Control of Marketing operations

by

by In any management practice, the functions of planning, staffing, directing and controlling are very crucial. Controlling is an important element of management and measuring and correcting of activities to assure that events conform to a marketing plan. It measures performance against goals and plans, shows where negative deviations exist and by putting in motion actions to correct deviations, helps assure accomplishment of plans.

Marketing control is a crucial function of marketing management. Using suitable controls, any deviation in marketing programmes and plans could be detected and corrected to direct it towards the marketing objectives and goals. Marketing control provides the means of testing whether desired goals and results are actually being achieved or not.

During planning of marketing programmes, the marketing objectives and targets are set and controls are used to check the implementation of marketing programmes and plans will lead to the set target and if not, then corrective action must be taken to ensure that at the end of the period, the actual performance of the marketing department and its activity is close to the desired results.

Marketing control is the most important task of the marketing department of a company. It is a control tool for ensuring that the marketing activities of company get directed towards its marketing objectives. According to Kotler, “Marketing control is the process of measuring and evaluating the results of marketing strategies and plans and taking corrective action to ensure that marketing objectives are attained.”

Marketing control is a crucial part of the marketing job. It is the role for ensuring that the marketing programmes and activities of the firm are always directed toward its marketing objectives. Marketing control provides the means of testing whether the desired goals and results are being achieved or not. Inherent in the process is the assumption that the desired results are known beforehand. And knowing the desired results in advance, involves planning. In this sense, planning and control are closely interrelated.

Therefore, marketing control is defined, as the set of process that determines the deviation, if any, between the actual sales performance and the desired sales results and guides the marketing activity to the corrective action to achieve the desired marketing goals and objectives.

The actual performance may deviate from the desired performance due to many reasons including organisational factors and environmental factors. The marketing organisation will have to develop suitable strategy in terms of marketing mix programmes to counter environmental factors and necessary steps to correct any organisational factors.

Controlling may be defined as the process of analyzing actual operations and seeing that actual performance is guided towards expected performance. It involves comparing operating results with plans and taking corrective action when results deviate from plans. It is a mechanism by which someone or something is guided to follow the predetermined course. As a plan is put into operation, it becomes necessary to check results to find out whether the work is proceeding along the right lines. In case of any deviations, necessary corrective action is taken to ensure that in future the work proceeds in the desired manner.

According to Koontz and O’Donnell, “The managerial function of controlling is the measurement and correction of the performance of activities of subordinates in order to make sure that enterprise objectives and the plans devised to attain them are being accomplished.”

Concept of Control:

The essence of the concept is in determining whether the activity is achieving the desired results. In other words, the managerial function of control consists in a comparison of the actual performance with the planned performance with the object of discovering whether all is going on well according to plans.

Remedial action arising from a study of the deviations of the actual performance with the standard or planned performance will serve to correct the plans and make suitable changes in the process and structure of organisation, the staffing process and the process and techniques of direction. In this sense, the controlling function of management enables management to be self-corrective.

Nature of Control:

The main characteristics of the controlling function of management are given below:

- Control can be exercised only with reference to and on the basis of plans.

- The managerial functions cannot be completed effectively without performing the control function.

- Control is in fact a follow-up action to the other functions of management.

- It is an on-going process. That is, as long as an organisation exists, some sort of control is required.

- Control is forward-working because past cannot be controlled.

- Control is a process of measurement, comparison and verification.

- The essence of control is action.

- Control is dynamic and not static.

- Control aims at preventing unacceptable or incorrect performance.

- Control is a check-up measure. It comes in the end so as to ensure the proper implementation of plans.

Relationship between Planning and Control:

Planning is the basis of control. Control implies the existence of certain standards against which actual results may be evaluated. Planning provides such standards. Where there is no plan there is no basis for control. Planning sets the course and control makes operations adhere to that course. Planning initiates the process of management, control completes the process. Without plans, control is blind for when one does not know where to go, one cannot judge whether one is on the right track or not.

Hicks stated that “Planning is clearly a pre-requisite for controlling. It is utterly foolish to think that controlling could be accomplished without planning. Without planning there is no pre-determined understanding of the desired performance.” Control makes planning a meaningful exercise just as planning provides the guidelines for control.

Planning is meaningless without control and control is aimless without planning. Planning and control are the inseparable, the twins of management. Unplanned actions cannot be controlled, for control involves keeping activities on course by correcting deviations from plans.

Planning is looking ahead and control is looking back. Planning is the determination of objectives, goals, strategies, policies, programmes of an organisation to give purpose and direction to the activities of the organisation over a specified period of time. It is anticipatory. It reduces confusion and uncertainty.

Control, on the other hand, is the direction of the operations of an enterprise towards pre-determined standards and monitoring the process in this regard for the purpose of correction and feed back. The purpose of control is to see that the structure and the pace of events in a business are conforming to plans.

All controls imply existence of goals and plans. No manager can ascertain whether his subordinates are operating in the desired way unless he has a plan. Control will be much better if the plans are more clear, complete and well coordinated and cover a long period. Without planning, there may be no control. Planning and controlling are inseparable functions of management. Planning and control are interrelated and interdependent.

Purpose of Control (Objectives):

A sound control system is needed for the following purposes:

- Control reveals deficiency in planning: thus, plans and policies can be improved.

- Control helps managers to discharge their responsibilities.

- Control consists in verifying whether everything occurs in conformity with the plan adopted, the instruction issued and the principles established.

