by

by Steps for Preparing Funds Flow Statement:

The steps involved in preparing the statement are as follows:

- Determine the change (increase or decrease) in working capital.

- Determine the adjustments account to be made to net income.

- For each non-current account on the balance sheet, establish the increase or decrease in that account. Analyze the change to decide whether it is a source (increase) or use (decrease) of working capital.

- Be sure the total of all sources including those from operations minus the total of all uses equals the change found in working capital in Step 1.

General Rules for Preparing Funds Flow Statement:

The following general rules should be observed while preparing funds flow statement:

- Increase in a current asset means increase (plus) in working capital.

- Decrease in a current asset means decrease (minus) in working capital.

- Increase in a current liability means decrease (minus) in working capital.

- Decrease in a current liability means increase (plus) in working capital.

- Increase in current asset and increase in current liability does not affect working capital.

- Decrease in current asset and decrease in current liability does not affect working capital.

- Changes in fixed (non-current) assets and fixed (non-current) liabilities affects working capital.

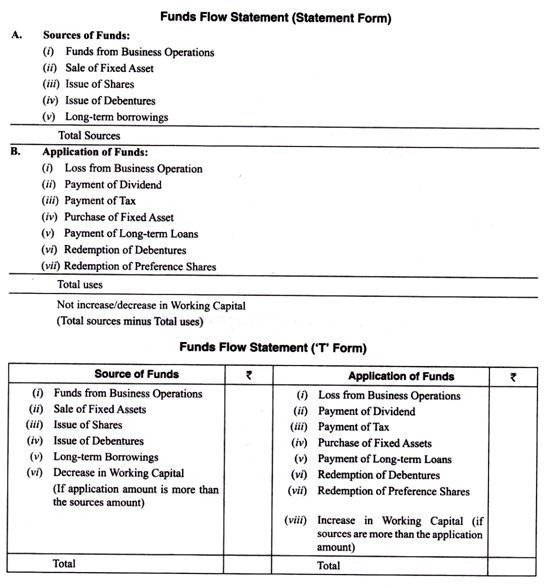

Format of Funds Flow Statement:

A funds flow statement can be prepared in statement form or ‘T’ form.

Both the formats are given below:

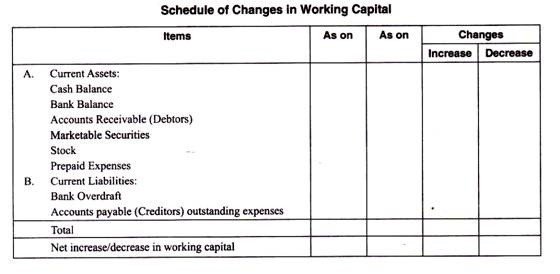

Schedule of Changes in Working Capital:

Many business enterprises prefer to prepare another statement, known as schedule of changes in working capital, while preparing a funds flow statement, on a working capital basis. This schedule of changes in working capital provides information concerning the changes in each individual current assets and current liabilities accounts (items).

This schedule is a part of the funds flow statement and increase (decrease) in working capital indicated by the schedule of changes in working capital will be equal to the amount of changes in working capital as found by funds flow statement. The schedule of changes in working capital can be prepared by comparing the current assets and current liabilities at two periods.

The format of schedule of changes in working capital is as follows:

One thought on “Procedure for preparation of Fund Flow Statement”