by

by The budget is an estimate of income and expenditure for a definite duration. In economics, budget is a systematic list of revenue and expenditure or we can say it’s a plan for income and expenditure.

The word ‘budget’ has been borrowed from the English word “Bowgette” which traces its origin from the French word “Bougette”. Word “Bougette” has arrived from the word, ‘Bouge’ which means a leather bag.

The Union Budget of India, also referred to as the Annual Financial Statement in the Article 112 of the Constitution of India, is the annual budget of the Republic of India. The Government presents it on the first day of February so that it could be materialised before the beginning of new financial year in April. Until 2016 it was presented on the last working day of February by the Finance Minister in Parliament. The budget, which is presented by means of the Finance bill and the Appropriation bill has to be passed by Lok Sabha before it can come into effect on 1 April, the start of India’s financial year.

An interim budget is not the same as a ‘Vote on Account’. While a ‘Vote on Account’ deals only with the expenditure side of the government’s budget. An interim budget is a complete set of accounts, including both expenditure and receipts. An interim budget gives the complete financial statement, very similar to a full budget. While the law does not disqualify the Union government from introducing tax changes, normally during an election year, successive governments have avoided making any major changes in income tax laws during an interim budget.

As of September 2017, Morarji Desai has presented 10 budgets which is the highest count followed by P Chidambaram’s 9 and Pranab Mukherjee’s 8. Yashwant Sinha, Yashwantrao Chavan and C.D. Deshmukh have presented 7 budgets each while Manmohan Singh and T.T. Krishnamachari have presented 6 budgets.

Reason OF Union Budget

The Government performs two important functions by making a budget every year:

- The Government estimates the expected expenditures for developmental works in different sectors of the economy e.g. Industry, Manufacturing, Education, Health, Transport, etc.

- To meet the expenditures for the coming financial year, the Government tries to work out the sources of revenue. ( i.e. by imposing new taxes or increasing or decreasing the previous rates of taxes, or to remove or impose subsidy on any commodity.

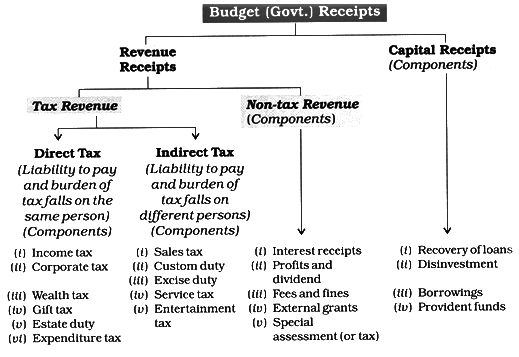

Components of the Union (Central) Budget of India:

The budget is divided into two parts:

(i) Revenue Budget and

(ii) Capital Budget.

The Revenue Budget comprises revenue receipts and expenditure met from these revenues. The revenue receipts include both tax revenue (like income tax, excise duty) and non-tax revenue (like interest receipts, profits). Capital Budget consists of capital receipts {like borrowing, disinvestment) and long period capital expenditure (creation of assets, investment).

Capital receipts are receipts of the government which create liabilities or reduce financial assets, e.g., market borrowing, recovery of loan, etc. Capital expenditure is the expenditure of the government which either creates assets or reduces liability. Capital budget is an account of assets and liabilities of the government which takes into consideration changes in capital.

Structure or components of a government budget broadly consists of two parts Budget Receipts and Budget Expenditure as shown in the following chart with their classification.

Types of Budget

- Traditional or General Budget: The initial structure of the present-day general budget is known as the Traditional Budget. The main aim of the General Budget is to set up financial control over the Executive and the Legislative. This budget contains the details of income and expenditure of the Government.

This budget contains the details of the expenditure in different sectors done by the Government. However, the result of this expenditure is not explained in this budget. Thus, the main idea behind the traditional budget that is to solve the problems of independent India and to achieve the developmental targets was defeated.

As a result, the need and importance of drafting a ‘Performance Budget was accepted and it was presented as a complimentary budget to the earlier Traditional budget.

- Performance Budget: When the outcome of any activity is taken as the base of any budget, such a budget is known as ‘Performance Budget’. For the first time in the world, the performance budget was made in the USA. An Administrative Reforms Commission was set up in 1949 in America under Sir Hooper. This commission recommended for making a ‘Performance Budget’ in the USA. In the Performance Budget, it is the compulsion of the government to tell that ‘what is done’, ‘how much done’ by it for the betterment of the people. In India, the Performance Budget is also known as the ‘Outcome Budget’.

- Zero Based Budget: There are two primary reasons for adopting this type of Budget in India.

(i) The continuous revenue deficit in the budget of the country.

(ii) Poor implementation of the Performance Budget.

In the zero-based budget, neither expenses incurred during the previous financial years are not considered nor the expenditure of the last financial year used for the coming years.

Under Zero-based budgets, every activity is decided based on Zero basis i.e. the previous expenditures are not considered. This budget is also known as ‘Sun Set Budget’ which means the finance department has to present the zero-based budget before the end of the financial year.

Outcome Budget: In India, development-related schemes such as MGNREGA, NRHM, Mid Day Meal, PMGSY, Digital India, Prime Minister Skill Development Council, etc. are started every year. The large sum of money is spent on these schemes every year. However, at present, the government doesn’t have any parameters to measure the results of these schemes.

Budget Deficit

A budget deficit occurs when government expenditures exceed revenues from taxes and other sources. Although the concept of a budget deficit applies to any organization with operating revenues and expenses, the term is most commonly applied to government budgets.

