by

by Funds flow statement is a statement which discloses the analytical information about the different sources of a fund and the application of the same in an accounting cycle. It deals with the transactions which change either the amount of current assets and current liabilities (in the form of decrease or increase in working capital) or fixed assets, long-term loans including ownership fund.

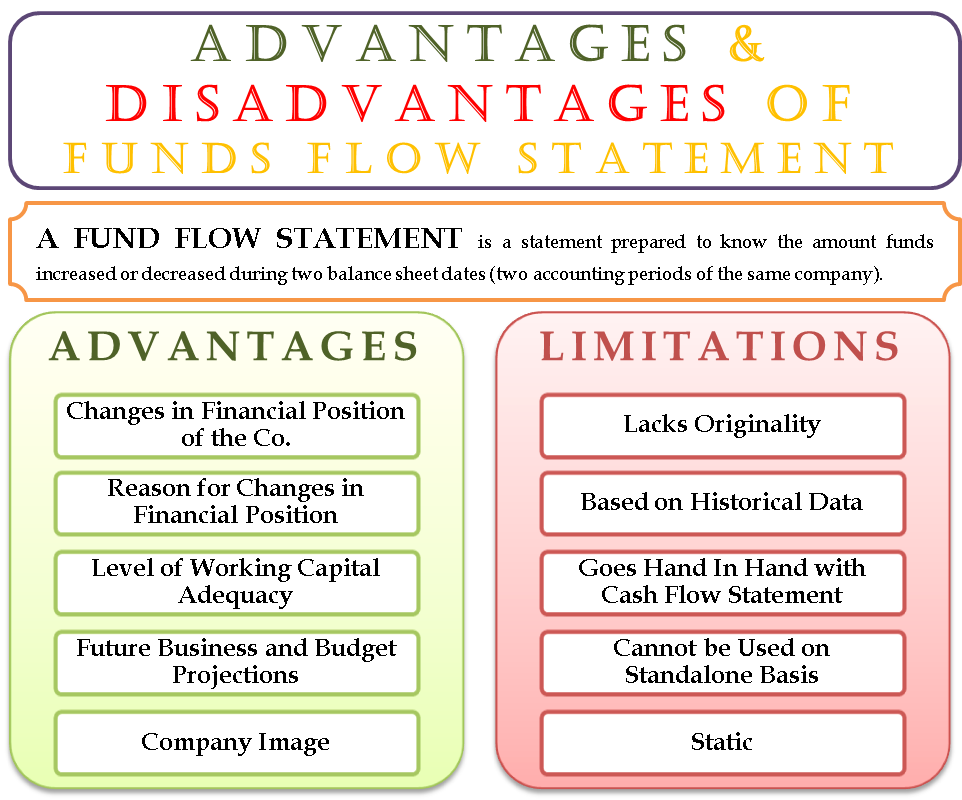

It gives a clear picture about the movement of funds between the opening and closing dates of the Balance Sheet. It is also called the Statement of Sources and Applications of Funds, Movement of Funds Statement; Where Got—Where Gone Statement: Inflow and Outflow of Fund Statement, etc. No doubt, Funds Flow Statement is an important indicator of financial analysis and control. It is valuable and also helps to determine how the funds are financed. The financial analyst can evaluate the future flows of a firm on the basis of past data.

This statement supplies an efficient method for the financial manager in order to assess the:

(a) Growth of the firm

(b) Its resulting financial needs

(c) To determine the best way to finance those needs

In particular, funds flow statements are very useful in planning intermediate and long-term financing.

Objective of Preparing a Fund Flow Statement

The main purpose of preparing a Funds Flow Statement is that it reveals clearly the important items relating to sources and applications of funds of fixed assets, long-term loans including capital. It also informs how far the assets derived from normal activities of business are being utilized properly with adequate consideration.

Secondly, it also reveals how much out of the total funds is being collected by disposing of fixed assets, how much from issuing shares or debentures, how much from long-term or short-term loans, and how much from normal operational activities of the business.

Thirdly, it also provides the information about the specific utilization of such funds, i.e. how much has been applied for acquiring fixed assets, how much for repayment of long-term or short-term loans as well as for payment of tax and dividend etc.

Lastly, it helps the management to prepare budgets and formulate the policies that will be adopted for future operational activities.

Significance and Importance of Funds Flow Statement

Since traditional reports (i.e. Income Statement/Profit and Loss Account, and Balance Sheet) are not very informative, a financial analyst has to depend on some other report—Funds Flow Statement. In other words, along with the traditional sources of information, some other sources of information are absolutely required in order to take the challenge offered by modern business.

Funds Flow Statement, no doubt, caters to the needs of management. This is because a Funds Flow Statement not only presents the Balance Sheet values for consecutive two years, it also ascertains the changes of working capital—which is a very important indicator.

It not only reveals the source from which additional working capital has been financed but also, at the same time, the use of such funds. Moreover, from a projected funds flow statement the management can easily ascertain the adequacy or inadequacy of working capital, i.e., it helps in decision-making in a number of ways.

The significance and importance of Funds Flow Statements may be summarized as:

(a) Analysis of Financial Statement

The traditional financial statements, viz. Profit and Loss Account and Balance Sheet, exhibit the result of the operation and financial position of a firm. Balance Sheet presents a static view about the resources and how the said resources have been utilized at a particular date with recording the changes in financial activities. But Funds Flow Statement can do so, i.e., it explains the causes of changes so made and effect of such change in the firm accordingly.

(b) Highlighting Answers to Various Perplexing Questions

Funds Flow Statement highlights answers of the following questions:

- Causes of changes in Working Capital;

- Whether the firm sells any Non-Current Asset; if sold, how were the proceeds utilized?

- Why smaller amount of dividend is paid in spite of sufficient profit?

- Where did the net profit go?

- Was it possible to pay more dividend than the present one?

- Did the firm pay-off its scheduled debts? If so, how, and from what sources?

- Sources of increased Working Capital, etc.

(c) Realistic Dividend Policy

Sometimes it may so happen that a firm, instead of having sufficient profit, cannot pay dividend due to lack of liquid sources, viz. cash. In such a circumstance, Funds Flow Statement helps the firm to take decision about a sound dividend policy which is very helpful to the management.

(d) Proper Allocation of Resources

Resources are always limited. So, it is the duty of the management to make its proper use. A projected Funds Flow Statement helps the management to take proper decision about the proper allocation of business resources in a best possible manner since it highlights the future.

(e) As a Future Guide

A projected Funds Flow Statement acts as a business guide. It helps the management to make provision for the future for the necessary funds to be required on the basis of the problem faced. In other words, the future needs of the fund for various purposes can be known well in advance which is a very helpful guide to the management. In short, a firm may arrange funds on the basis of this statement in order to avoid the financial problem that may arise in future.

(f) Appraising of the Working Capital

A projected Funds Flow Statement, no doubt, helps the management to know about how the working capital has been efficiently used and, at the same time, also suggests how to improve the working capital position for the future on the basis of the present problem faced by it, if any.

One thought on “Funds Flow Analysis”