Financial Management, Introductions, Concept, Introduction, Objectives, Scope, Functions and Goals

by

by Financial Management involves planning, organizing, directing, and controlling financial activities to achieve an organization’s objectives. It focuses on the efficient procurement and utilization of funds while balancing risk and profitability. Key aspects include capital budgeting, determining financial structure, managing working capital, and ensuring liquidity. It aims to maximize shareholder wealth by optimizing resource allocation and minimizing costs. Effective financial management supports decision-making related to investments, financing, and dividends, ensuring sustainable growth. It also involves analyzing financial risks and returns, maintaining financial stability, and complying with legal and regulatory requirements.

Financial Management is a critical function in business management, dealing with the planning, procurement, and utilization of funds to achieve organizational objectives. It ensures that adequate funds are available at the right time and are used efficiently to maximize returns while maintaining liquidity and solvency. It integrates financial planning, control, and decision-making to support business growth, stability, and profitability.

In a business, financial management plays a pivotal role in sustaining operations, investing in new opportunities, and managing risks. It acts as the backbone for decision-making in areas like capital budgeting, financing, dividend policy, and working capital management. A sound financial strategy enables organizations to achieve both short-term operational efficiency and long-term strategic goals.

Objectives of Financial Management

- Ensuring Adequate Funds

One of the primary objectives of financial management is to ensure that a business always has adequate funds to meet its operational, investment, and contingency needs. This involves careful planning of financial requirements, estimating cash inflows and outflows, and maintaining liquidity. Adequate funds ensure smooth functioning, prevent financial crises, and help the organization fulfill its commitments to employees, suppliers, and creditors.

- Maximizing Profitability

Financial management aims to maximize the profitability of the business by making sound investment and financing decisions. Profitable operations increase the value of the business, provide higher returns to shareholders, and create resources for growth and expansion. Decisions related to cost control, pricing, and investment appraisal are made to enhance profit while managing risks effectively.

- Ensuring Liquidity

Maintaining liquidity is crucial for meeting short-term obligations, such as paying salaries, creditors, and taxes. Financial management focuses on balancing liquidity and profitability to avoid insolvency. Sufficient liquid resources enable the organization to handle emergencies and sustain operations without disrupting production or service delivery.

- Optimal Utilization of Funds

Financial management ensures that the funds available are used in the most efficient manner. Resources should be allocated to the most profitable projects and departments, avoiding wastage or underutilization. This objective supports cost control, resource efficiency, and higher returns on investment, ensuring that every rupee invested contributes to business growth.

- Minimizing Cost of Capital

Another objective is to procure funds at the lowest possible cost while balancing risk and ownership control. Financial managers strive to maintain an optimal mix of debt and equity to reduce the overall cost of capital. Efficient financing reduces interest expenses, improves profitability, and enhances the organization’s financial stability.

- Maximizing Shareholder Wealth

Financial management aims to maximize the wealth of shareholders by ensuring a steady growth in earnings and dividends. Long-term strategies, such as profitable investments and prudent financing, contribute to increasing share value. Shareholder wealth maximization aligns financial decisions with owners’ interests, creating trust and attracting further investment.

- Financial Planning and Forecasting

Financial management involves systematic planning and forecasting to predict future financial requirements. Proper financial planning helps in anticipating fund shortages or surpluses, reducing uncertainties, and ensuring timely availability of resources. Forecasting also supports investment decisions, risk management, and long-term business growth.

- Ensuring Financial Stability and Risk Management

Maintaining financial stability is a key objective to protect the business from unexpected losses or economic downturns. Financial management incorporates risk assessment and mitigation strategies, such as diversification, insurance, and hedging. A stable financial position allows the organization to survive crises, maintain creditworthiness, and plan for sustainable growth.

Scope of Financial Management

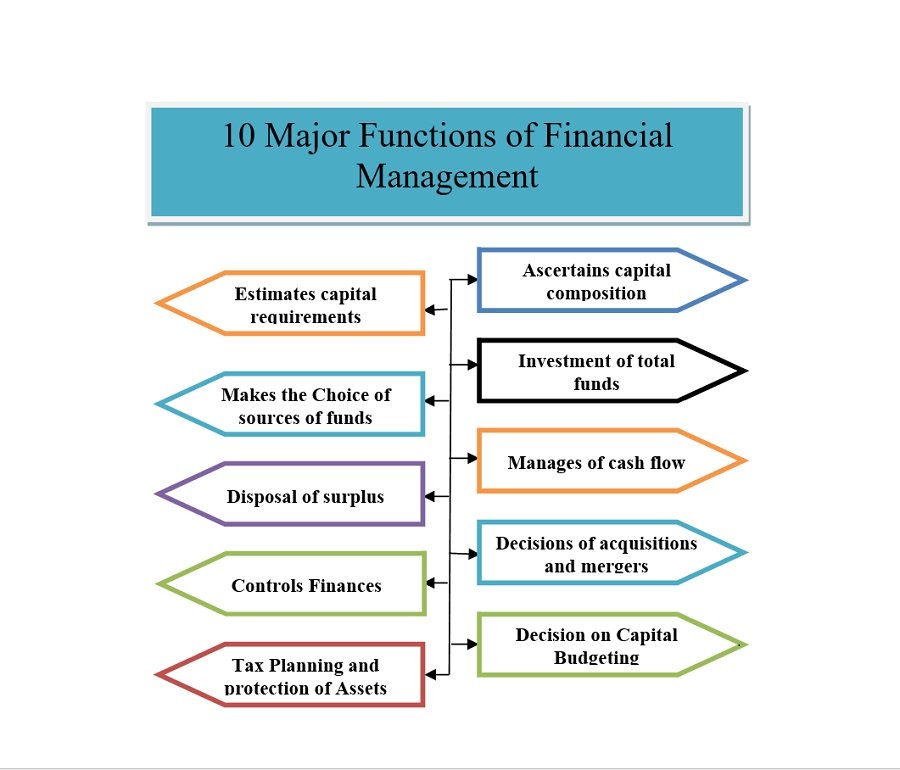

Functions of Financial Management

Financial management involves a wide range of activities aimed at ensuring the effective acquisition, allocation, and control of funds in an organization. Its primary functions can be classified into three broad categories: Investment, Financing, and Dividend decisions, along with supportive functions like financial planning and control.