Components

- Revenues

For national governments, a majority of revenue comes from income taxes, corporate taxes, consumption taxes, and social insurance taxes. For non-governmental organizations and companies, revenues come from the sale of goods and services.

- Expenses

For governments, expenses include government spending on healthcare, infrastructure, defense, subsidies, pensions, and other items that contribute to the health of the overall economy. For non-governmental organizations and companies, expenses include the amount that is spent on daily operations and factors of production, including rent and wages.

Implications

Contrary to what it may sound like, a budget deficit is not always a negative indicator of economic health. Some of the implications of a budget deficit are described below:

- Increase aggregate demand

A budget deficit implies a reduction in taxes and an increase in government spending, which results in an increase in the aggregate demand of the country and subsequent economic growth, ceteris paribus.

- Boost the economy during a recession

During a recession, the economy tends to experience a decrease in investment spending from the private sector, along with lower aggregate consumption and demand. A government may choose to borrow and run a deficit to combat the situation by taking measures to spend effectively.

- Increase government spending

Government spending serves many purposes, including investments in infrastructure, healthcare, human capital, unemployment benefits, pension programs, and so on. A nation’s government may choose to spend more than its revenues allow by running a deficit.

- Fiscal policy

A budget deficit may be used to finance an expansionary fiscal policy, which involves lowering income and corporate taxes (therefore reducing revenue for the government) and increasing government spending on infrastructure and investments to attract foreign capital and boost economic growth.

- Higher taxes in the future

A current budget deficit that runs persistently often implies that the government will need to increase taxes in the future to pay off the accumulated debt since taxes are one of the primary sources of revenue for the government.

- Higher interest rates and bond yields

In order to borrow large amounts, governments often offer higher interest rates to investors and international banks that lend them money. Increased government borrowing results in higher interest rates and bond yields since investors and banks require compensation for the risk through interest payments.

Theories

- Ricardian Equivalence Theory

The Ricardian Equivalence Theory argues that using budget deficit or borrowing to stimulate the economy exerts no effect. It relies on many assumptions, including one that states that the government will increase taxes to pay off the current deficit.

According to the theory, households take it into account while making investment and saving decisions and choose to save more to compensate for the future increase in taxes. Therefore, consumption in the economy decreases, and the increase in government spending financed by a deficit does not impact the economy.

- Crowding Out Theory

The Crowding Out Theory states that an increase in government spending and borrowing leads to a decrease in investments from the private sector. It is because governments borrow by selling bonds to the private sector and by borrowing from foreign sources, such as other countries and international banks.

However, it often results in higher interest rates, as well as higher spending on bonds by the private sector which leads to lower funds for private sector investments and a higher cost of borrowing (due to higher interest rates).

Therefore, the increase in government spending is often met with a relatively smaller decrease in private sector investments, which offsets the overall effect of the expansionary move.

Types of Budget Deficit

There are three types of budget deficit, which are explained below

- Fiscal Deficit

- Revenue Deficit

- Primary Deficit

Fiscal Deficit

Fiscal deficit is defined as the excess of total expenditures over the total receipts excluding the borrowings in a year. In other words, this can be defined as the amount that the government needs to borrow in order to meet all expenses.

The more the fiscal deficit more will be the amount borrowed. Fiscal deficit helps in understanding the shortfall that the government faces while paying for the expenditures in the absence of lack of funds.

The formula for calculating fiscal deficit is as follows

Fiscal deficit = Total expenditures – Total Receipts excluding borrowings.

Impact of Fiscal Deficit

The following impacts of fiscal deficit can be seen

- Unnecessary expenditure: A high fiscal deficit leads to unnecessary expenditure done by the government that leads to potential inflationary pressure on the economy.

- Printing more currency by RBI for meeting the deficit, also called deficit financing leads to the availability of more money in the market, leading to inflation.

- Borrowing more will hinder the future growth of the economy as most of the revenue will be utilised towards meeting debt payments.

Remedial measures for Fiscal Deficit

- Reduced public expenditure

- Reduction in bonus, leave encashments and subsidies

- Increase tax to generate revenue

- Disinvestment of public sector units

Revenue Deficit

Revenue expenditure is defined as the excess of total revenue expenditure over the total revenue receipts. In other words, the shortfall of revenue receipts as compared to the revenue expenditure is known as revenue deficit

Revenue deficit signals to the economists that the revenue earned by the government is insufficient to meet the requirements of the expenditures required for the essential government functions.

The formula for revenue deficit can be expressed as

Revenue Deficit = Total Revenue expenditure – Total Revenue receipts

Impact of Revenue Deficit

- Reduction in assets: For meeting the shortfall in the form of revenue deficit, the government has to sell some assets.

- It leads to conditions of inflation in the economy

- A large number of borrowing leads to a greater debt burden on the economy.

Remedial measures for Fiscal Deficit

- By reducing unnecessary spending.

- By raising the rate of taxes and applying new taxes, wherever possible.

Primary Deficit

Primary deficit is said to be the fiscal deficit of the current year minus the interest payments that are pending on previous borrowings, or it can be said that primary deficit is the requirement of borrowing without the interest payment.

Primary deficit, therefore, shows the expenses that government borrowings are going to fulfil while not paying for the income interest payment.

A zero deficit shows that there is a requirement for availing credit or borrowing for clearing the interest payments pending.

The formula for the primary deficit is expressed as follows

Primary Deficit = Fiscal Deficit – Interest Payments

Measures to reduce the primary deficit can be similar to the steps taken to reduce the fiscal deficit as the primary deficit is any borrowings that are above the existing deficit or borrowings.