by

by This method is also called, Proportional Capitalization Method, Gradual Capitalization Method or Actual Cash Price Paid Method. As the name itself indicates, this method assumes that the asset accrues to the hirer gradually to the extent of payment made towards the cash price of the asset acquired on hire purchase basis. Therefore, in the books of the hirer or hire purchaser, Asset Account is debited to the extent of only the instalment amount paid towards the cash price of the asset. In other words, Asset Account is debited with the instalment towards cash price of the asset every time instalment is paid. The salient features of this method are as follows.

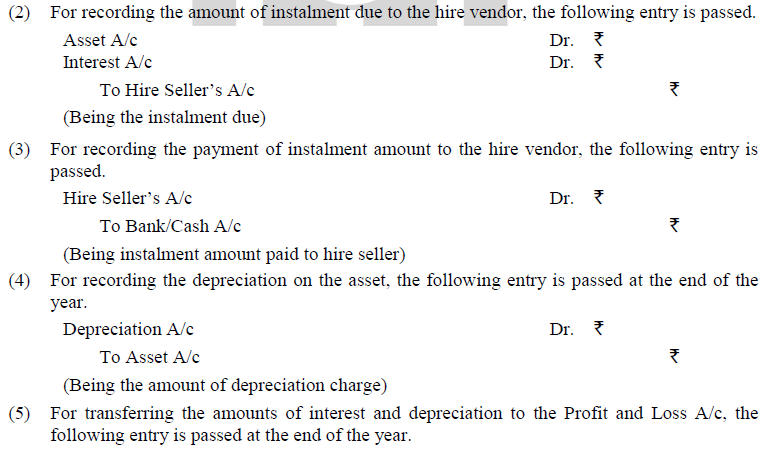

(1) As both the amount due and the interest due thereon (i.e., on the amount due) are zero at the time of signing the hire purchase agreement (i.e., at the time of delivery of the asset), down payment, if any, made is only towards the cash price of the asset (but not towards interest also). Therefore, the amount of down payment is debited to Asset A/c crediting Cash or Bank A/c.

(2) Each instalment payable is towards both the cash price of the asset (called, instalment cash price) and the interest accrued on the amount outstanding (from the date of immediately preceding instalment paid and the date of the current instalment payment). When the instalment is due for payment, a portion of instalment towards cash price is debited to Assets A/c and the remaining portion pertaining to interest is debited to Interest A/c crediting Hire Seller’s A/c. When the payment is made, Hire Seller’s A/c is debited and Cash or Bank A/c is credited.

(3) Since the hire purchaser starts using the asset acquired under hire purchase system, the asset is subject to wear and tear. Hence, depreciation is provided in the books of the hirer, usually, at the end of each accounting year. Therefore, Depreciation A/c is debited and Asset A/c is credited.

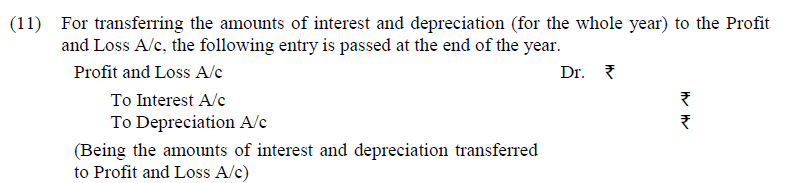

(4) As both the amounts of interest paid (as a part of instalment amount) and depreciation charged constitute the expenses (i.e., items of Nominal Accounts), both are transferred to Profit and Loss A/c at the end of each accounting year by debiting Profit and Loss A/c (for the aggregate of interest and depreciation) crediting Interest A/c (for the amount of interest) and Depreciation A/c (for the amount of depreciation).

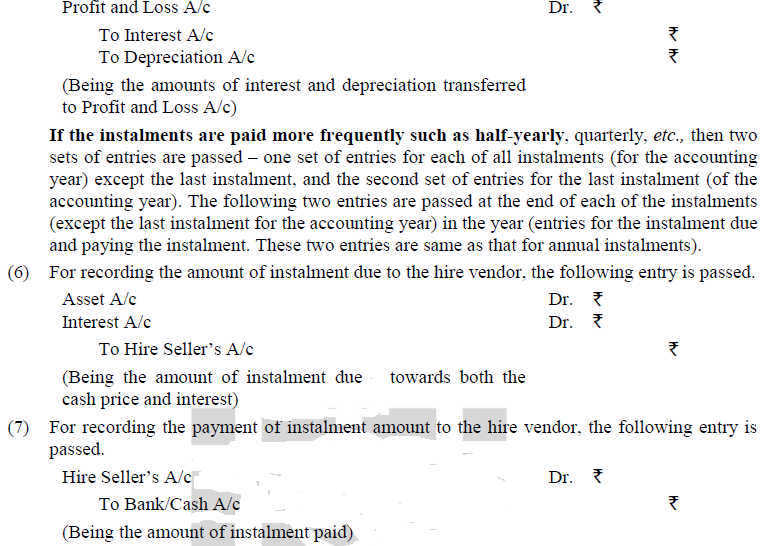

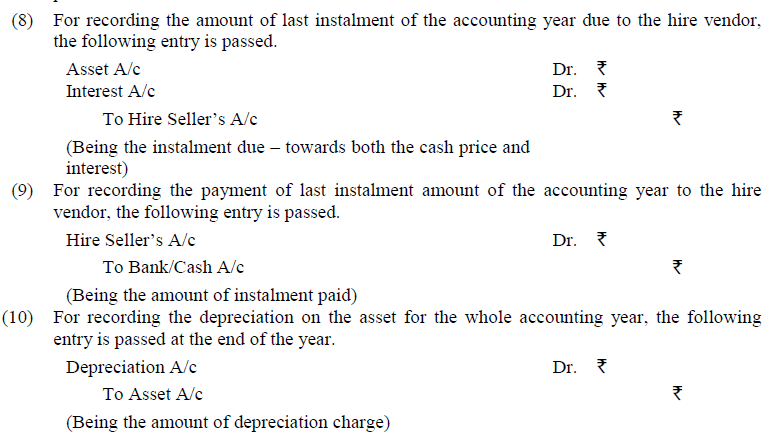

With this introduction about the nature of Asset Accrual Method, the journal entries for different hire purchase transactions in the books of hire purchaser are presented below.