarding when they will receive their invested capital. Redeemable debentures can be structured with callable features, allowing the company to redeem them early if desired. They are commonly used for long-term financing projects where companies plan future repayments through profits or refinancing.

8. Irredeemable (Perpetual) Debentures

Irredeemable debentures, also known as perpetual debentures, do not carry a fixed maturity date. Instead, the company pays interest indefinitely, and the principal is repaid only upon the company’s liquidation or at its discretion. These debentures provide investors with a steady income stream but no guarantee of capital repayment within a fixed timeline. They are less common today but can be useful in specific financing structures, particularly for companies looking to maintain long-term capital without a redemption pressure. Investors in perpetual debentures need to assess the issuer’s long-term stability carefully.

9. Participating Debentures

Participating debentures provide investors with the right to participate in the company’s profits beyond the fixed interest rate. In addition to the assured interest, holders may receive an extra return linked to the company’s performance, often expressed as a share of profits. These debentures are attractive to investors who want both steady income and a share in the company’s success without taking on the full risks of equity. For companies, participating debentures can be a flexible tool to align financing costs with profitability.

10. Zero-Coupon Debentures

Zero-coupon debentures do not pay periodic interest. Instead, they are issued at a deep discount to their face value, and investors receive the full face value at maturity. The difference between the purchase price and the maturity value represents the investor’s return. These debentures appeal to investors looking for capital appreciation rather than regular income. For companies, zero-coupon debentures can be advantageous because they reduce periodic cash outflows, concentrating the repayment obligation at maturity. They are sensitive to interest rate changes, which can affect their market value.

Advantage of Debentures

- Stable Source of Long-Term Finance

Debentures provide companies with a stable and reliable source of long-term finance. Unlike short-term loans or working capital borrowings, debentures are typically issued for extended periods, often five years or more. This long-term funding allows companies to plan and invest in large projects without worrying about frequent repayments. By securing capital through debentures, companies can support expansion, modernization, or acquisitions with confidence. The predictability of repayment schedules helps firms align their financing needs with long-term growth strategies, ensuring they maintain operational stability and minimize liquidity risks.

- No Ownership Dilution

A major advantage of issuing debentures is that it raises capital without diluting the ownership or control of existing shareholders. Since debenture holders are creditors, not owners, they have no voting rights in company decisions or management. This makes debentures an attractive financing tool for companies wishing to retain control within the hands of existing promoters or stakeholders. By choosing debentures over equity issuance, companies can expand their financial base and meet funding needs without compromising on governance, protecting the interests of both management and current shareholders.

- Tax Deductibility of Interest

Interest payments on debentures are treated as a tax-deductible expense for companies, reducing their overall taxable income. This results in significant tax savings compared to dividend payments on equity shares, which are not tax-deductible. For highly profitable companies, this tax benefit can substantially lower the effective cost of borrowing. Consequently, debentures become an efficient financing instrument, allowing firms to optimize their capital structure by reducing their tax burden while ensuring access to needed funds. The tax shield provided by interest payments enhances the overall financial attractiveness of debentures.

- Lower Cost of Capital

Debentures generally carry lower costs compared to equity financing, primarily because investors in debt expect lower returns than equity holders due to reduced risk. The fixed-interest nature of debentures means companies are not obligated to share additional profits with debenture holders, unlike dividends for shareholders. Moreover, the tax deductibility of interest further reduces the effective cost of capital. Companies with strong credit ratings can issue debentures at competitive rates, making them a cost-effective choice for raising funds, especially when compared to issuing new equity or seeking high-interest loans.

- Fixed Repayment Terms

Debentures come with predetermined repayment schedules, offering predictability in financial planning for both issuers and investors. Companies know exactly when and how much they need to repay, which aids in budgeting and cash flow management. Investors, in turn, benefit from clarity on when they will receive interest payments and principal repayment. This fixed nature reduces uncertainty and allows businesses to match repayments with revenue generation timelines, such as aligning maturity dates with the completion of long-term projects or asset life cycles, ensuring smooth financial operations.

- Flexibility in Design

Debentures offer significant flexibility in terms of structuring repayment terms, interest rates, convertibility options, and security backing. Companies can tailor debenture offerings to match their specific funding needs and market preferences. For example, they may issue convertible debentures to attract investors seeking both fixed income and potential equity upside or opt for secured debentures to lower borrowing costs by pledging assets. This flexibility allows firms to strategically tap into different investor segments, ensuring they raise capital on the most favorable terms while balancing risk and cost.

- Wide Investor Base

Debentures attract a wide range of investors, including institutional investors, pension funds, mutual funds, insurance companies, and conservative individual investors. These investors are typically drawn by the security, fixed income, and predictable returns associated with debentures. By tapping into such a broad base, companies can access substantial pools of capital and diversify their funding sources beyond traditional banking relationships. The popularity of debentures among risk-averse investors makes them a reliable fundraising tool, especially for well-established companies with strong credit ratings and consistent financial performance.

