by

by Target costing can be viewed as a proactive cost management tool used to reduce the total cost of the product, over its complete lifecycle, through production, engineering, research and design. It helps the firm in managing the business in reaping profits in the extremely competitive market.

Simply put, target costing is a process of ascertaining and attaining full stream cost, at which the intended product with specific requirements, must be produced so as to realise the desired profits, at an anticipated selling price over a specified period. It involves the discernment of maximum cost to be incurred on a new product, followed by the development of sample that can be profitably created for that target cost figure.

Target Costing and Product Development Phase

In this technique, the costs are planned and managed out of the product or process early in the introduction phase like development or designing, instead of performing it in the latter phase of product development.

Target Costing applies to new products and succeeding generations of a product. It begins with understanding the market thoroughly and an intention to satisfy customer needs, concerning product quality, features, timeliness and price.

Target Cost

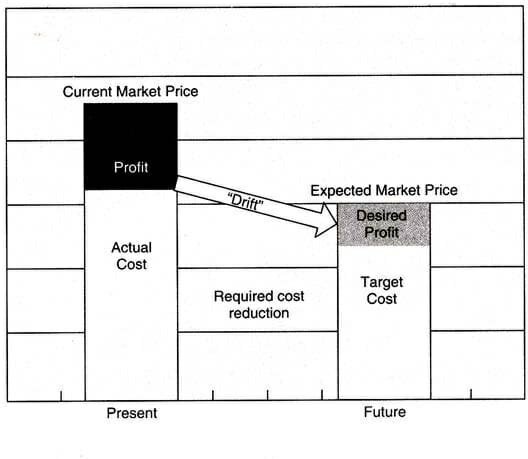

Target Cost = Anticipated selling price – Desired profit

Target Cost refers to an estimate of product cost reached by deducting a desired profit margin from the competitive market price.

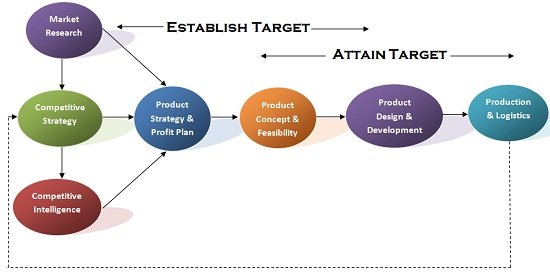

Target Costing Process

Establishment Phase of Target Cost

- Determine selling price for the new product and estimated output from market analysis and target profit.

- Ascertainment of the target cost by deducting the profit from the selling price.

- Functional cost analysis for specific components and processes

- Decide the estimated product cost.

- Make comparison between estimated cost and target cost.

- If the estimated cost is greater than the targeted one, then repeat cost analysis, to reduce the estimated cost.

- Final decision to be taken, on the introduction of the product, once the estimated cost is on target.

- Cost management while production is performed.

Attainment Phase of Target Cost

In target costing process, the cost which is directly influenced by it is given priority, which includes material and purchase parts, tooling cost, conversion cost, development expenses and depreciation. Nevertheless, it is a comprehensive cost management technique, so all those cost and assets which are influenced by initial product planning decision are taken into account.

Target Costing Principles

- Price-led costing

- Cross functional teams

- Customer focus

- Focus on product design and process

- Lifecycle cost reduction

- Value Chain involvement

Target Costing is all about planning or projecting the cost of a product prior to its introduction, to make sure that products with low margin are not introduced, as they are not able to reap sufficient returns. It is also used for controlling the design specification and production techniques, and encouraging a focus on the customer.

Advantages of Target Costing:

- It shows management’s commitment to process improvements and product innovation to gain competitive advantages.

- The product is created from the expectation of the customer and hence cost is also based on similar lines. Thus, the customer feels more value is delivered.

- With the passage of time, the company’s operations improve drastically, creating economies of scale.

- The company’s approach to designing and manufacturing products becomes market-driven.

- New market opportunities can be converted into real savings to achieve the best value for money rather than to simply realize the lowest cost.

One thought on “Target costing”