- A sound control system not only reveals deviations but suggests -the corrective actions required to overcome the deficiencies.

- Control keeps the subordinates under check and creates discipline among them.

- Effective control ensures efficiency and effectiveness in the organisation.

- A control system ensures the achievement of objectives.

Significance of Control (Benefits):

A good control system offers the following benefits:

- A good control system provides timely information to management which is very useful in taking corrective actions. Control reveals deficiency in planning so that suitable action can be taken to improve plans and policies.

- Control facilitates delegation and decentralization of authority. It helps to expand the span of supervision.

- It forces the individuals to integrate their efforts and to work as a team for the achievement of standards.

- It measures progress towards the goal and brings to light the adjustments, if any, required in day-to-day operations.

- Control enables management to verify the quality of various plans. Control helps to review, revise and update the plans. Without an efficient control system even the best plans may not work out as expected.

- Absence of control leads to a lowering of morale among employees because they cannot predict what will happen to them. They become the victims of the bias and repression of the superior.

- According to Terry, “Controlling helps ensure that actions proceed according to plans, that proper direction, is taken, and that the various factors are maintained in their correct interrelationships, so that adequate coordination is attained. “Control provides unity of direction.”

- In the content of predetermined goals, control keeps all activities and efforts within their fixed boundaries and makes them to move towards common goals through co-ordinated directives.

- An effective control system stimulates action by spotting the variations from the original plan highlighting them for the people who can set things right.

- A person is likely to act according to plan, if he is aware that his performance will be evaluated against the planned targets. Therefore, he is more inclined to achieve the results according to the standards fixed for him.

Limitation of Control:

- A firm cannot control the external factors-technological changes, changes in fashions, Government policies, social changes etc.

- In some cases, standards of performance cannot be defined in quantitative terms, for example, human behaviours.

- Control is a time-consuming and expensive process.

- Control may not be acceptable to employees.

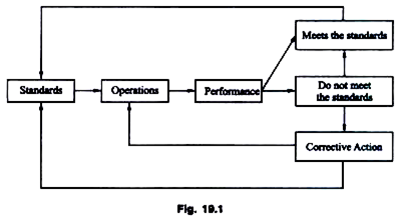

The control Process:

The process of control involves the following steps:

- Fixation of Standard:

The first step in control process is the setting up of control standards. Standards represent the criteria against which actual performance is measured. Standards serve as the benchmarks because they reflect the desired results or acceptable level of performance.

- Measurement of Performance:

After the fixation of standards, the actual performance of various individuals is measured. This involves setting up the methods of collecting accurate and up-to-date information on the progress of work. All measurements should be clear, comparable and reliable. Measurement of performance against standards should be on a future basis so that deviations are anticipated and necessary corrective actions are taken to prevent them.

- Comparing Performance with Standards:

This refers to the comparison of the actual performance with the standards. It should be remembered here that appraisal of actual performance becomes quite easy if the standards are properly determined and methods of measuring performance are clearly stated. It is also important to note that while making appraisal of performance, the manager should concentrate mainly on those matters where major deviations are noticed.

- Analysis of Deviations:

All deviations need not be brought to the notice of top management. A range of deviations should be established and only cases beyond this range should be reported. This is known as control by exception. When the deviation between standard and actual performance is beyond the prescribed limit, an analysis of deviations is made to identify the causes of deviations. Then the deviations and causes are reported to the managers who are authorized to take action.

- Talking Corrective Action:

More reporting of actual performance or its comparison with predetermined standards is not sufficient. Unless timely action is taken to adjust operations to standards, control process is incomplete. Corrective action may involve setting of new goals, change in organisation structure, and improvement in staffing and new techniques of directing.

Pre-Requisites of a good control system:

- The objective and target must be clear.

- The control system must be suitable.

- The system should be easy to understand and operate.

- Selection of tools and techniques must be proper.

- There must be speedy feedback system.

- There must be prompt reporting system of variances.

- It must justify the expenses involved.

- There must be a good system of corrective actions.

- It must fix individual responsibility for the poor performance.

- Controls, which are essential, should be given priority.

Marketing Controls:

There are several types of control available and the importance and purpose of these controls depend on the objectives for which these controls are to be used. All these controls have a common purpose, that is, monitoring the key result areas is marketing management. The key results are generally common for all marketing organisations.

Some of the important marketing controls commonly used are:

- Annual Plan Control:

This is the most basic of all controls used in marketing organisations. The main purpose of this control is to monitor and take corrective action to examine whether planned sales results are being achieved. The responsibility for this lies with the marketing departmental head and all others in the top management.

- Profitability Control:

Besides annual-plan control, companies carry on periodic research to determine the actual profitability of their different products, territories, customer groups, trade channels, order size etc. The task requires an ability to assign marketing and other costs to specific marketing entities and activities.

- Efficiency Control:

Suppose a profitability analysis reveals that the company is earning poor profits in connection with certain products, territories or markets. The question is whether there are more efficient ways to manage the sales force, advertising, sales promotion. Distribution etc.

- Strategic Control:

Organisations should examine critically their policies, objectives, marketing strategy, and competitive advantage and growth opportunities regularly so that their direction and growth and overall marketing effectiveness is not impaired or reduced. The scanning of marketing environment has become much more relevant and significant in view of uncertain’ economic conditions, fast changing technology, customer life-style, demographic changes etc.