- Enhances Creditworthiness

Successfully issuing debentures in the market can enhance a company’s credit profile and reputation. A strong debenture issuance signals financial strength, stability, and market confidence, improving the firm’s standing with other creditors, suppliers, and stakeholders. This enhanced creditworthiness can lead to better financing terms in future borrowings, improved supplier relationships, and greater investor confidence. Moreover, regular and timely servicing of debenture obligations builds a positive track record, positioning the company as a responsible borrower capable of managing debt efficiently, further opening doors to future financing.

- No Profit Sharing Obligation

Unlike equity shareholders, debenture holders are entitled only to fixed interest payments, irrespective of the company’s profitability. Even if the company achieves record profits, debenture holders cannot demand a share of the excess earnings. This allows companies to retain surplus profits for reinvestment, dividend distribution to shareholders, or reserve accumulation. By using debentures, companies gain access to necessary funds without committing to sharing their long-term financial success, making debentures a strategic tool for balancing external financing needs with internal wealth retention and growth objectives.

Disadvantage of Debentures

- Fixed Interest Burden

Debentures require the issuer to pay fixed interest periodically, regardless of the company’s profitability. Even during downturns or financial stress, the obligation to pay interest remains, putting pressure on cash flows. This can limit a firm’s flexibility and reduce liquidity for operational needs. Unlike dividends on equity shares, which can be skipped in poor years, interest on debentures is mandatory. Failure to meet interest payments may lead to legal consequences or damage to creditworthiness, making debentures a rigid financial commitment for companies.

- Repayment Obligation

Debentures must be repaid at maturity, which can strain the company’s finances if adequate provisions are not made in advance. Unlike equity shares, which are not repaid unless liquidated, debentures have a predetermined redemption timeline. If the company fails to arrange sufficient funds for repayment, it may have to refinance or liquidate assets, affecting operations. This fixed repayment requirement increases financial risk and reduces financial flexibility, especially for businesses facing market uncertainty or with inconsistent cash flows.

- Asset-Based Security Requirement

Secured debentures are often backed by specific assets as collateral, which may restrict the company’s ability to freely use or sell these assets. The encumbrance on key assets reduces a firm’s borrowing capacity for future needs. Additionally, in case of default, the debenture holders have the right to claim these assets, potentially disrupting business operations. Companies with limited unencumbered assets may find it difficult to raise funds through secured debentures, thereby limiting their financing options and strategic autonomy.

- No Flexibility During Economic Downturns

Debenture interest and repayment obligations continue regardless of a firm’s financial health. In times of economic slowdown or recession, this inflexible obligation can worsen financial strain. Companies may be forced to divert resources from critical areas like R&D, marketing, or inventory management to meet fixed payments. Unlike equity financing, which adapts to business cycles by varying dividends, debentures offer no such leeway. This lack of flexibility can weaken the company’s ability to adapt, innovate, and stay competitive during tough times.

- Increased Financial Risk (Leverage)

Excessive reliance on debentures increases a company’s financial leverage. While leverage can enhance returns in good times, it amplifies losses during downturns. High levels of debt in the capital structure increase the risk of insolvency or bankruptcy if the company’s earnings fall short of expectations. Creditors, including debenture holders, have priority claims on assets over shareholders, potentially leaving equity investors with nothing in case of liquidation. Therefore, overuse of debentures can jeopardize the overall financial stability of a business.

- Restrictive Covenants and Conditions

Debenture agreements often come with restrictive covenants that limit the company’s operational and financial freedom. These may include restrictions on taking additional loans, selling assets, or paying dividends to shareholders. Such conditions are designed to protect the interests of debenture holders but may constrain the company’s strategic initiatives and long-term planning. Companies may find it difficult to respond quickly to market opportunities or challenges due to these contractual obligations, thereby affecting agility and innovation in business decisions.

- Negative Impact on Credit Ratings

Issuing large amounts of debentures increases the company’s debt burden, which can negatively impact its credit rating. Credit rating agencies closely monitor debt-equity ratios and interest coverage ratios to assess credit risk. A lower credit rating leads to higher borrowing costs, not just for future debentures but for other loans as well. Additionally, it can erode investor confidence, reduce share prices, and limit access to capital markets. This reputational risk makes debenture financing less attractive for companies already operating with high debt levels.

- Not Suitable for Startups or Loss-Making Firms

Debentures are generally unsuitable for startups or firms with inconsistent or negative earnings. These entities may struggle to meet fixed interest payments or arrange for redemption, increasing the likelihood of default. Since debenture holders are risk-averse, they typically require collateral and a strong credit history—something many early-stage or distressed companies lack. As a result, debenture financing becomes inaccessible or very expensive for such firms, making it a viable option primarily for established, creditworthy businesses with stable cash flows.

- Investor Perception and Market Sentiment

Heavy issuance of debentures may send negative signals to investors and the market. It can be interpreted as a sign that the company is avoiding equity financing due to fear of dilution or lack of confidence in share valuation. If the market perceives the firm to be highly leveraged or over-dependent on debt, it may lead to reduced investor confidence, falling stock prices, and increased scrutiny. Such sentiments can affect the company’s reputation, access to capital, and shareholder relations in the long term.

