by

by Kurtosis is a statistical measure that describes the degree of peakedness or flatness of a frequency distribution in comparison with a normal distribution. It indicates how observations are concentrated around the mean and how the tails of the distribution behave.

In Business Statistics, kurtosis helps analysts understand the shape of a distribution and identify whether data contains extreme observations. It is widely used in finance, economics, market research, quality control, and risk analysis.

Definition of Kurtosis

Kurtosis is the measure of the shape of a distribution that indicates the extent to which observations cluster around the center and the thickness of the tails relative to a normal distribution.

The term Kurtosis was introduced by Karl Pearson.

Excess Kurtosis

An excess kurtosis is a metric that compares the kurtosis of a distribution against the kurtosis of a normal distribution. The kurtosis of a normal distribution equals 3. Therefore, the excess kurtosis is found using the formula below:

Excess Kurtosis = Kurtosis – 3

Types of Kurtosis

The types of kurtosis are determined by the excess kurtosis of a particular distribution. The excess kurtosis can take positive or negative values as well, as values close to zero.

1. Mesokurtic

Mesokurtic Distribution is a distribution that has the same degree of peakedness and tail thickness as a normal distribution. It serves as the standard or benchmark against which other types of kurtosis are compared. In a mesokurtic distribution, observations are moderately concentrated around the mean, and the tails are neither too heavy nor too light. The coefficient of kurtosis (β₂) is equal to 3, while excess kurtosis is 0. Many natural and social phenomena approximately follow a mesokurtic pattern. This type of distribution indicates a balanced spread of data without an unusual concentration of extreme values. In business statistics, mesokurtic distributions are often considered ideal because they reflect a normal and predictable pattern of observations.

Example: The distribution of examination scores in a large class often approximates a mesokurtic distribution.

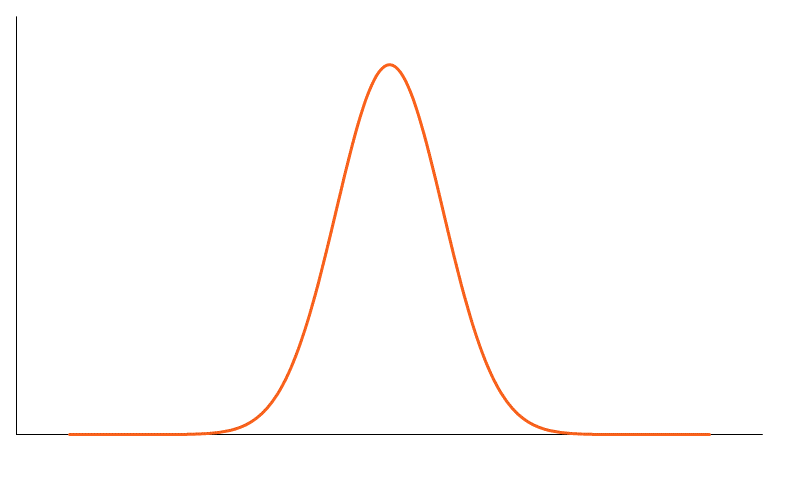

2. Leptokurtic

Leptokurtic Distribution is more peaked than a normal distribution and has heavier tails. In this type of distribution, a large number of observations are concentrated near the mean, while the tails contain more extreme values than a normal distribution. The coefficient of kurtosis (β₂) is greater than 3, and excess kurtosis is positive. Because of its heavy tails, a leptokurtic distribution indicates a higher probability of extreme observations occurring. This characteristic is particularly important in finance and investment analysis, where sudden gains or losses may occur. In business statistics, leptokurtic distributions are useful for identifying situations involving high risk and volatility. The presence of a sharp peak and heavy tails suggests that observations cluster around the center but occasionally produce significant deviations from the average.

Example: Stock market returns often follow a leptokurtic distribution because extreme gains and losses occur more frequently than expected under a normal distribution.

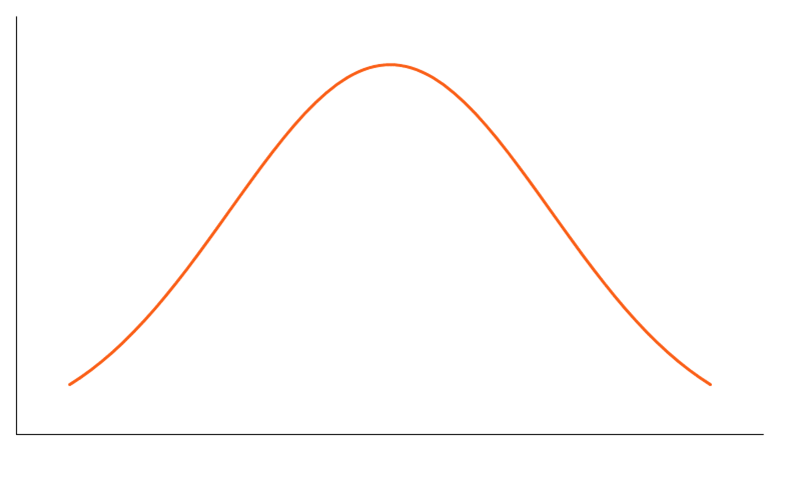

3. Platykurtic

Platykurtic Distribution is flatter than a normal distribution and has lighter tails. In this type of distribution, observations are more evenly spread across the range of data, resulting in a broad and low central peak. The coefficient of kurtosis (β₂) is less than 3, while excess kurtosis is negative. Because the tails are lighter, extreme observations occur less frequently than in a normal distribution. A platykurtic distribution indicates greater dispersion and lower concentration of observations around the mean. In business statistics, such distributions may occur when data is uniformly distributed across different categories. The flatter shape suggests that observations are widely dispersed and that the likelihood of unusually high or low values is relatively small.

Example: The distribution of customer arrivals spread evenly throughout a day may exhibit a platykurtic pattern.

One thought on “Kurtosis”