- Investment or Capital Budgeting Function

This function involves deciding where and how to invest the funds of the organization to generate maximum returns. It includes analyzing long-term investment proposals, evaluating risks, and choosing projects that align with the company’s objectives. Proper capital budgeting ensures efficient utilization of resources and supports growth while balancing profitability and risk.

- Financing Function

Financing deals with raising funds from appropriate sources at the right time and cost. This includes selecting the optimal mix of debt, equity, and retained earnings to finance operations and investments. Efficient financing ensures sufficient funds are available without overburdening the company with high costs or risking financial stability.

- Dividend Decision Function

This function focuses on deciding the portion of profits to be distributed as dividends and the portion to be retained for business growth. Dividend decisions affect shareholders’ satisfaction and the company’s ability to reinvest in expansion or meet financial obligations. A balanced dividend policy maintains investor confidence while supporting long-term financial goals.

- Financial Planning Function

Financial planning involves forecasting future financial needs and determining strategies to meet them. It includes estimating capital requirements, projecting cash flows, and planning for contingencies. Proper financial planning ensures the availability of funds when needed, minimizes financial risk, and avoids liquidity crises.

- Financial Control Function

Financial control focuses on monitoring and regulating financial resources to ensure they are used efficiently. It involves budgeting, cost control, auditing, and financial reporting. Effective financial control prevents misuse of funds, improves accountability, and supports strategic decision-making.

- Working Capital Management

This function deals with managing short-term assets and liabilities to ensure smooth day-to-day operations. It includes managing cash, inventory, receivables, and payables. Efficient working capital management maintains liquidity, reduces financing costs, and ensures the company can meet its short-term obligations.

- Risk Management Function

Financial management also involves identifying, assessing, and mitigating financial risks. This includes interest rate risk, credit risk, market risk, and operational risk. Proper risk management protects the organization from potential losses and ensures long-term financial stability.

- Profit Planning and Management

Financial management ensures that funds are used efficiently to maximize profits. It involves cost analysis, revenue planning, and investment appraisal to achieve optimal returns. Profit planning helps in achieving business growth, enhancing shareholder wealth, and maintaining competitive advantage.

Goals of Financial Management

Financial management involves planning, acquiring, and utilizing funds to achieve organizational objectives. Its goals represent the desired outcomes that guide financial decisions and strategies. These goals ensure the business uses its resources efficiently while maintaining stability and growth. Broadly, financial management goals can be classified into primary goals and secondary goals.

- Primary Goal: Wealth Maximization

The foremost goal of financial management is maximizing the wealth of shareholders. Wealth maximization focuses on increasing the market value of the company’s shares over the long term. This goal ensures that financial decisions, whether related to investment, financing, or dividend distribution, aim to enhance the overall value of the firm. It balances risk and return, prioritizing long-term sustainability over short-term profits.

- Profit Maximization

Profit maximization refers to increasing the company’s earnings in the short term by efficiently managing costs and revenues. While important, this goal does not consider the time value of money, risk factors, or long-term growth. Hence, wealth maximization is often preferred as it provides a broader perspective, ensuring both profitability and sustainable growth.

- Ensuring Liquidity

A vital goal of financial management is maintaining adequate liquidity to meet short-term obligations like salaries, taxes, and creditor payments. Without sufficient liquidity, a company may face insolvency despite being profitable on paper. Proper cash flow management ensures smooth operations, financial stability, and the ability to respond to emergencies.

- Efficient Fund Utilization

Financial management aims to allocate resources optimally across various projects and departments. Efficient fund utilization avoids wastage, reduces costs, and ensures maximum returns from investments. Proper budgeting, cost control, and performance monitoring contribute to this goal, enhancing overall organizational efficiency.

- Risk Management

Financial management seeks to identify, assess, and mitigate financial risks, such as market fluctuations, credit risk, and operational risk. By adopting hedging techniques, diversification, and insurance, organizations can safeguard their resources and ensure stability in uncertain economic conditions. Effective risk management protects both the company and its shareholders.

- Ensuring Financial Stability

Maintaining a stable financial position is a key goal. Stability enables the organization to sustain operations, attract investors, and maintain creditworthiness. A stable financial environment supports long-term growth, facilitates expansion plans, and improves stakeholder confidence.

- Optimal Capital Structure

Financial management aims to achieve an optimal mix of debt and equity to finance operations. A balanced capital structure reduces the overall cost of capital, enhances profitability, and minimizes financial risk. It ensures that funds are available when needed without overburdening the company with debt obligations.

- Social and Ethical Goals

Modern financial management also considers social responsibility and ethical practices. This includes responsible investment, compliance with regulations, and fair treatment of stakeholders. Incorporating ethical considerations ensures sustainable growth and enhances the company’s reputation.