Valuation of Debentures:

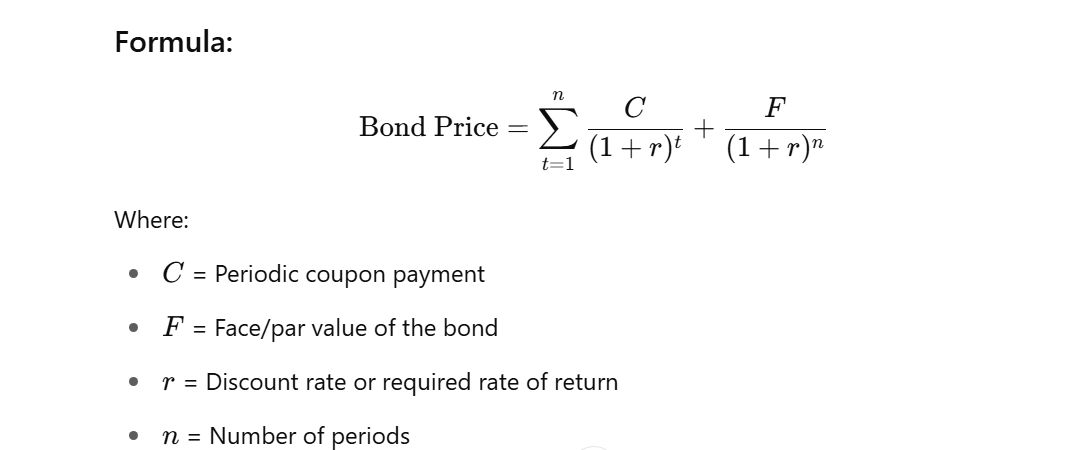

- Present Value Method (Discounted Cash Flow Method)

Present Value Method, also known as the Discounted Cash Flow (DCF) method, is the most widely used and fundamental method for bond valuation. Under this method, the value of a bond is the sum of the present values of its future cash flows, which include periodic interest payments (coupons) and the principal repayment at maturity.

The discount rate reflects the investor’s required return considering the bond’s risk. Each cash flow is discounted back to its present value using this rate. The more distant the cash flow, the lower its present value. If market interest rates increase, the present value of a bond’s cash flows decreases, and so does the bond’s price. Conversely, falling interest rates raise the bond’s price. This method is accurate and reflects the time value of money, making it the most theoretically sound approach for valuing both government and corporate bonds.

- Current Yield Method

Current Yield (CY) method provides a quick, approximate measure of a bond’s return based on its annual coupon income relative to its current market price. It does not consider the time value of money or capital gains/losses from holding the bond to maturity.

Formula:

Current Yield = Annual Coupon Payment / Current Market Price of Bond × 100

For example, if a bond has a face value of ₹1,000, a coupon rate of 8% (₹80 annual interest), and its current market price is ₹950, the current yield would be:

80950 × 100 = 8.42%

This method is commonly used by investors for comparing the yield of bonds in the secondary market. However, it does not account for changes in bond price due to interest rate fluctuations or maturity, and ignores the reinvestment of coupon payments. Therefore, while it’s easy to calculate and understand, the Current Yield is only suitable for initial screening or rough comparisons—not for precise bond valuation. It is best used when the investor plans to hold the bond for a short time or when price stability is assumed.

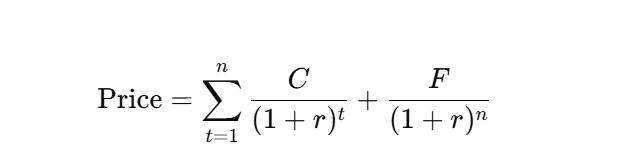

- Yield to Maturity (YTM) Method

The Yield to Maturity (YTM) is a comprehensive and widely accepted method for bond valuation. It refers to the rate of return expected on a bond if it is held until maturity, assuming all coupon payments are reinvested at the same rate. Unlike the Current Yield, YTM considers both the coupon income and any capital gain or loss (i.e., difference between purchase price and face value).

Formula (conceptually):

The bond price is equated to the present value of all future cash flows, and YTM is the rate (r) that satisfies:

This equation is solved iteratively (trial and error or using financial calculators/Excel).

YTM is considered the true return from a bond investment. It’s especially useful when bonds are not selling at face value (i.e., at a discount or premium). For instance, if a bond is priced at ₹950 with a face value of ₹1,000, the investor will earn not just interest, but also a capital gain of ₹50 if held to maturity. Hence, YTM accounts for total return. Despite being more complex to calculate, it’s a preferred method by financial analysts for making informed investment decisions.

Share this:

- Share on X (Opens in new window) X

- Share on Facebook (Opens in new window) Facebook

- Share on WhatsApp (Opens in new window) WhatsApp

- Share on Telegram (Opens in new window) Telegram

- Email a link to a friend (Opens in new window) Email

- Share on LinkedIn (Opens in new window) LinkedIn

- Share on Reddit (Opens in new window) Reddit

- Share on Threads (Opens in new window) Threads

- More